Property Investment

Can you predict next year’s best-performing property market?

Everyone wants to know which property market will boom next. The truth might surprise you 👇

Property Investment

3 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Interest rates are high. So lots of investors ask: “Does property investment still make sense in 2024?”

One investor said: “With high interest rates and the rent we get, is it worth buying an investment property? Most of the time, we spend money from our pocket to cover the mortgage repayments.”

That is such a good question. You don’t want to buy an investment property and find it doesn’t give you a good return.

So, let’s dig into the numbers to see if it’s worth it.

At today’s interest rates, the rent doesn’t usually cover all your expenses.

So, you have to make up the difference by "topping up" the property out of your own pocket.

While interest rates are high, this is usually between $300 - $600 a week.

Doesn’t matter whether it’s new or existing. If you don’t have a cash deposit, Valocity estimates that over 9 in 10 investors top up their new purchases.

So it’s fair to ask – is spending that money worth it? Will I get a return? And how much might house prices go up in 2024?

No one knows exactly how much house prices might go up next year.

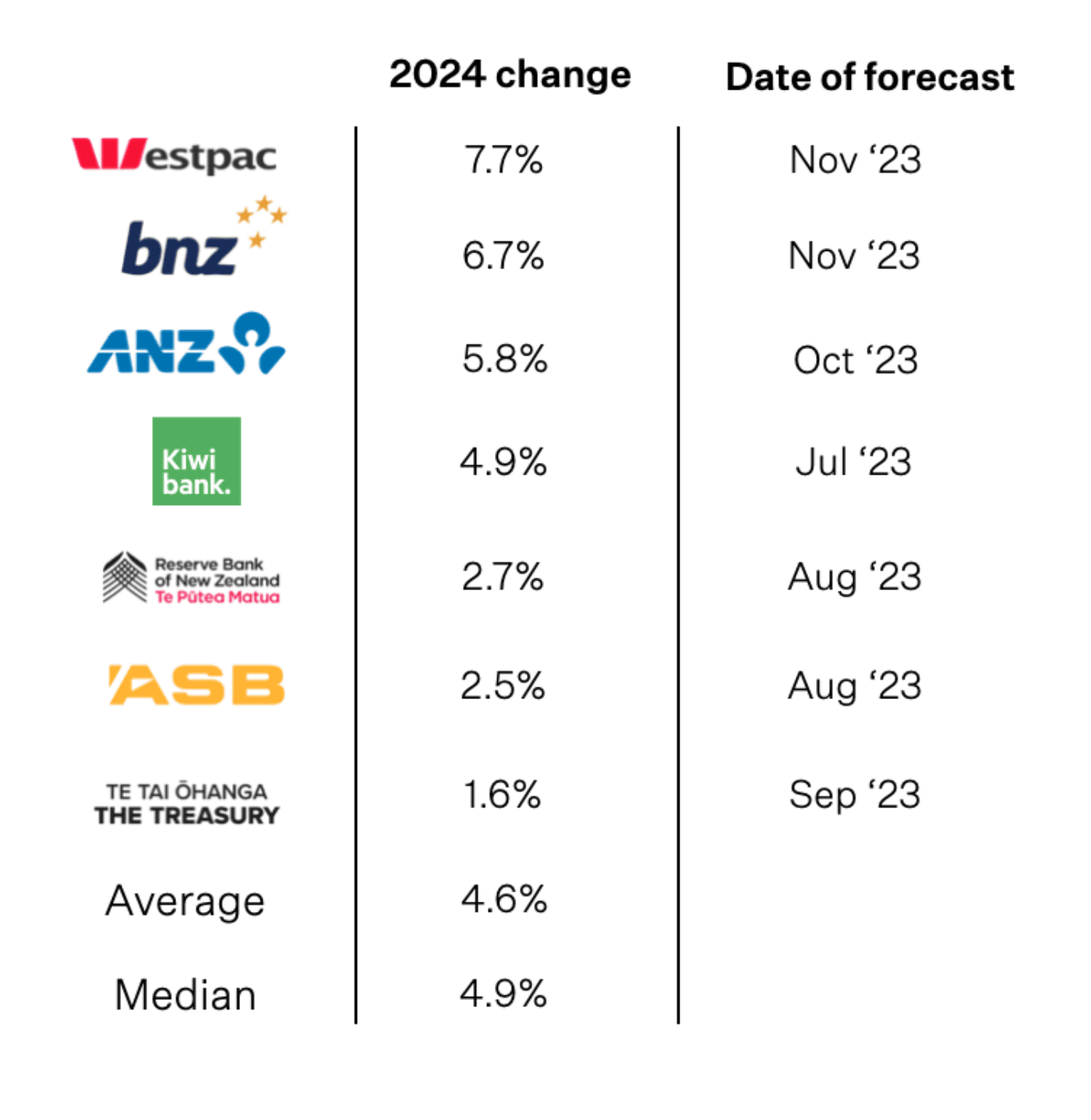

But getting a range of opinions can give us a sense of what might happen. Here’s what the main banks think will happen.

Westpac is the most aggressive. They think house prices will go up 7.7% next year. ASB is a bit more conservative. They say 2.5%.

The median forecaster says 4.9%.

So what would happen if you bought an $800k property in Auckland and it went up by 4.9% next year?

By the end of the year, it might be worth $839,200. You made $39,200.

To hold that property, you probably would have had to invest about $25,000 in cash to hold that property.

So you put in $25k, and if KiwiBank is right, you get out $39.2k.

That’s a 56.8% return on the cash you put into the property.

Here’s what the returns would look like based on other bank’s forecasts.

What if ANZ’s forecast is right? House prices go up 5.8%. You've put in $25k and made $46.4k. An 86% return.

But if ASB is right, house prices go up by 2.5%. Then you put in $25k and get $20k back. So you didn’t make money.

This is the good and the bad of investing in property and using debt.

You can make massive returns because you buy a really valuable asset (a house). Then, you keep all the gains when it goes up in value.

But if property prices don’t go up, you can spend money and not get a return.

But it’s not the coin flip it might sound like.

Property prices can go up or down. But they go up more often than not.

Auckland properties have about a 70% chance of increasing in value in any given year. That’s by our number crunching.

And that chance appears to be better in 2024 since the property cycle is turning.

Property prices have already increased 2.8% since May 2023 (REINZ).

So, my view is that ASB’s 3-month-old forecast is a bit pessimistic. We’ll find out where their heads are at when they release an updated forecast within the next month.

So, is it still worth investing in 2024?

If Westpac’s, ANZ’s, BNZ’s or KiwiBank’s forecasts turn out right, yes. Investing in property could make sense for you.

A 57% return on the cash you put in seems like a good return to me.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser