Property Investment

The #1 mistake investors make

Everyone’s looking at past property growth, assuming past winners will keep winning. Here’s why that’s the #1 mistake investors make 👇

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

One of the most common questions I hear is: "Are there cashflow positive properties out there?"

In other words, a property where the rent covers all its own costs.

To find them, investors usually go hunting in smaller towns, where the prices are low, and the yields look high.

But here's the gotcha I always point out: high yield doesn't mean high profit. Those properties tend to come with higher costs, too.

Let’s look at a real property to see if the numbers stack up.

Last year, Ed – our economist at Opes – was on 1 News talking about Mataura. Home to the cheapest houses in New Zealand.

I jumped online and found this property. A standard 3-bed, 1-bath house. With an asking price of $335,000.

The next step is to find out how much the property could rent for.

Now, you can’t just look up the average rent for the area. Because you want to know the rent for the specific property you are looking to buy.

So I called a local property manager, who said the property could rent for $480–$510 a week.

If you use the middle of the range, that’d give this property a 7.7% gross yield.

That’s way higher than the country’s average. The average property investor gets a gross yield of around 4.5%.

And if you just looked at the back of the envelope maths and only thought about the mortgage, then this property would appear to pay its own way.

But in reality, there are lots of other costs to consider.

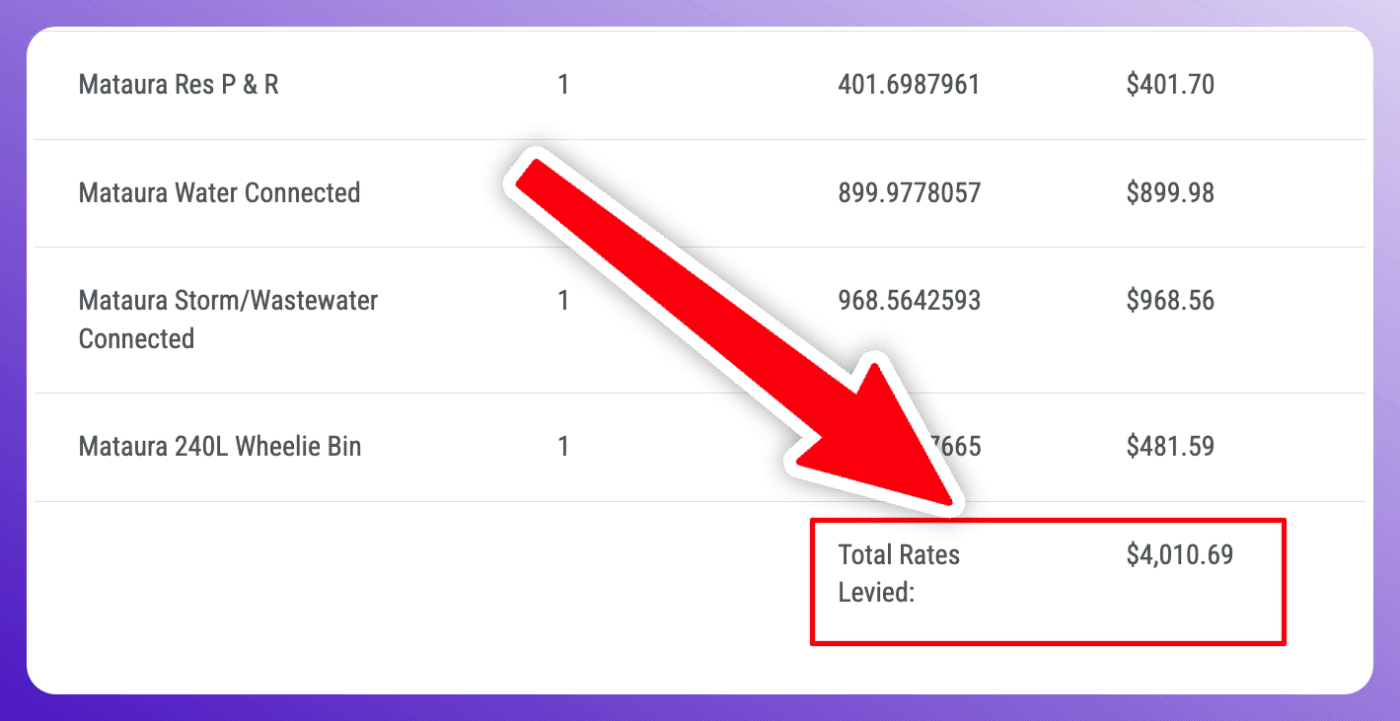

Running a rental property comes with lots of costs. So I found out the rates by jumping on the local council’s website.

The rates on this property were just over $4,000 a year.

For insurance, AMI estimated it’d cost around $3,100 a year.

That was based on a rebuild value of about $700,000 (even though the property was listed at $335,000).

That’s because insurers care about what it costs to rebuild the house, not what you paid for it.

You also need to think about your property manager, unless you live in the area. Sometimes, property managers in smaller towns charge a little bit more.

So while I had the local property manager on the phone, he told me he charged 9% +GST.

That’s slightly higher than the 8% (or so) you might see in a larger city.

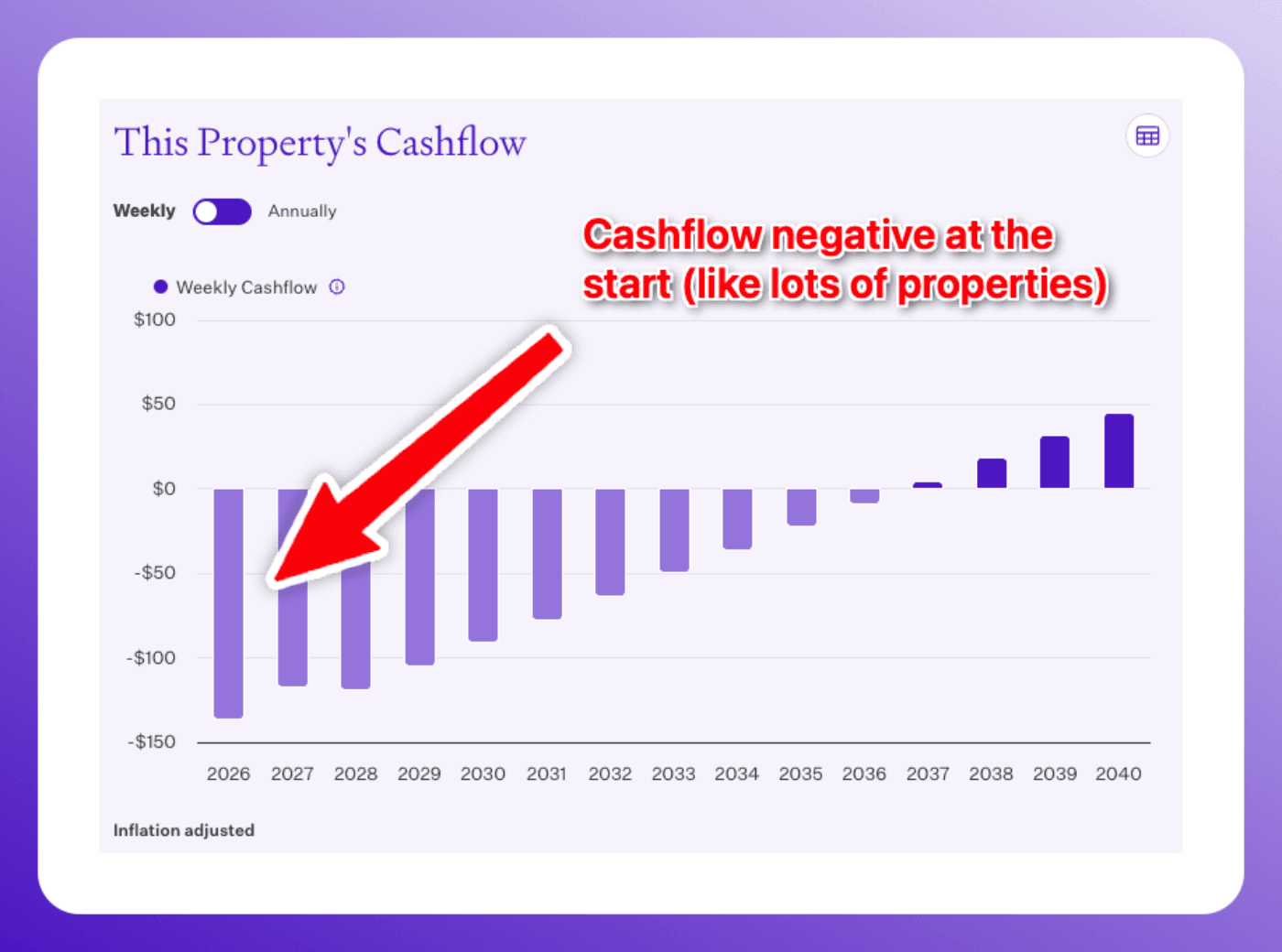

So now that we've got the price, the rent, and the main costs, we can finally calculate the cashflow.

The easiest way to do this is in Opes+, a free app for property investors.

What happens once we add in the rent and all the costs, including:

We can see that while the property earns a good yield (7.7%), the costs still make it cashflow negative by about $136 a week.

The point isn't to bag on this property or Mataura.

It’s to show you that even a high yield property can be cashflow negative if you borrow a lot of the money and factor in all the costs honestly.

Now, to be fair, there is a way to make the property cashflow positive. If you put in enough of the deposit; then the mortgage repayments will be lower, and the cashflow will be higher.

And if you could buy the property about $100k cheaper that’d tip it into cashflow positive territory.(Good luck with that 😅).

But the point of this newsletter is to say that gross yields (on their own) aren't enough to tell you whether a property has positive or negative cashflow.

The issue I see is that not enough investors actually investigate all the costs and run the numbers properly.

The truth of the matter is that most properties do require a top-up if you are honest about all of the costs.

That's not a bad thing. It's just the reality of investing in 2026.

Gross yields are vanity.

Cashflow is sanity.

P.S. Here’s the link to create your free Opes+ account to start running the numbers on investment properties the right way.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser