Property Investment

How long will it take for house prices to recover?

Everyone wants to know when house prices will recover. We ran the numbers. Here’s how long it could take 👇

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

There's always something working for and against you in the property market.

You’ll never see a situation where everything is all rosy.

And there’s never a time when everything is all bad.

Right now, petrol prices are surging. Banks are tweaking their interest rates up. And there's a war in Iran that's making everyone nervous.

On the other hand, house prices just got their best result in 4 years. Net migration is turning around. And the rental market is starting to show signs of life.

Let's break both sides down.

Since the conflict in the Middle East kicked off, 91 petrol is up almost 50 cents a litre. Diesel is up even more. You’ll have noticed it at the pump.

So the first-round effect: you're spending more on fuel.

But it also has a second-round effect – and this is the one property investors should pay attention to.

When petrol gets more expensive, everything else tends to follow. It costs more to ship food to the supermarket. It costs more to get goods from the port to the store. Those costs flow through the whole economy.

If that feeds into broader inflation, the Reserve Bank might respond by increasing the OCR. And that would push mortgage rates up.

That’s, in part, why ANZ increased its 2-year rate from 4.89% to 5.09%. Interest rate markets think the war in Iran could cause the OCR to go up sooner than expected.

But then, just on Tuesday, Reserve Bank Governor Anna Breman gave a speech. She said that the RBNZ would likely "look through" the immediate increase in petrol prices.

She said that a temporary spike "can – and should – be looked through" if it's unlikely to impact medium-term inflation.

What the Reserve Bank will be watching is: Will the inflation stay at the petrol pump? Or does it spread?

That’s helped. Over the last couple of days, interest rate markets have calmed down a bit. The 1-year swap rate has fallen.

But it's not all doom and gloom. There are a few things I've been pointing out to investors that are quietly working in their favour.

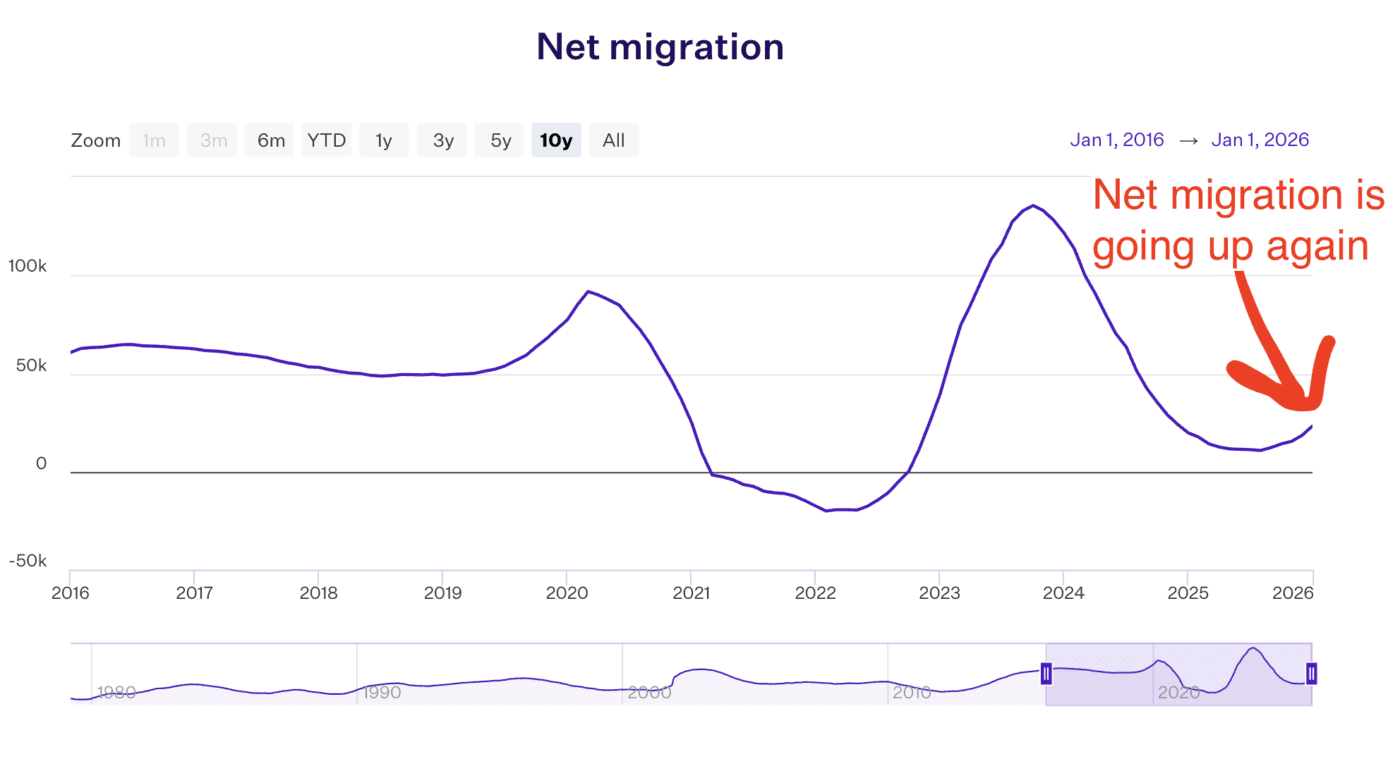

Net migration is turning around.

Remember six months ago, when the big story was Kiwis leaving New Zealand in droves? That tide is shifting.

More people are moving here. Fewer Kiwis are moving overseas. So the trend in net migration is getting better.

Net migration added 25,000 people to our population over the last year.

That's under the 20-year average of around 33,000. But it’s not that far off. And it’s going in the right direction.

House prices had their biggest monthly jump in 4 years.

REINZ data for February showed house prices lifted at the fastest rate we've seen since late 2021.

It's too early to call it a trend. But the market is looking less grim than it did 6 or 12 months ago.

The rental market is coming back to life.

We're seeing a slight easing in the number of landlords who say it's hard to find a good tenant.

If I look at our own property management company, properties are renting quicker than they were.

And the median rent went up from $590 to $610 over the last 6 months. (Tenancy Services Jul ’25 – Jan ’26).

This is the second-highest the median rent has ever been.

Almost a year ago to the day, I wrote a newsletter about Trump’s tariffs. At that time, investors were worried that it would tank the markets. (It hasn’t).

That newsletter has this graph showing NZ house prices against a number of major shocks.

What do you see?

Major events come and go. But if you're in it for the long term, property prices tend to go up over time:

If you're an existing investor – or you're thinking about getting started – it's important to look at both sides.

You don't want to bury your head in the sand and ignore the risks. But you also don't want to spook yourself out of making a long-term decision.

I'm not playing down the risk of higher interest rates coming from the war in Iran. I'm not dismissing the fact that we're all paying more for petrol.

But yesterday's problems have a habit of becoming tomorrow’s fish and chip wrapping.

There's always something working for you, and something working against you. The trick is making sure you're looking at both.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser