Property Investment

Property Market Update (May)

See how your property market is tracking and what’s happening with house prices today.

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

“How much will house prices go up in the next 10 years?”

That was the most common question I got on a webinar earlier this week (from over 600 investors!)

Now I don’t have a crystal ball.

But I do have data (and a new tool for you to play with).

Let's say you're trying to figure out where house prices might go up over the next 10 years.

You might start with what happened to property values over the last decade.

And if you did that, you’d see that Auckland has gone up the slowest of the main cities:

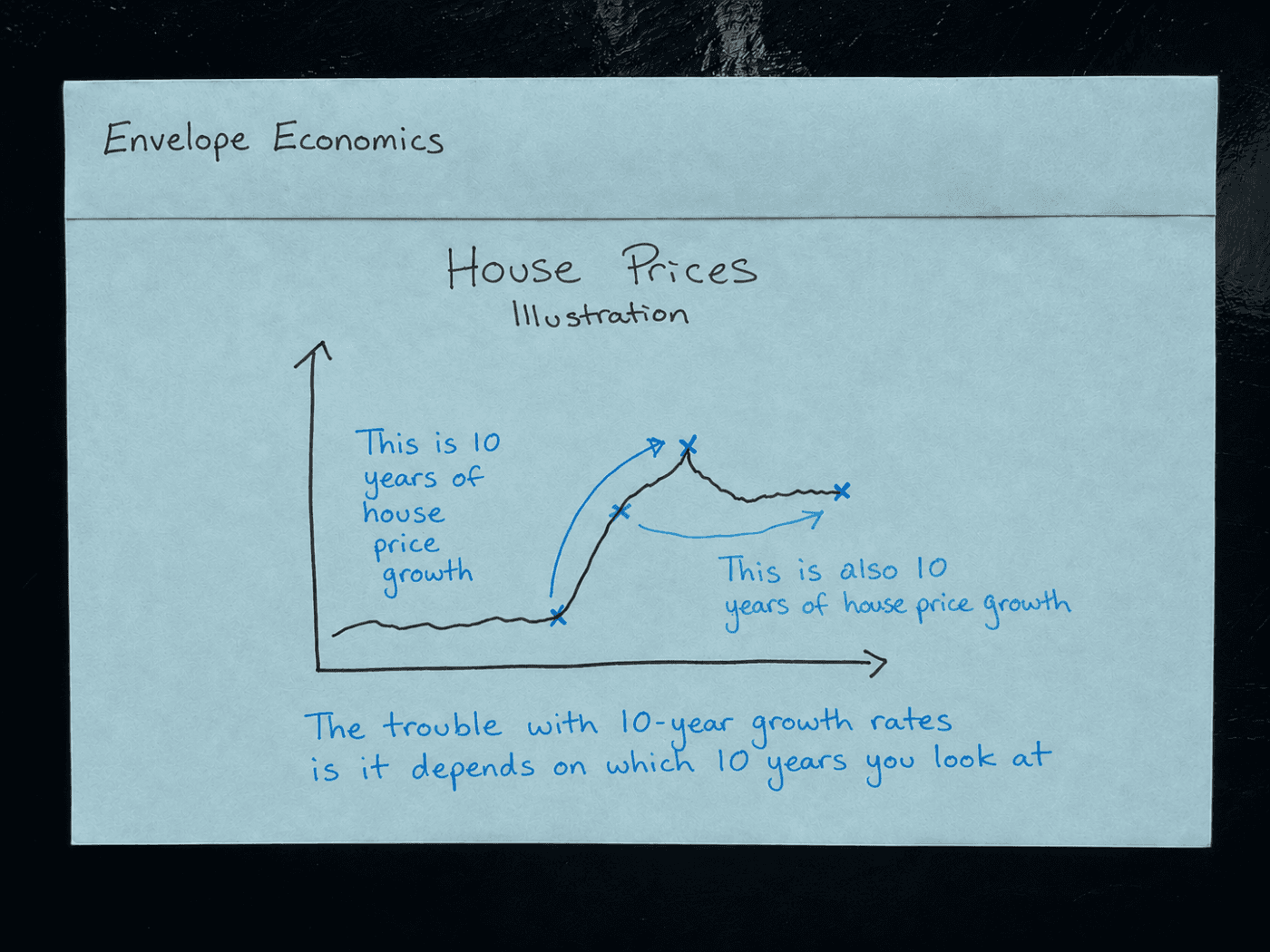

But there’s a problem with this.

These numbers are HEAVILY influenced by where house prices happened to be 10 years ago … and where they are today.

And if the 10-year period you look at:

Auckland is a great example.

Because 10 years ago, Auckland had just finished a massive house price run. And right now, it’s in a deep downturn.

10 years ago, Christchurch had been flat for ages. Now it’s at the top of a massive boom.

So looking at a single 10-year window might not tell you what often happened in the past.

So, I often say to investors, don’t ask: “What happened over the last 10 years?”

Instead, ask: "What usually happens over 10 years?"

That sounds great in theory, but how do you get the numbers?

The trouble with these numbers is that they are hard to calculate.

That’s for 2 reasons:

And unless you're the sort of person who enjoys spending Friday nights inside Excel, it's a bit of a mission.

So, I asked our economist (Ed) to create a tool.

And for once in his life, he's actually listened (and remembered), and he built you this 👇

Here’s what it does:

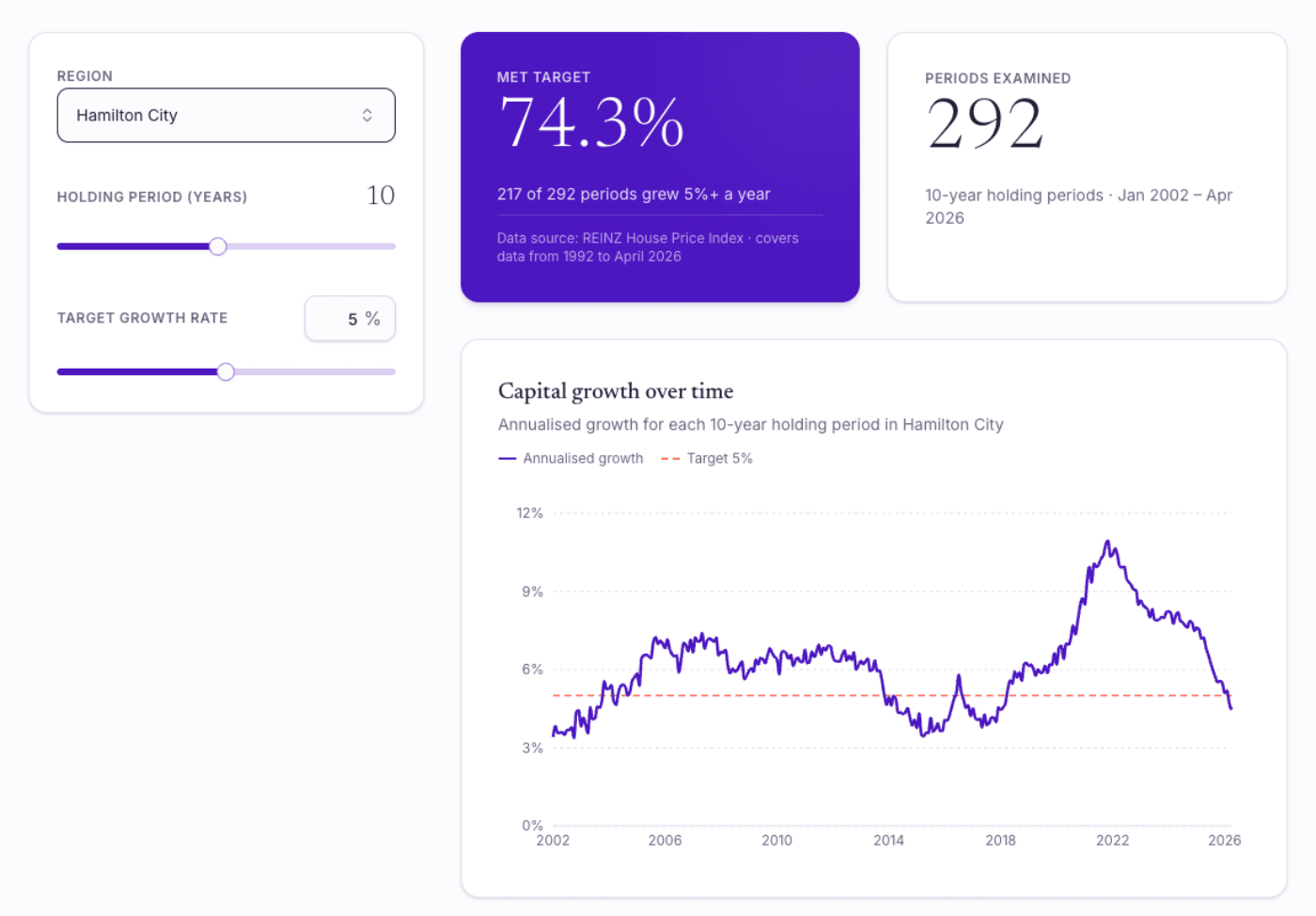

Let's say you want to know how fast house prices typically rise in Hamilton over 10 years.

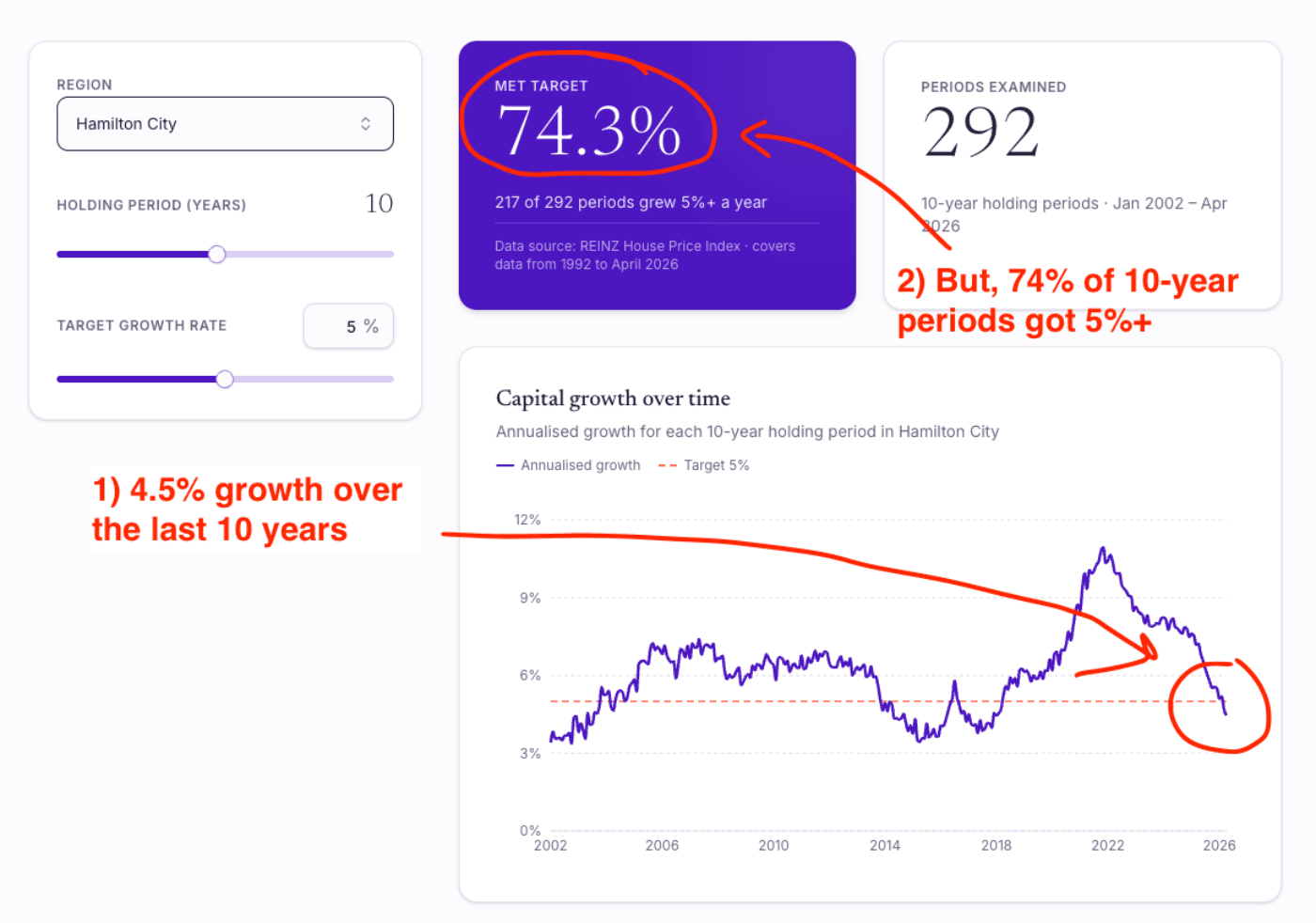

Over the last 10 years, Hamilton house prices rose by 4.5% per year.

So, you might think, well, that gives me a sense of what might happen over the next 10 years.

But that’s only one 10-year period. So, it might not tell you what usually happens.

That’s why this tool compares:

And it does this 292 times. That way, you can see what tends to happen over 10 years. (Or, however many years you care about).

Hamilton house prices have only gone up 4.5% per year over the last decade.

If you bought at any random time since 1992, and held for 10 years, 74.3% of the time, your house value would have gone up by at least 5% per year.

That’s assuming that your house followed the market perfectly.

So, it gives you a more well-rounded way to understand how much house prices have gone up in the past.

Here’s how you can use it. Head to the: Long-term house price growth calculator

Then, you put in:

And it shows how often that growth rate has been achieved in the past.

Now, this tool won’t predict the future. Nothing can.

But I am a big believer in putting the data in your hands.

That way, you’re in the driver’s seat of your property investing journey, and you can get a sense of how fast you think house prices might go up in the future.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser