Property Investment

Are you on track for the retirement you want?

Most Kiwis have no idea if they'll have enough to retire. Here's how to find out 👇

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Private Property – our weekly newsletter that gives you insights into what's happening in the NZ property market. Written by managing director Andrew Nicol. Sign up to receive this in your inbox every Thursday.

“Aaaargh!!! 50 basis points!! Our rental cashflow is going to take a hammering!”

This is an actual text I received yesterday, from one of my investors.

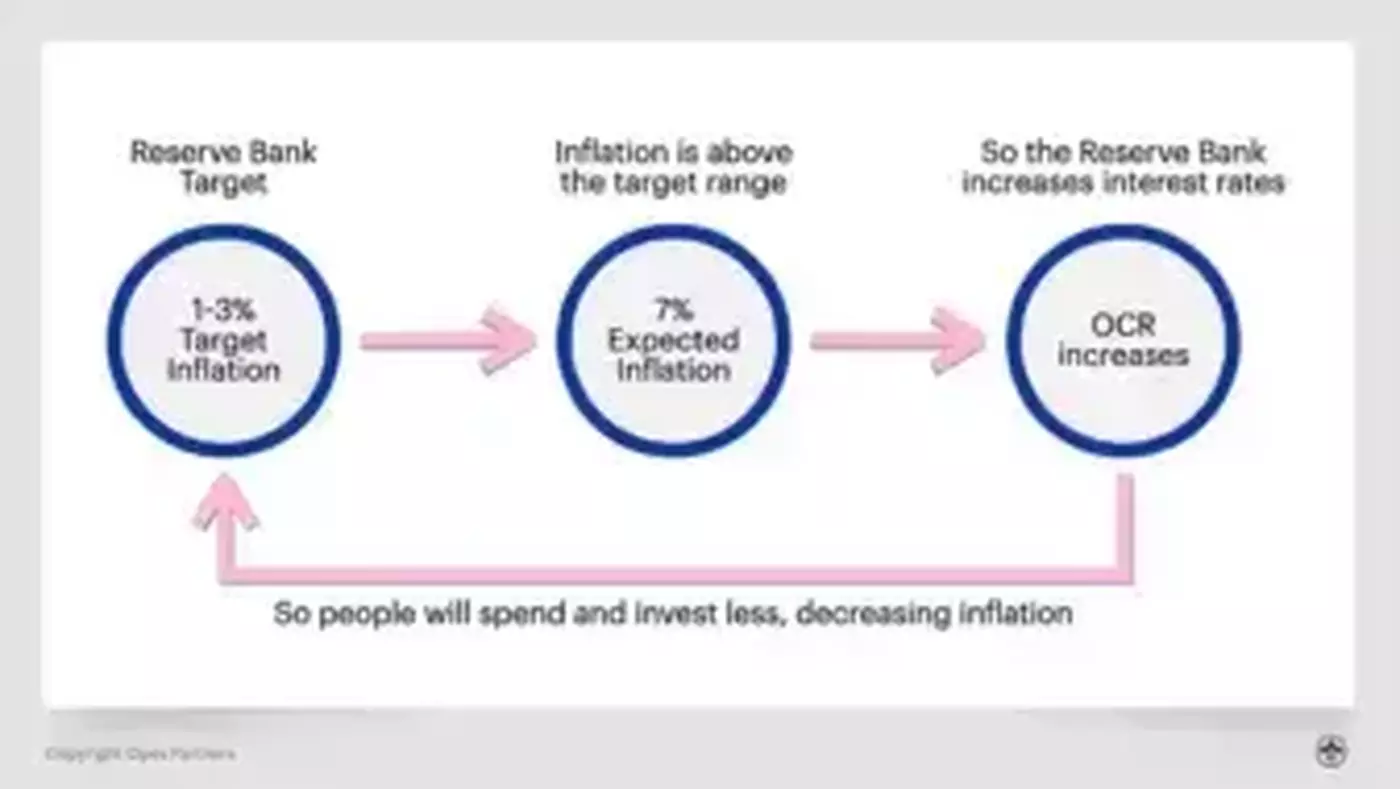

That’s because the Reserve Bank announced they will lift the OCR by 0.5% (to 1.5%).

They’ve made this move to fight inflation and the rising cost of living – which is expected to peak later this year at 7%.

Before we talk about what higher interest rates mean for you as an investor – here's a quick summary of why the Reserve Bank made the move.

Though the rise was widely predicted, investors naturally get nervous … especially when every news website runs scary stories about higher rates.

But, while there are some reasons to worry about rising interest rates, there are also reasons to remain calm.

Let’s go through both lists.

1. Interest rates will climb faster than expected

You may start paying a slightly higher interest rate sooner than expected.

However, this will hit different investors in different ways. That's because it depends on how long you have fixed your term for, and when your interest rate comes up for renewal.

Regardless, higher mortgage costs will undoubtedly soak up more of your investment property’s cashflow.

When interest rates climb, investors start to feel nervous. This could mean that some buyers will delay getting into the market, which will cause house prices to soften.

This means capital gains will be confined to only certain parts of the country over the next 12-18 months.

The Reserve Bank’s plan was always to increase the OCR to its current level at some point. If not now, then in 6 weeks.

What hasn’t changed is where they think the OCR will end up. This remains at 3.25%.

The endpoint is the same. Rates are still rising as expected, but now it’s happening slightly faster than we thought 6 weeks ago.

Be prepared for further interest rate rises. They are coming (Dun dun dun).

When you took out your mortgage, the bank tested that you could still afford all your debt repayments … even if interest rates were 6.7%-ish and on principal and interest.

So, if your investment mortgage is on interest only and is currently fixed at 2.5%, you can afford significant rate rises under the bank’s modelling.

That is probably of little comfort since paying more towards your mortgage will mean saving less or tightening your belt …

But the bulk of borrowers can afford significant interest rate rises before the market starts to creak.

The Reserve Bank is raising interest rates to tackle high inflation. Once this has been attacked, rates will track down again.

The bank’s own guidance suggests the OCR will rise to 3.25% before sliding back to around 2%.Well known economist,

Tony Alexander, gave the following ballpark predictions following yesterday’s announcements.

Some investors will feel a bit of pain. But the pain will be temporary. The pain will pass.

Right now, the prospect of higher interest rates is scaring some buyers off. Developers are struggling to sell their own projects. This means, I am out there negotiating deals.

Last week my colleague Ed was on The Project (on TV3) talking about a deal I’d just negotiated. One of my investors has just bought a townhouse with a valuation of $1.24 million but will pay only $999k.

That means they’ll make $250k in equity by signing the deal. Interest rates will have to rise substantially before these deals are worth losing.

While property prices will slide over the next 18 months…they won’t crash.

Partly, this is because investors aren’t clamouring to sell.

But it’s also because:

Investors will continue to hold, at least until they get out of the bright-line period. The dip will largely be over by the time that happens, and sentiment will improve.

The bottom line is interest rate rises won’t be pain-free but they will be bearable. Just keep your eyes on your longterm future goals, knowing any short-term pain will be worth it for the long term gain.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser