Case Studies

Case study: We made $101,000 before our property was even built

Learn how a New Plymouth couple turned smart advice and timing into a six-figure win ... and what other investors can learn from their story.

Case Studies

7 min read

Author: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

These first-time property investors (Tim and Jo) were in their early 50s and wanted to start planning for their retirement.

Here’s how they plan to use investment properties to build $105,000 of passive income of (per year) by the time they hit retirement.

Everything in this case study is true to life (goals, salary, property prices, the Opes financial adviser they used). Only the names have been changed to protect their privacy.

Tim and Jo are 51 and 55 years old. They’re both self-employed and own their house in rural Canterbury. Both are self-employed. Tim’s been running his company for 20 years, and Jo is a midwife.

Because they’re both businesses, they both earn strong incomes. Together they had a household income of about $300k per year.

Up until this point, the pair focussed all their efforts on becoming mortgage free. They had an ambitious goal to wipe their $560,000 home loan clean in 5 years.

But, since they were also nearing retirement, they wanted to see whether investment properties could be used to prepare for the future.

The pair were first-time investors, and so wanted to work with a financial adviser to build a property investment plan. In the end, they decided to work with Stevie Waring from Opes Partners.

To create a property investment plan, you need to figure out what you’re investing for (your goals). Once you have your goals figured out, you can decide how ambitious your plan needs to be.

So, let’s get back to our couple. Tim and Jo had big, and specific plans for their retirement.

They wanted to:

Now, with any financial goal setting, it’s important to take these conceptual goals and assign some numbers to them.

What this means is: How much money do you need to make your goal a reality?

For instance, Tim and Jo’s wanted to be financially secure in retirement. But, in their eyes how much money do they need to feel financially secure?

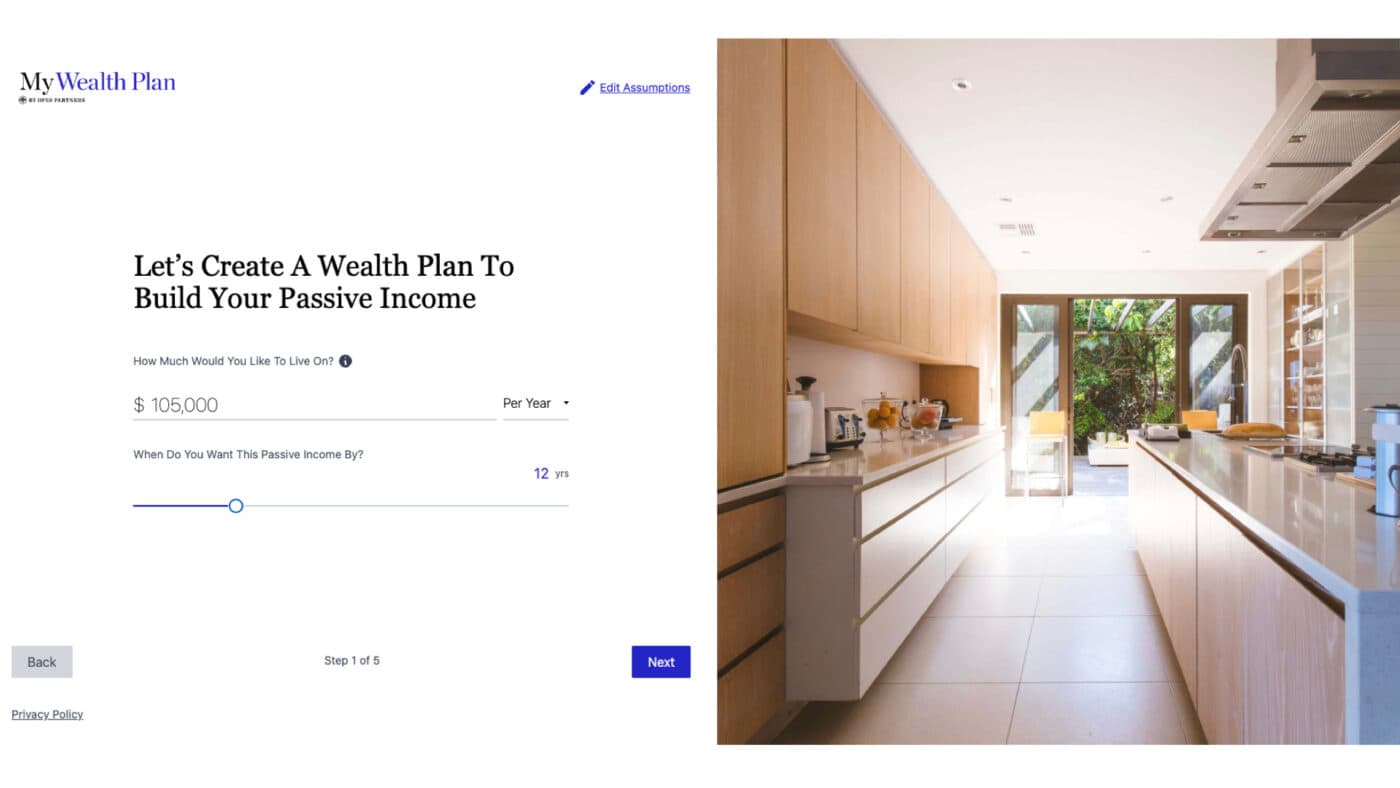

After an in-depth conversation, the pair decided they’d need $105,000 in income per year (before tax). That’s how much they’d need to maintain their current lifestyle. They also decided they wanted to retire in 12 years, once Tim is 67 and Jo is 63.

It’s important to point out that this is significantly lower than what the pair currently earn. However, $105k is what they currently spend per year.

That’s because, in retirement they won’t be paying a mortgage, so don’t need to earn as much as they do today (when they are paying a mortgage).

This is true for many Kiwis who are planning their retirement. There won’t be a mortgage, childcare costs, KiwiSaver contributions or the same need to save. So the amount you need to bring in each year to maintain your lifestyle will go down.

To achieve their $105,000 passive income goal, the couple would need $2.625 million of equity (net assets) by the time they hit retirement.

That’s assuming they’re not going to rely on the NZ superannuation, and that they can get a 4% net yield on those assets.

So, how did they make it work?

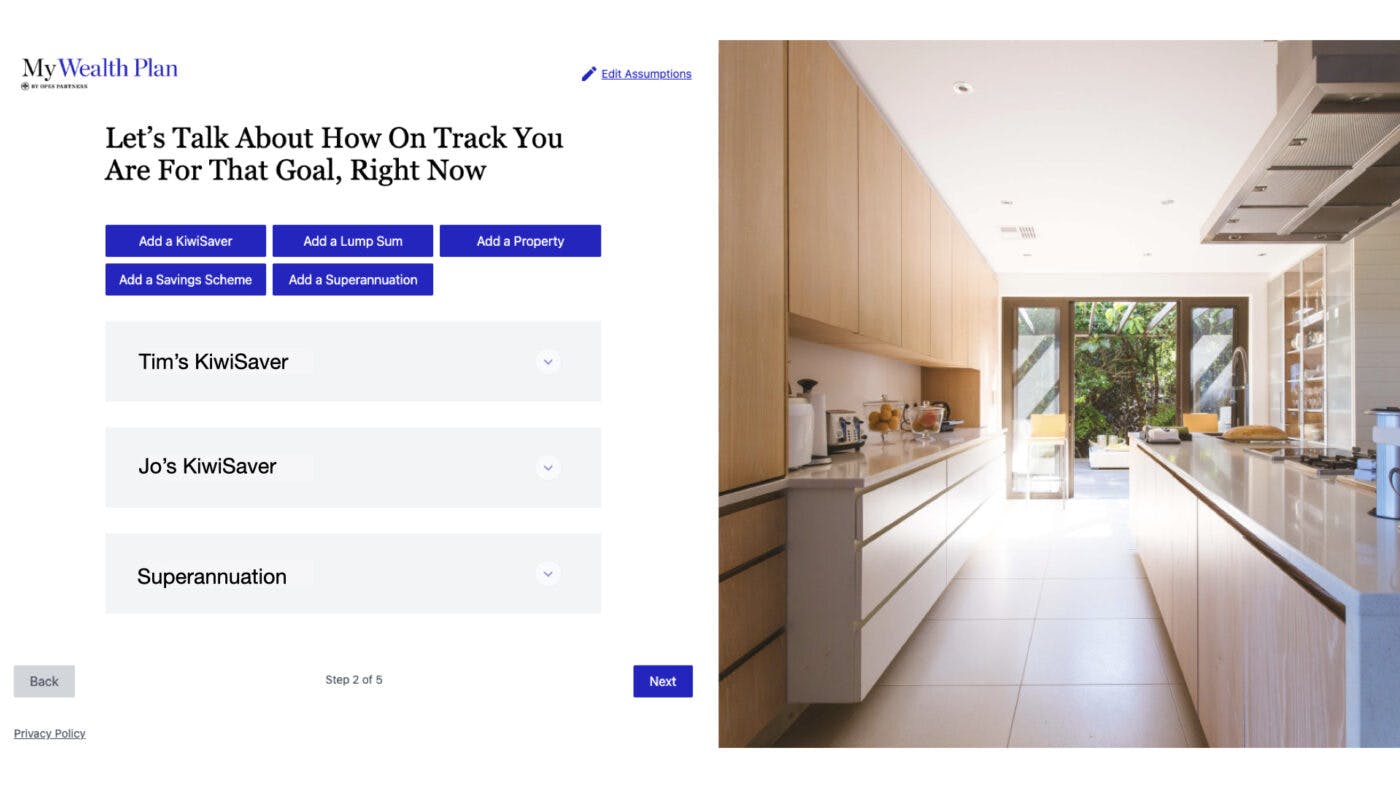

Once Tim and Jo had their goal figured out (build $2.625 million of debt free assets), they could figure out how close they’d be based on what they were currently doing.

Between the pair, they had $250,000 sitting in KiwiSaver. And they both planned to continue putting money into KiwiSaver up until they retired. So, this would get them part of the way there.

And because the pair were also close to retirement, they had the confidence to use the NZ superannuation (in its current form) as part of their plan.

This meant that if Tim and Jo did nothing else, they were already 60% of the way there.

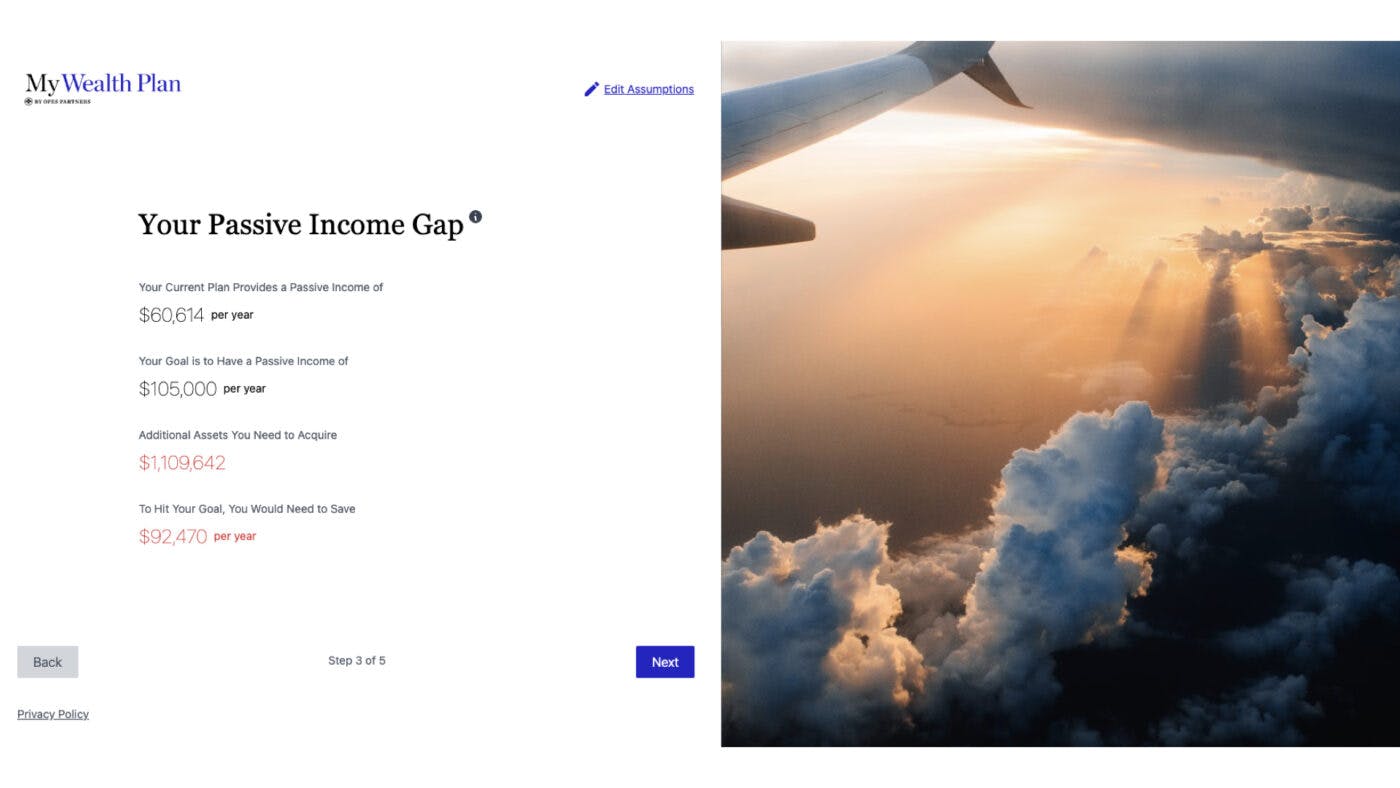

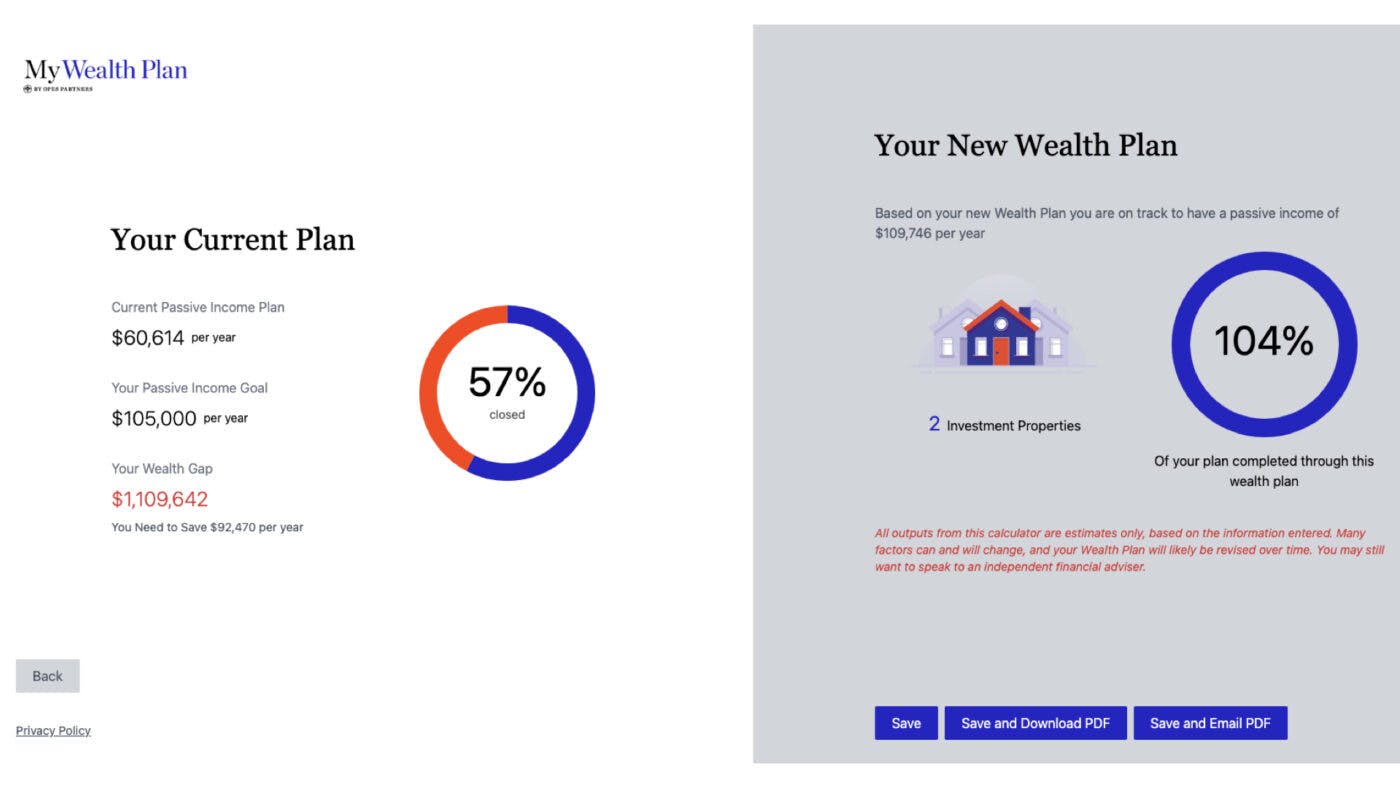

So, Tim and Jo had a Wealth Gap. There was a 40% difference between what they were on track to have and the $105,000 annual salary retirement dream.

If Tim and Jo did nothing else, they were on track for a retirement income of $60.6k per year. And while that’s not a bad income, it’s not what they wanted.

In total they’d be $1.1 million short of the assets they’d need to achieve their goal.

And if they were trying to save this money, they’d need to stash away over $92.4k per year, which wasn’t achievable.

It was time to figure out how property could be used to fill this Wealth Gap.

It’s a misconception that you need 10+ properties to retire well.

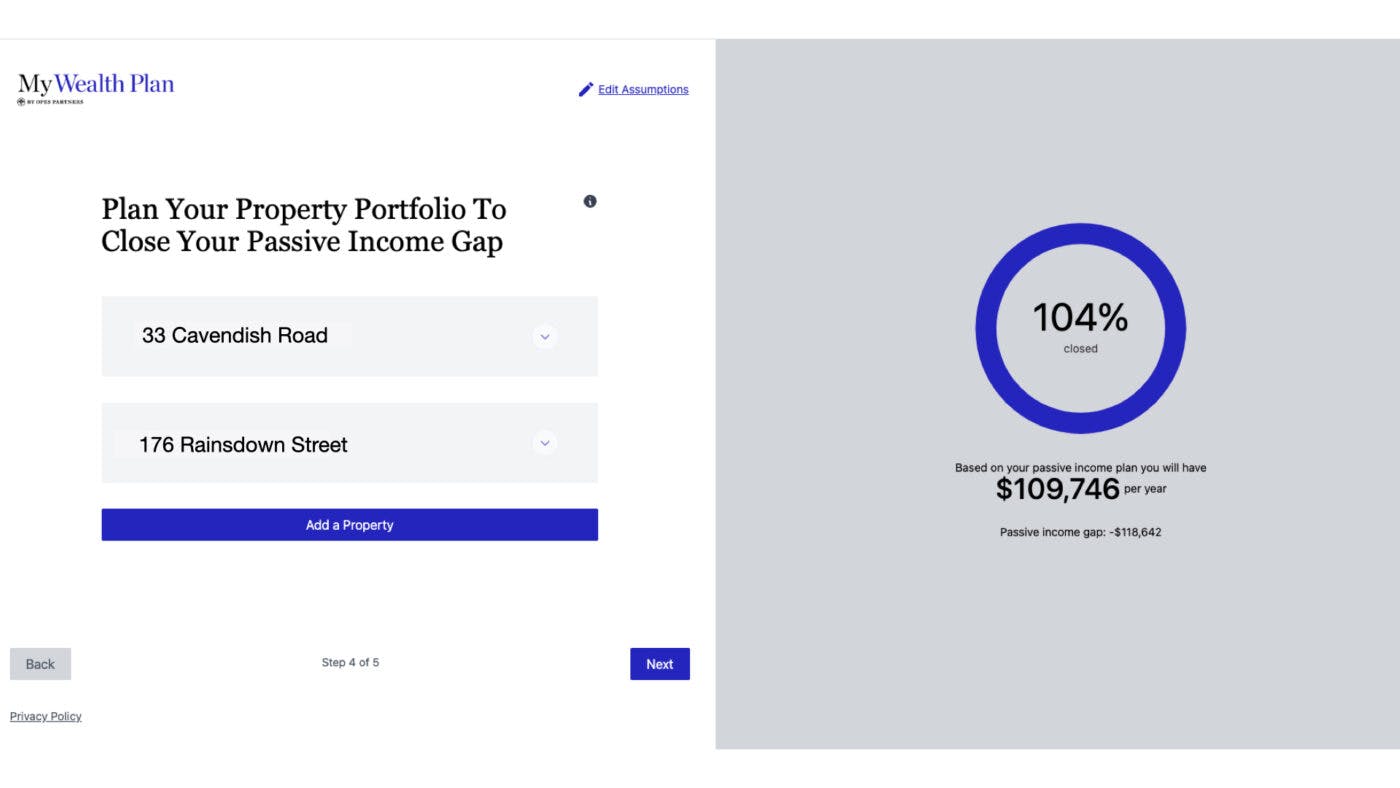

Tim and Jo used Opes Partners’ MyWealth Plan software to figure out that if they invested in just 2 properties, they’re forecast to achieve 92% of their goal.

Put simply, 2 properties are forecast to get them just shy of $100K in passive income. While not the full $105k, this was close enough that they wanted to get underway.

Together, they put together this plan with their Stevie – their Opes Property Partner:

Because Tim and Jo had decided to purchase a property in Christchurch, Stevie spent time selecting a few property options based in the Garden City.

These property options came from the 58 different developers (from around the country) that we have relationship with here at Opes Partners.

But, after looking at the properties, Tim and Jo paused.

As first time investors, they asked themselves: “What if we bought two properties now, rather than waiting another 2 years to get the second one?”

Afterall, they were in a good position, with equity and incomes. So they comfortable they could manage both purchases now, instead of waiting for the two year gap.

To make this work, they purchased a new-build townhouse in Christchurch that was close to being built.

They then put an Auckland property under contract that had a much longer settlement. This means they sign the contract, locking in today’s price, but with 18 months breathing room before the property was built and they would need to settle it.

When Tim and Jo re-ran their numbers with Stevie, bringing forward that purchase meant they would blow past their initial goal, and hit 107% of their passive income goal.

Up until this point, the couple had been channelling all their extra money into diligently paying down their mortgage, and had high hopes to pay the remaining $560K in the next five years.

But now they planned to have two extra properties, which would require them to invest money topping up the property.

Tim and Jo realised these extra properties were going to affect their mortgage goals, adding two years to their personal mortgage if they were to buy both investments straight away.

Jo and Tim decided to accept this trade-off, given that a secure retirement was more important to them than an extra 2 years paying a mortgage.

For Tim and Jo, the fact they were first time investors worked to their advantage.

Not only were they in a good financial position to begin with, but they also had plenty of equity to tap into.

It can be a scary prospect to take on two properties at once, especially when house prices are falling (like they are at the time of writing).

The next few years will likely see interest rates rise, before coming back to a more-normal level.

But in the meantime, investors like Tim and Jo are able to use the market to score a better deal than if the property market was rising.

While the couples still has work to do – paying off their mortgage, managing their property investment top-up, and contributing to KiwiSaver – they now have two things.

If you want the same service Jo and Tim got, your next step is to book a Portfolio Planning Session with us here at Opes Partners.

This is where you and a financial advisor will use the MyWealth Plan software to create a similar plan to Tim and Jo’s.

Free wealth plan session

Your next step is to book a portfolio planning session. This is where you and a financial adviser will create you a financial plan.

Book your free sessionJournalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Laine Moger, a seasoned Journalist and Property Educator holds a Bachelor of Communications (Honours) from Massey University and a Diploma of Journalism from the London School of Journalism. She has been an integral part of the Opes team for four years, crafting content for our website, newsletter, and external columns, as well as contributing to Informed Investor and NZ Property Investor.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser