Property Investment

Iran and interest rates

Petrol prices are climbing fast. So is this the start of higher interest rates again? Here’s what investors need to know 👇

Property Investment

3 min read

Author: Andrew Nicol

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Yesterday, a first-time investor asked: “How do I know for sure my investment property will go up in value?”

The answer is you will never know. Not for sure. There is no guarantee.

But this question has always bugged me.

We know property tends to go up in value. But how could I show the probability?

So, I hired MyFiduciary, a nerdy investment company, to help me run the numbers.

Here’s what we get –

If you buy a property in Auckland, our model suggests that:

Flip around the other way. After 10 years, you have a 92% chance that your house has gone up in value.

What’s the trend?

If you buy a property and only hold it for a few years, you have a larger chance of losing money.

There’s more risk.

If you buy a property and hold it for decades, there is a smaller chance of losing money. There is less risk.

Property is more risky if you buy and sell quickly. It is less risky if you are in it for the long run.

Because this is a new concept, it can be hard to get your head around. Think of it this way.

Property values tend to go up in the long term. But, sometimes, they’re up. Sometimes, they’re down.

Think about an area like Gisborne. Over the last 30 years, property values in the region have gone up by 6.36% a year on average.

But there were 9 years between 2007 and 2016 when house prices didn’t go up at all. Most of the time they went backwards.

That’s an example where you can own a property for 10 years, and be close to being in that unlucky 8%.

But 5 years later, Gisborne house prices had spiked. Property owners in the region made money. So hold on for the long term, and you’re more likely to make money.

If you’re a data nerd, you probably want to know how we run the numbers.

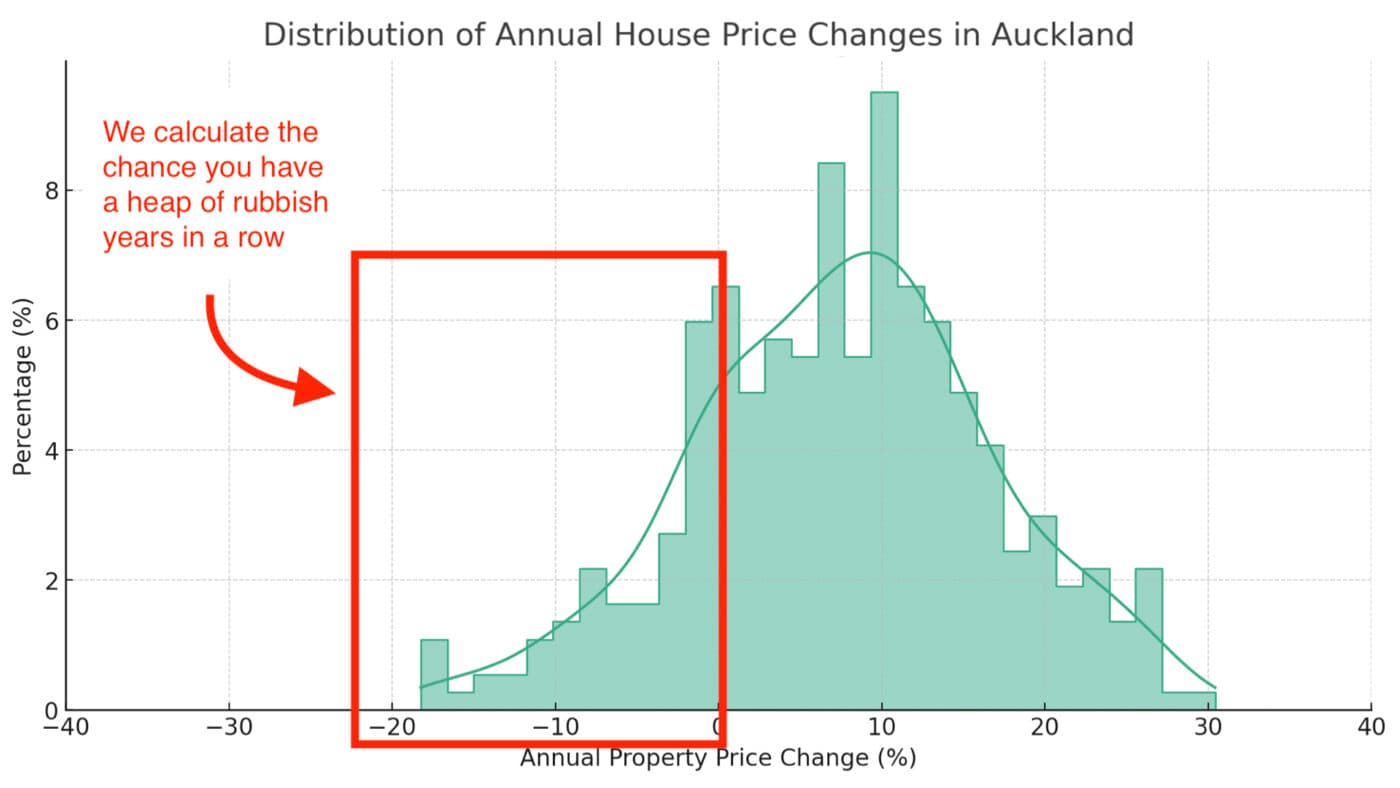

First, we look at how fast house prices have gone up per year in Auckland. We use over 30 years' worth of data.

This gives us a bell curve.

Sometimes, property prices go up very fast. Sometimes, they go up very slowly. Most of the time, it’s somewhere in the middle.

Then, we dial up the chance that property prices move around more in the future (just to be conservative).

Then we get to the good bit.

We calculate the probability that we stick at the bottom end of that distribution.

It’s just like asking, “what’s the chance we have a whole heap of rubbish years in a row where the bad years outweigh the good?”

It’s not perfect. It’s not a crystal ball. But it’s better than saying, “property always goes up in value.” Because – depending on the timeframe – it doesn’t.

I’m not sharing this to make you scared or think that property is a bad investment.

There is a chance you lose money in any investment. All investments have risks.

I’m sharing this with you so you understand the risk and know how to handle it.

How do you handle it?

This helps you quantify the risk so you can prepare for the good and the bad.

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser