Property Investment

How long will it take for house prices to recover?

Everyone wants to know when house prices will recover. We ran the numbers. Here’s how long it could take 👇

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

Private Property – our weekly newsletter that gives you insights into what's happening in the NZ property market. Written by managing director Andrew Nicol. Sign up to receive this in your inbox every Thursday.

It happened. Again.

Yesterday, the Reserve Bank increased the OCR. While an increase was expected.

The size of the jump surprised economists.

It was an 0.5% increase rather than the projected 0.25%.

National’s Nicola Willis called it a ‘punch in the guts’ for Kiwis with mortgages.

But is it the knockout blow to interest rates you might think? Here’s why interest rates won’t increase (at least not by that much).

Many people think a higher OCR = higher interest rates. That’s not always how it works.

OCR hike ≠ interest rate hike

6 weeks ago, the Reserve Bank lifted the OCR by 0.5%. But since that increase, interest rates have come down:

– ASB’s 1-year rate fell by 0.2%

– BNZ has been offering cracker deals at 4.99%, and

– ANZ has been discounting their interest rates for some investors we’re working with

The purpose of the OCR increase is to stop that from happening. The Reserve Bank wants banks to:

1. Keep mortgage interest rates where they are

2. Increase their deposit rates

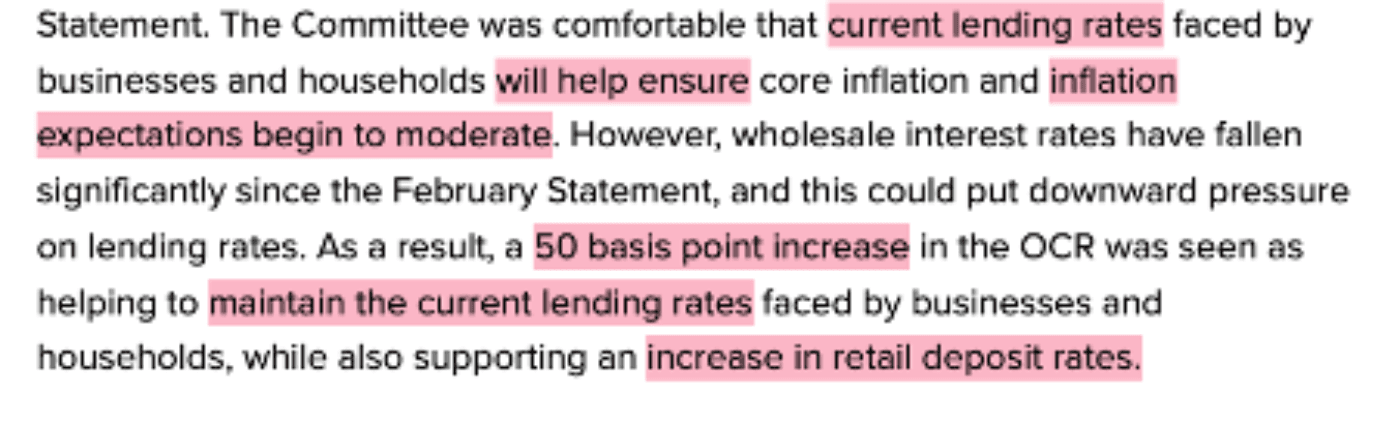

Take a look at the Reserve Bank’s own press statement –

The Reserve Bank thinks the current mortgage interest rates are enough to tackle inflation.

The increase in the OCR is to keep these rates where they are.

Banks don’t (usually) borrow cash from the Reserve Bank to lend you money for your mortgage.

Instead, they get the money from:

– their own funds,

– wholesale money markets and from

– term deposits

And since the most recent OCR increase, the 1-year wholesale interest rate had gone down!

It was getting cheaper for the bank to borrow from someone else and lend to you for your mortgage.

This is what’s allowed banks to put their interest rates down (even though the OCR went up).

Since yesterday’s announcement, the 1-year wholesale rate has returned to where it was after the previous OCR announcement.

On top of this, the banks have seen their margins increase. This is partly because mortgage interest rates have risen faster than term deposit rates.

That increase in margin allows the banks to decrease their mortgage interest rates sooner than the Reserve Bank wants.

And that’s why the central bank has surprised us.

If they only increased the OCR by 0.25% (as expected) … they’re worried that:

– mortgage interest rates will fall too soon,

– that we’ll start spending more,

– and that inflation will stick around for longer.

Here at Opes, we’ve predicted that the 1-year mortgage interest rate will hit 7% in April.

If you compare that to ANZ’s most recent forecast … they suggest that interest rates have already peaked at around 6.6%.

We’re sticking with our 7% projection for the 1-year rate. And are not changing this projection based on yesterday’s hike.

And that’s because while the Reserve Bank surprised us with its increase … the endpoint is still the same.

The Reserve Bank expects the OCR to peak at 5.5% later in May. That’s the same as what they’ve been projecting for the last 4.5 months.

The endpoint hasn’t changed. We’ll just get there faster than first thought.

And because of this, I’m not expecting a significant jump in interest rates.

But of course, that’s all based on the current data I have available today. New inflation data comes out in 2 weeks. That data will influence what happens to interest rates over the next year.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser