Property Investment

How much are property investors really adding to the economy? [New report]

Are landlords really greedy parasites? Here’s what the new data says 👇

Property Investment

4 min read

Author: Andrew Nicol

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

If you’ve read this newsletter for a while, you’ll have seen our over and undervalued model.

It’s a way of figuring out if an area looks a bit cheap or a bit expensive.

For instance, Auckland currently looks about 9% undervalued. So it could be a good place to invest.

This is one of the main tools I use with my clients and investors when deciding where to buy.

The other day, an investor asked: “Does this actually work? Will it really help me make more money?”

So, I ran the numbers to see what would happen if you blindly bought properties in undervalued areas. Let’s start back in the year 2000.

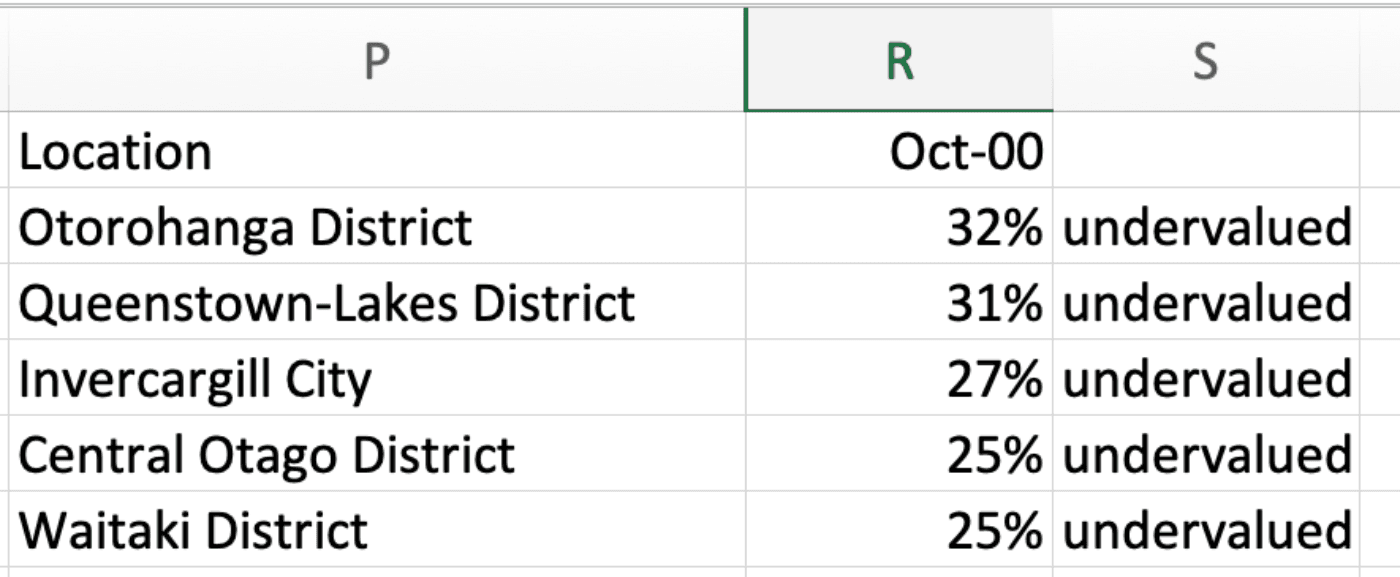

If you crunched the numbers 23 years ago, here’s what you would have seen:

Otorohanga was the most undervalued area (32%), followed by Queenstown (31%).

Looking at that data, I would have invested in Queenstown. Back then, you could buy there for $200k.

So what would have happened if you bought a property there instead of a $200k property anywhere else in NZ?

4 years later, the value of your Queenstown property would have increased by $215,000.

Whereas $200k invested in the average NZ property would have gone up in value by $121,000.

So, you’ve made $94,000 more in 4 years by buying in the undervalued area.

You're feeling chuffed, so you decide to buy again.

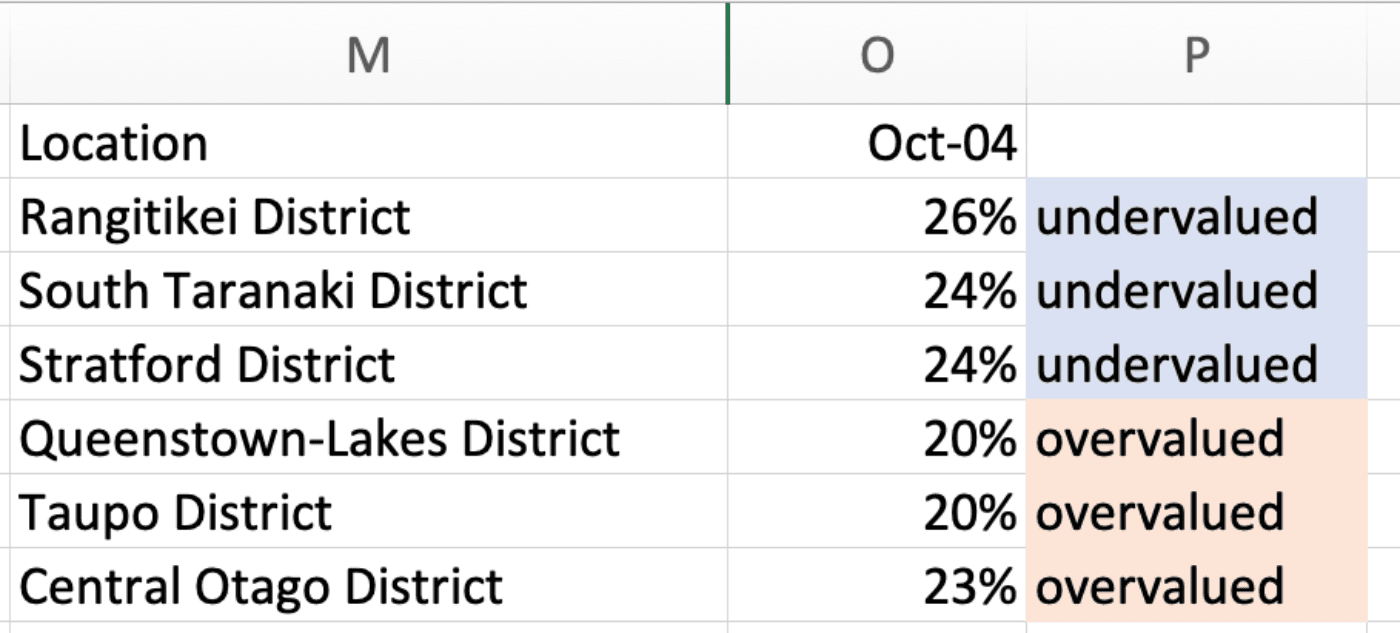

4 years later, here’s what the data looked like:

Queenstown is now 20% overvalued. You wouldn’t invest there, even though the market performed for you.

Instead, the most undervalued areas are Rangitikei (26%) and South Taranaki (24%).

Back then, you could buy a house in South Taranaki for $100k.

So what would’ve happened to a $100k property there vs the average $100k property in NZ?

4 years later, the South Taranaki property increased in value by $83k. That compares to $24k for the average property.

Again, the undervalued area outperformed by $59,000.

Let’s go again 4 years later.

At the tail end of the GFC, Auckland was 8% undervalued. You could buy a property there for $425k.

4 years later a $425k property in Auckland would be worth $237k more. That compares to $122k more for NZ's average $425k property.

Once again, the undervalued region outperforms. This time by $115,000.

Don’t skip ahead. The next one is critical.

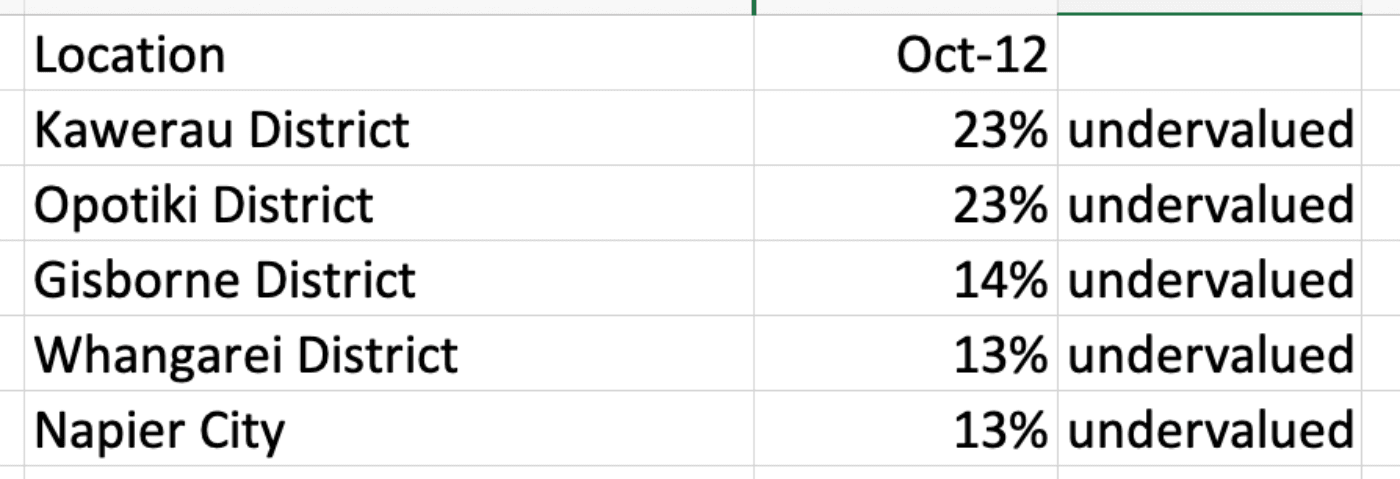

If you re-ran the same model in 2012, here’s where the most undervalued areas were:

A lot of these are smaller districts. So, let’s say you decide to invest in Napier. Back then, you could buy a property for $300k.

Did you get a better return investing in Napier?

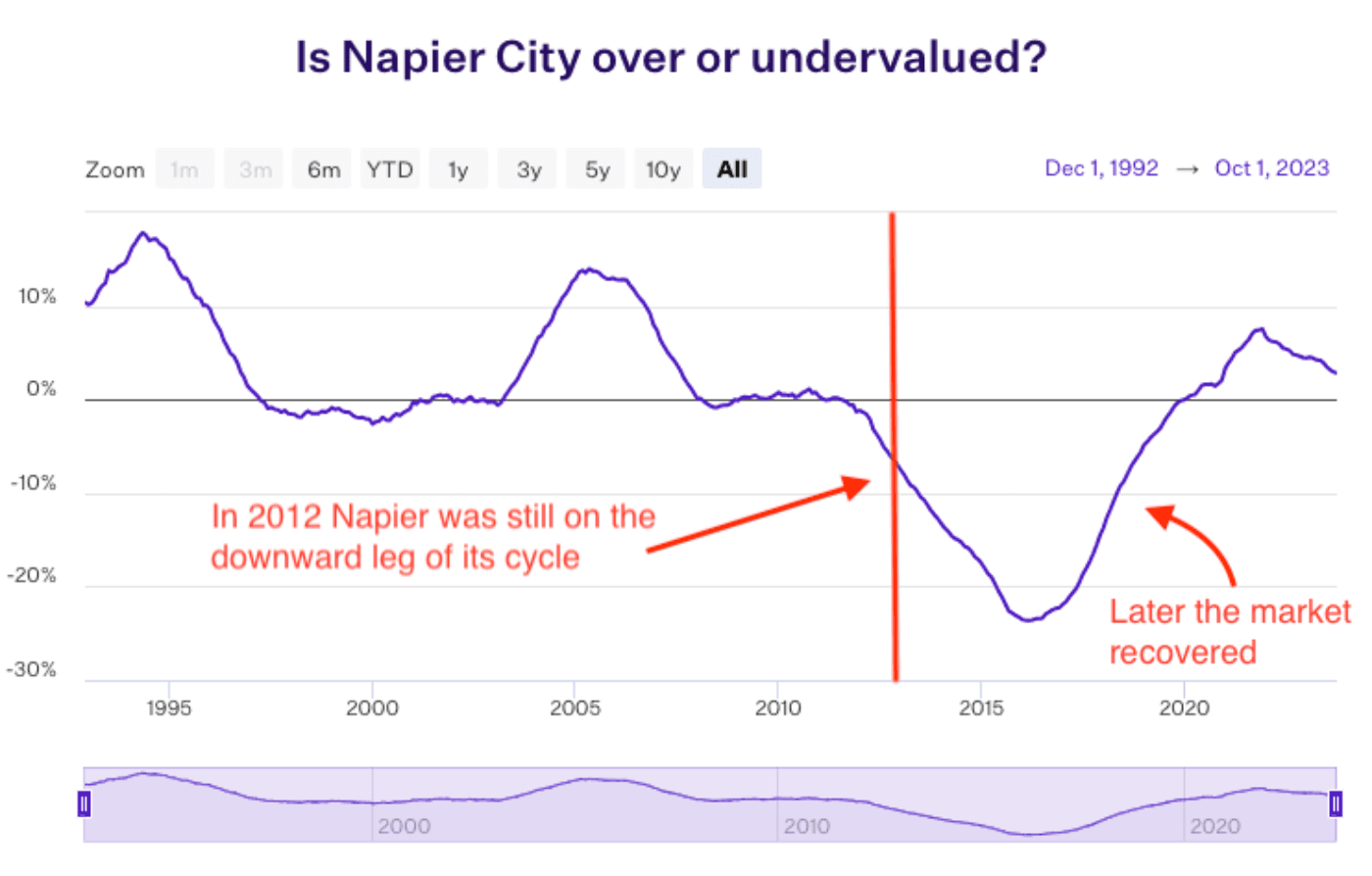

No. In this case, the undervalued area underperformed.

The Napier property’s value jumped $108k after 4 years. But the average property in NZ shot up in value by $163k.

Why did this happen? Well, the model isn’t bulletproof – especially in the short term.

Because Napier was still on the downward leg of its property cycle. It took another few years before it turned around.

That’s the shortcoming of this model. It tells you if an area feels cheap. But it doesn’t tell you when the market will recover.

So, over a fixed 4-year period, this model doesn’t work 100% of the time.

Let’s continue to see what happens if you follow this model every 4 years.

In 2016, you would have invested in Whanganui (33% undervalued), spending about $150,000. Over the next 4 years, you would have made $145k.

That’s $106,000 more than if you bought the average property.

Then, in 2020, you would have bought in Christchurch (24% undervalued). You could buy a property for $525k back then.

3 years later, you would have made $174k. That compares to $67k for the average NZ property.

So, let’s add it up. Over 23 years, how much money did we make?

If you made the investments discussed in this newsletter, by 2023, you would have made:

That’s about a 50% better return. An extra million dollars.

Massive. What would that extra $1 million mean for you and your retirement?

Some people think, “just buy a property. It doesn’t matter where. She’ll be right, mate.”

The point of this newsletter is to show that this type of thinking could cost you $1 million.

That’s why, here at Opes Partners, we spend time looking at data so our clients and investors get solid returns.

If you want our help building a portfolio, you can book a free meeting with our team here.

We’ll help you create a property investment plan. Then we have New Build properties you can buy.

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser