Property Investment

Can you predict next year’s best-performing property market?

Everyone wants to know which property market will boom next. The truth might surprise you 👇

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

Most property investors are doing the right things. But they're not sure if it's enough to create the future they want.

That’s where you need a Wealth Plan … and it's simpler than you think.

In today’s newsletter, I’ll not just show you how I do it for investors. But also, how you can do it yourself in 20 minutes (or less).

Here's how to create one in four easy steps.

A good Wealth Plan answers one big question: Am I on track for the future I want?

But before you even think about property or shares, you need to start with what that future looks like.

I like to ask people: “When you close your eyes and think about your perfect day of financial freedom … what are you doing (specifically)?”

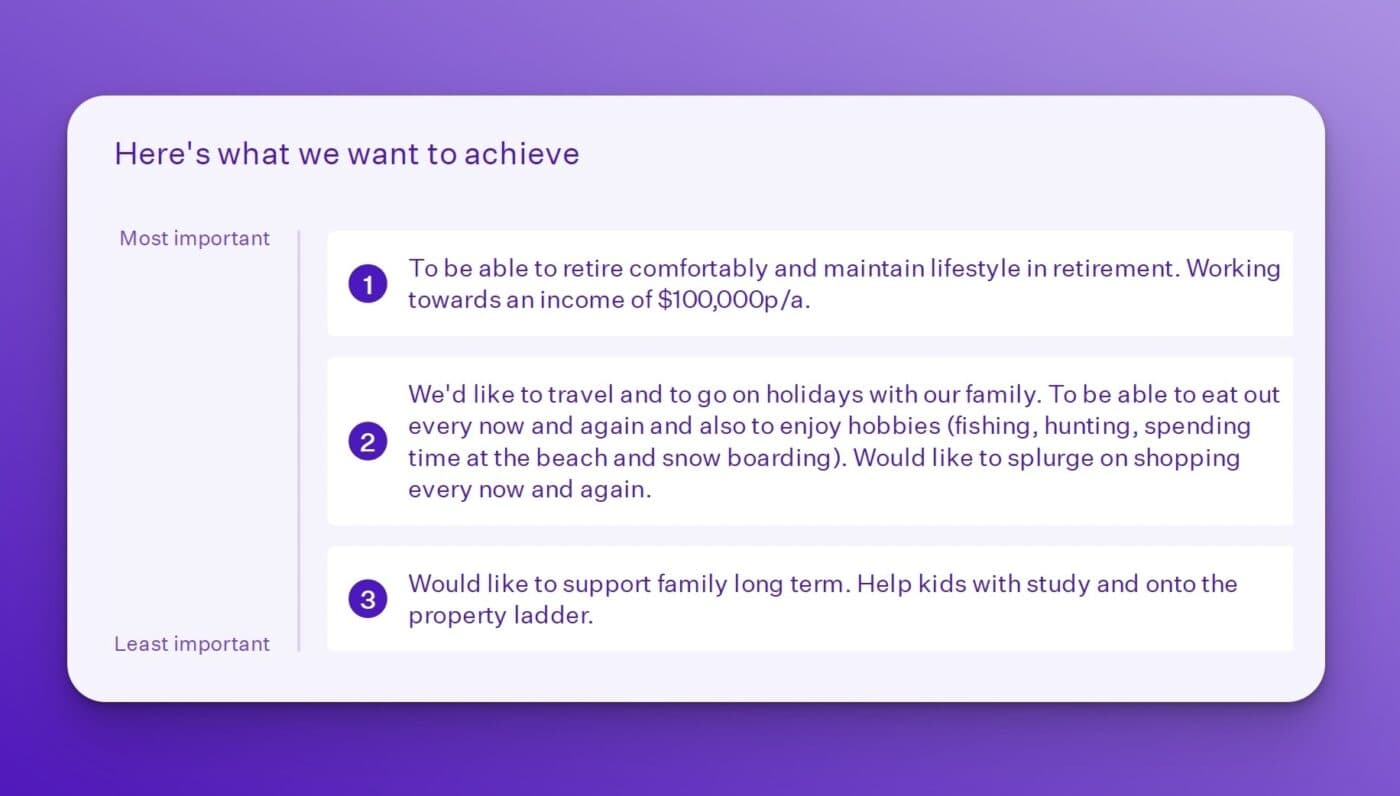

Here’s a real example of a couple in their 40s. They want to retire in 20 years. This is what they want out of life. (Shared with permission).

Pretty normal stuff. No superyachts. Just the freedom to go fishing on a Tuesday without checking the bank account first.

This couple wants to spend $100,000 a year starting in 20 years. So, how much wealth do they need to make it happen?

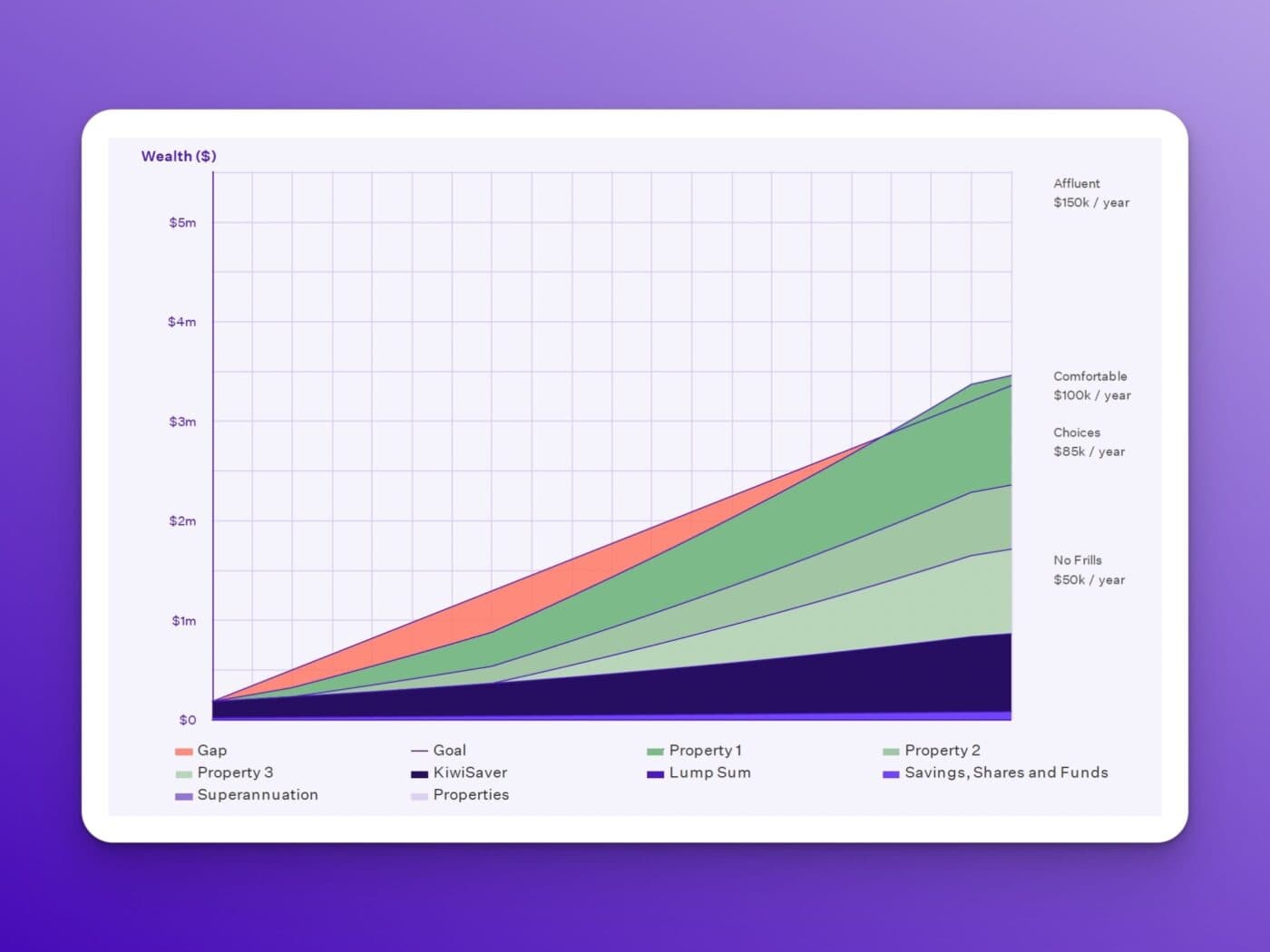

Once you run the numbers, the answer is just shy of $3.4 million in investments. That’s a lot of money. But, remember you’re probably not starting from 0.

Even if you don’t feel like you’re investing much now … you still might be if you have KiwiSaver.

And even if you don’t have a lot of wealth today, your current investments could grow substantially over time.

So you want to understand how much money you'll end up with if you just keep doing what you're doing now.

That’s what a good plan calculates.

If there is a difference between how much wealth you’ll need. And how much wealth you’re on track to have … then you have a Wealth Gap.

For this couple:

If they did nothing, their retirement income wouldn't be $100,000 a year. It would be around $29.4k. That's a $70.6k annual shortfall.

That might sound scary. But at that point, you can either pull back your goal, deciding to live on less. Or you can do something about it to close the gap.

One thing to note: this couple decided not to factor NZ Super into their plan. Because they don’t know what it’ll look like in 20 years. They’re treating that as a bonus.

Once you know your Wealth Gap, you've got options. You can invest more in KiwiSaver, look at shares, buy property, or invest in something else. The right answer depends on your situation.

But, let’s say our couple wants to invest in property.

They plan to buy 3 investment properties over the next few years and hold on to them for the long term.

A good financial plan will project how much wealth those properties could create over that time.

In 20 years, those 3 properties are projected to have enough wealth to close their Wealth Gap. And if that happens, this couple could spend around $70k more in retirement than they could now.

Of course, a financial plan has a bit more to it than this. You should think about:

But the core of it is these four steps.

I hate telling people what to do … without showing you how to do it.

So if you want to create your own plan, you have two options:

Good: You can jump into Opes+ and create your own plan.

(Remember, Opes+ is NZ’s #1 investing app for property investors)

Better: You can get one of my financial advisers to create your Wealth Plan with you. Book a free meeting with my financial advisers here.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser