Property Investment

Bad news

It’s not all doom and gloom. With investing, there’s always something working for and against you. Here’s what you need to know 👇

Property Investment

3 min read

Author: Andrew Nicol

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Private Property – our weekly newsletter that gives you insights into what's happening in the NZ property market. Written by managing director Andrew Nicol. Sign up to receive this in your inbox every Thursday.

This is your warning.

The Reserve Bank will probably introduce debt-to-income (DTI) restrictions in the next few years.

Two weeks ago, the Reserve Bank gave themselves the authority to bring in a DTI ratio at any time.

Once this comes in, you probably won’t be able to borrow as much. And your property portfolio will likely slow down.

This is big. Here’s what you need to know.

A debt-to-income ratio will decrease how much Kiwis can borrow, which the Reserve Bank hopes will slow down house prices.

Here’s how they work. A DTI limits how much you can borrow based on your income.

To work out how much you can borrow:

Income x DTI = max borrowing

For instance, let’s say you and your partner earn $100,000 (together) a year.

If the debt-to-income ratio is 7, you can only borrow $700,000.

$100,000 x 7 = $700,000

So, is the maximum debt-to-income ratio going to be 7x?

We don’t know … the Reserve Bank won’t announce the exact DTI until they bring it in. But it will likely be 6x or 7x.

Property investors and owner occupiers with large mortgages will be hit the hardest.

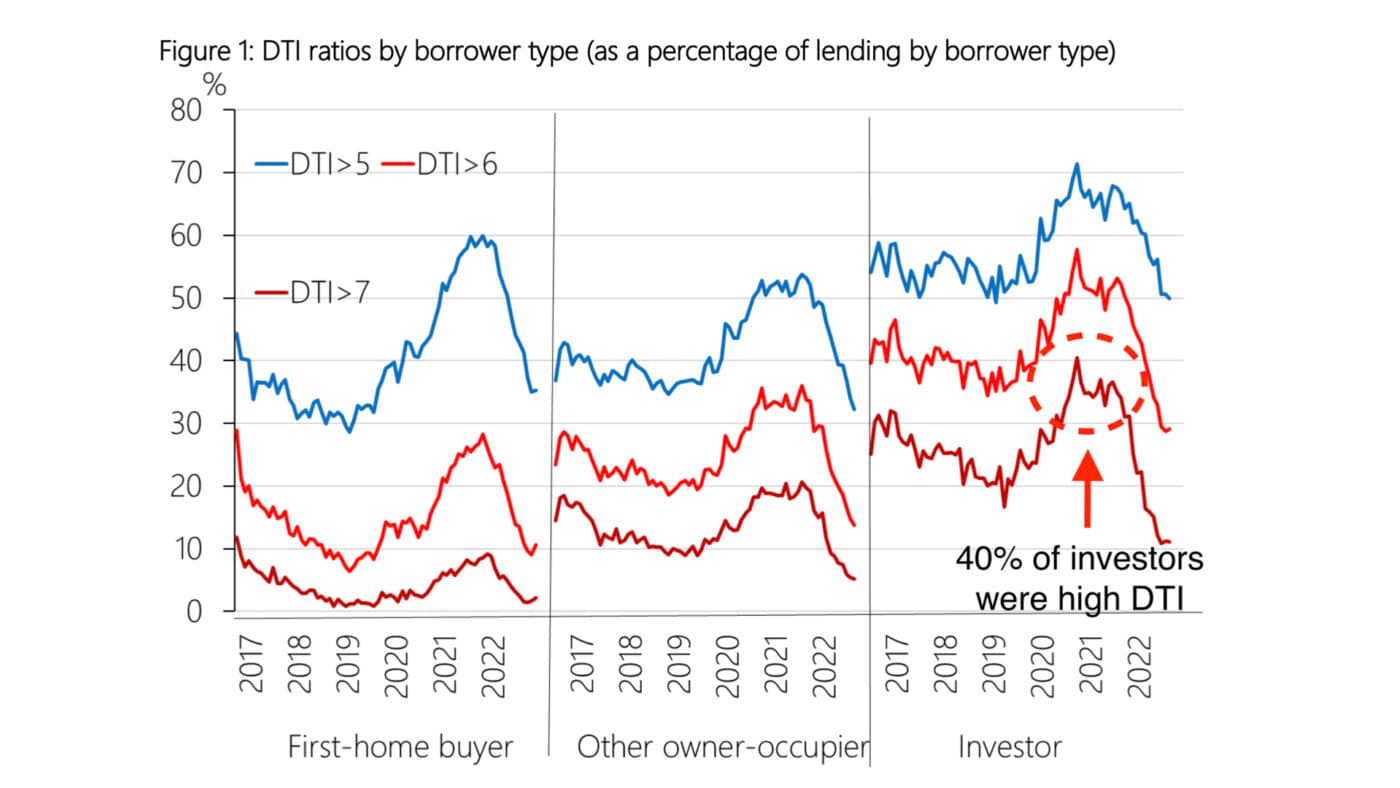

Look at this graph. At the peak, 40% of property investors were purchasing with a Debt to Income ratio of over 7x.

If the Reserve Bank had implemented a 7x DTI limit at that time, it would have potentially wiped out a large chunk of property purchases.

This would have stopped a large chunk of investors from growing their portfolios and from preparing for retirement.

It’s a lot. The DTIs come in addition to other recent lending rules like the Loan to Value Ratio restrictions (LVRs), the CCCFA, and bank stress tests.

So you might wonder, how do I keep investing?

There are three main ways:

The DTIs don’t apply to new builds, so if you’re investing in new builds with us here at Opes Partners, you probably won’t be impacted by these changes.

Sometime from March 2024 onwards. While the rules are live now, the banks need time to change their IT systems.

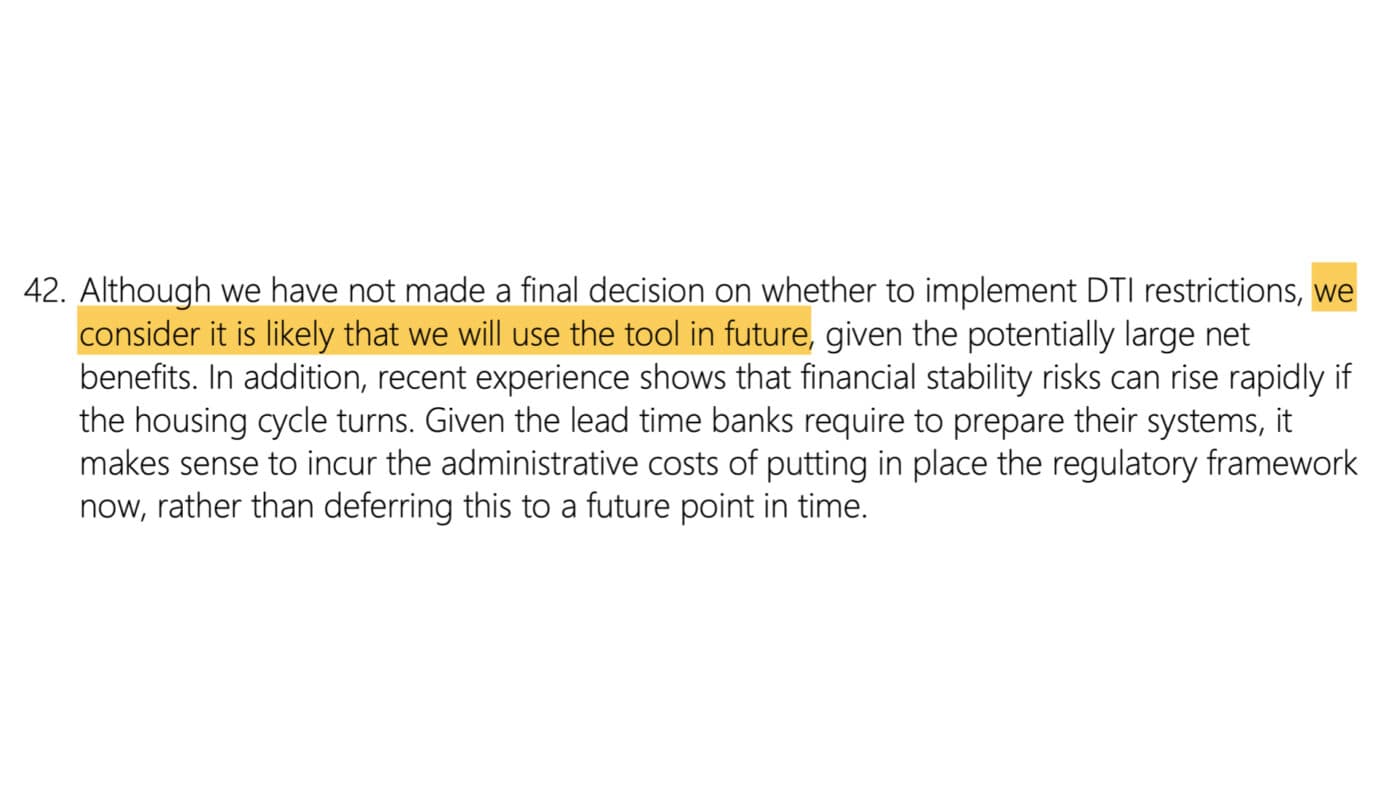

However, the Reserve Bank says that … “we consider it likely that we will use this tool in future.”

My best guess is that next time property prices start to rise again, they’ll bring in a DTI … and bring it in quickly.

That’s why they’ve done the work now, so they can snap their fingers and bring it in later.

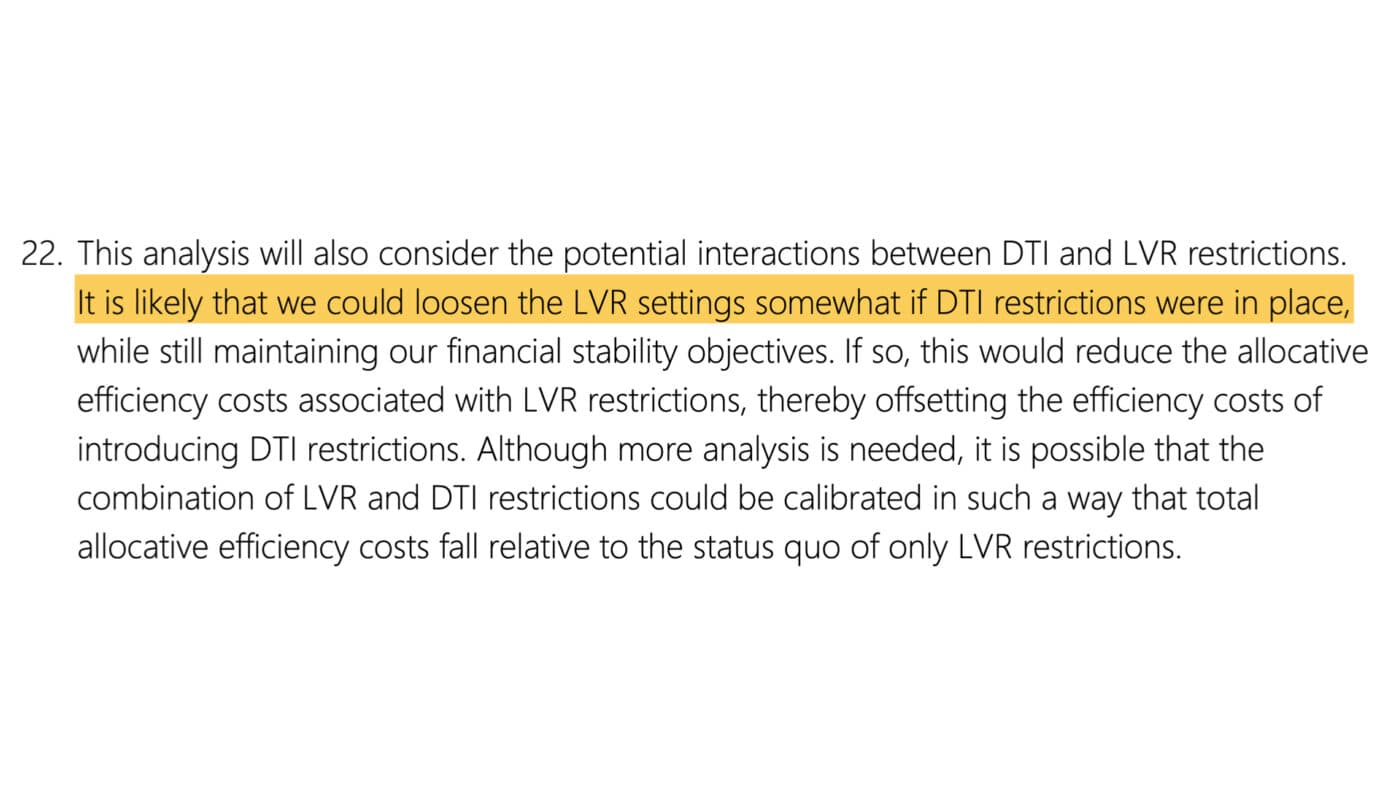

There is one (small) silver lining. When the DTIs come in, the Reserve Bank says it is likely that the LVR restrictions could be loosened.

Let’s say you’ve got a decent income but are tight on deposit (equity). This new regulation might help you borrow more, depending on your situation.

For some property investors, this change won’t impact them much … especially if you’ve got low debt or are investing in new builds.

But for others … you may not be able to become a property investor or grow your portfolio once these restrictions come in.

If that’s you, investing now before the DTIs come in could be a good idea.

I believe the best time to invest is when the bank’s willing to give you the money. In a year, they might not give it to you.

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser