Property Investment

How long will it take for house prices to recover?

Everyone wants to know when house prices will recover. We ran the numbers. Here’s how long it could take 👇

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

I want to show you how to analyse a property.

Because investors are hunting for yield right now.

Mortgage rates have come down, but cashflow is still tight.

So when a property promises a high return, it's hard not to notice.

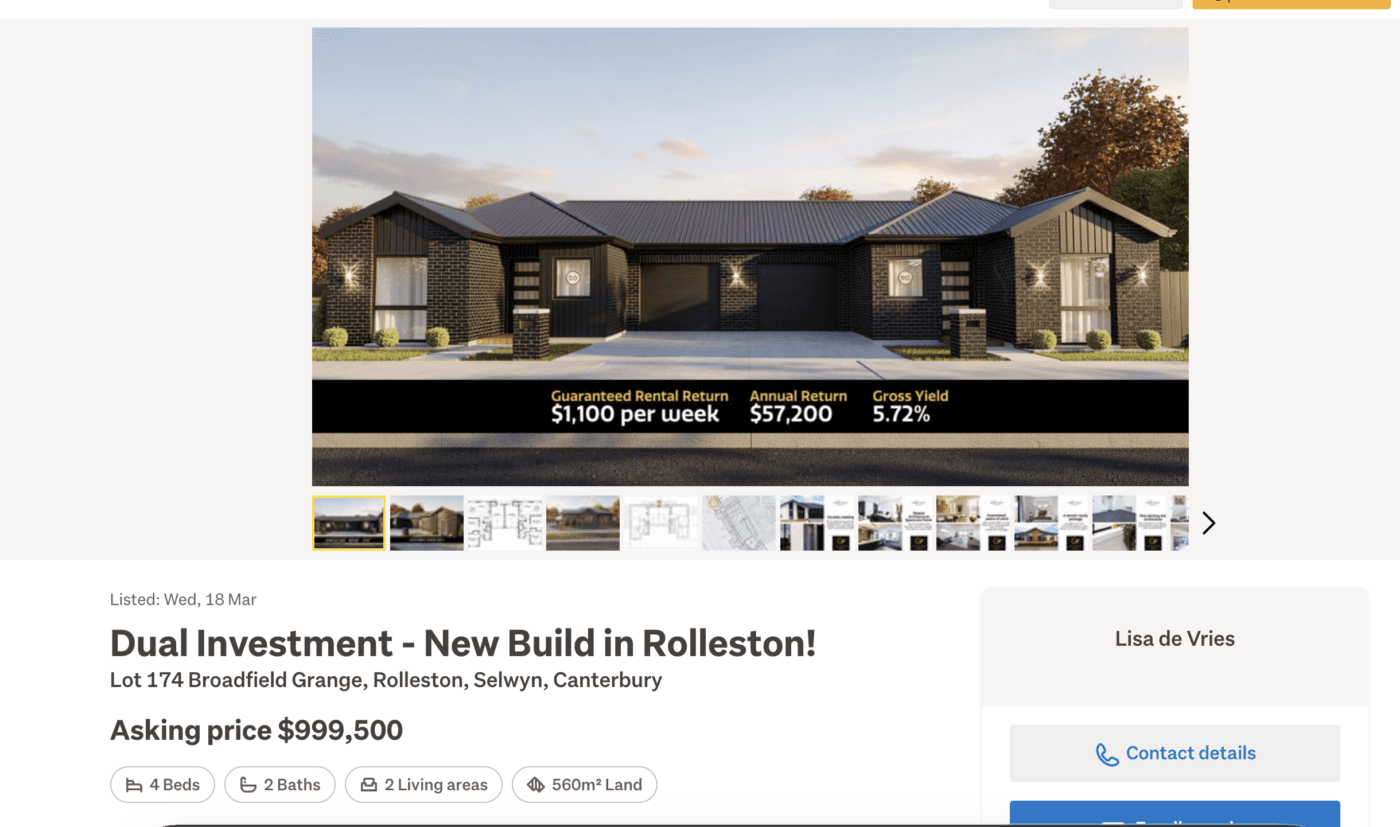

Recently, an investor asked me about this dual-key in Rolleston 👇 It's 2 homes on one title.

At first glance, it looks like what many investors want:

Now, I'm all for dual-key properties. And I'm all for Rolleston.

But before buying a property like this, do these 3 checks.

The first thing I'd do with any property offering a rental guarantee is check whether the rent stacks up in the real world.

Rental guarantees can absolutely be useful. We've used them ourselves at Opes in the past.

But remember, a rental guarantee is usually there so a developer can market a high gross yield, rather than to show you the true market return.

After all, the ‘guaranteed’ rent is often set above the true market rent.

In this example, the advertised rent was $1,100 a week ($550 for each home).

So I called Christchurch property managers.

Their view was that once the guarantee expired, a more realistic rent would be around $490-$520 a week for each property.

That's potentially a $60-a-week drop, per dwelling, once the guarantee ends.

That's $120 a week extra you might not have been expecting.

So that ‘5.7% gross yield’ is more like 5.1%.

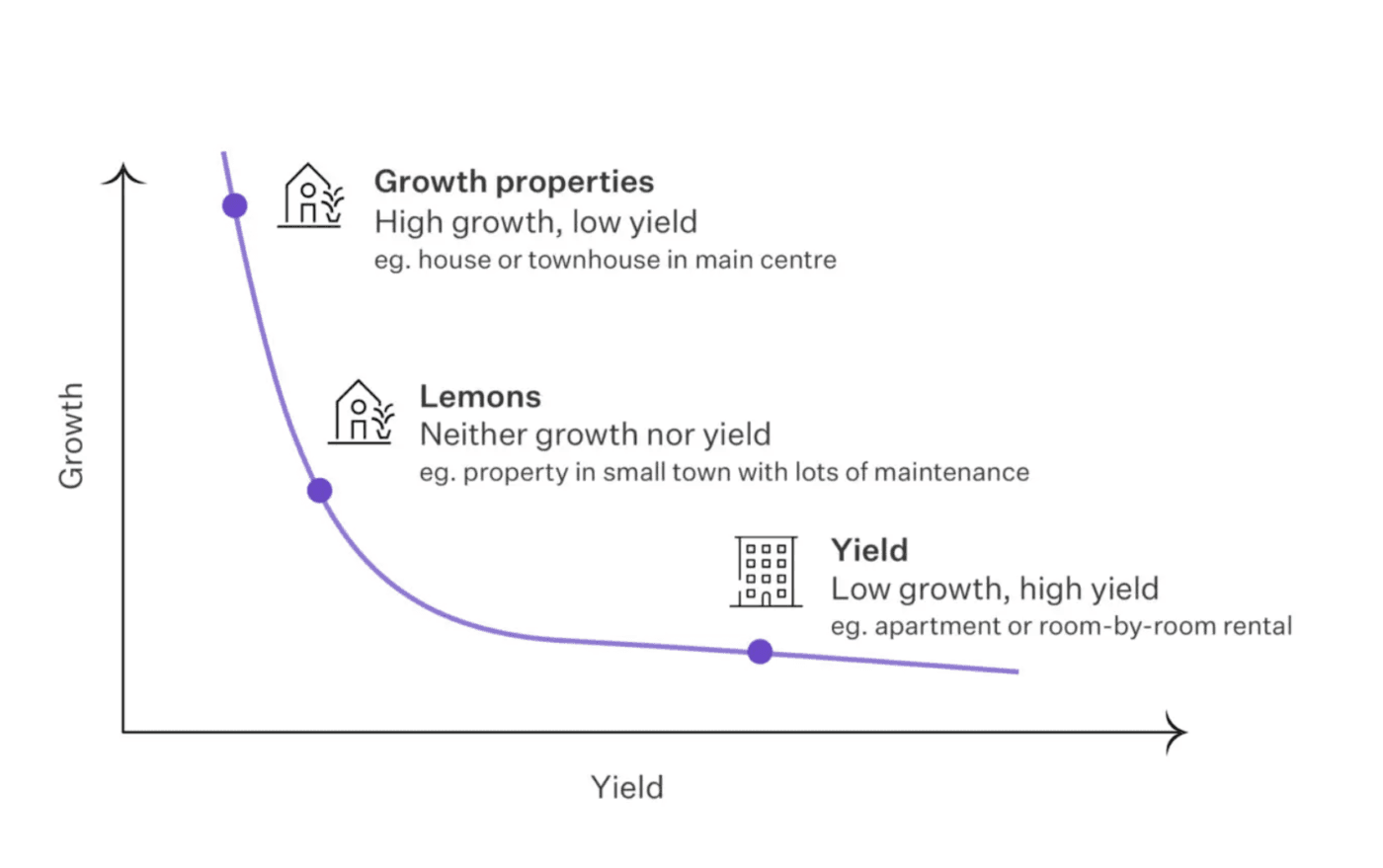

Every investment involves trade-offs.

Properties are either growth or yield.

Growth properties – tend to go up in value faster. But have lower rental yields.

Yield properties – tend to have better cashflow. But go up in value more slowly

There's nothing wrong with that.

In fact, I'm buying a yield property right now. It won't go up in value as fast but I'll get a slightly higher rent or return.

The trap isn't buying a high-yield property. It’s buying a Frankenstein that pretends to sit in the middle.

In this example, the actual yield is around 5.1%.

That's higher than a typical investment property. In my book, Wealth Plan, I discuss that a genuine yield property typically gets a 6%+ gross yield.

So for me, the yield is too low for this to be a true yield property. But it’s not a true growth property either, because it isn’t aimed at a typical family.

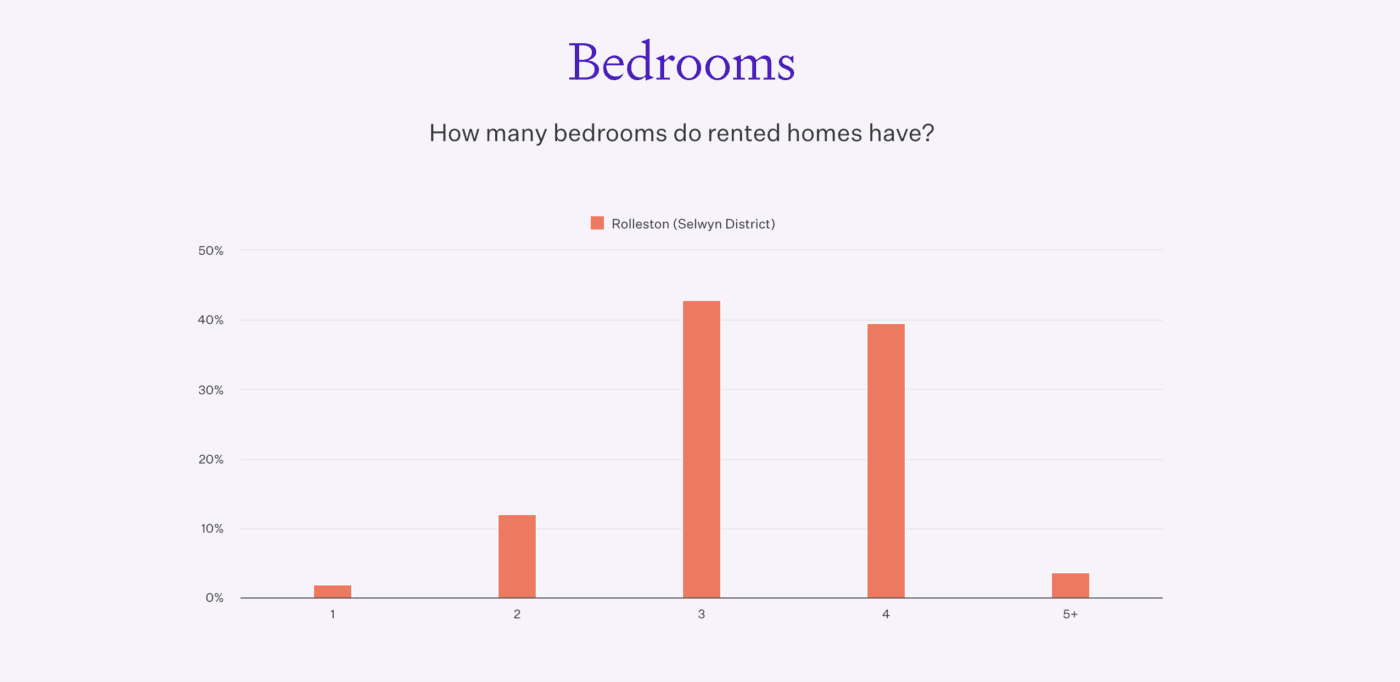

Before buying any investment property, think about who’s going to live in it.

In the case of Rolleston, the tenant pool is mainly families.

According to Stats NZ, over 80% of renters live in three- or four-bedroom homes.

And just over 10% live in 2-bedroom homes.

That makes me worried. If only 1 in 10 tenants live in the type of home you're buying …you might struggle to get a tenant.

Now, in some parts of the country, it's the other way around. 2 bedrooms are the most popular property type for renters, in those areas.

But that’s not the case in Rolleston.

You've got to match the property you’re buying with the location you’re buying in.

I'm not saying don't buy a yield property.

I'm not saying avoid dual-key homes, or avoid Rolleston.

It’s, before you buy, ask yourself:

And one more: could you buy two cheaper properties instead? You might get a similar yield, and spread your risk across two locations.

Because the highest-yielding deal on paper isn't always the smartest one.

Sometimes it's just the one with the most clever developer-spin.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser