Wealth

Property vs shares vs funds vs term deposits

In this article, you’ll learn which asset class earns the highest return based on the top-up you would usually put into your investment property.

Wealth

9 min read

Out of the major banks Rabobank currently offers the highest 12 month fixed term deposit interest rate at 3.95%.

As at Thursday 02 July 2026, the highest 18 months fixed term deposit interest rate is 4.00%. This is currently offered by 8 banks. They are .

The highest 2 year fixed term deposit interest rate is 4.30%. This is currently offered by 2 banks. They are Heartland Bank and Westpac.

The highest 3 year fixed term deposit interest rate is 4.50%. This is currently offered by 5 banks. They are BNZ, Co-operative Bank, Heartland Bank, SBS Bank and TSB Bank.

Heartland Bank currently offers the highest 4 year fixed term deposit interest rate at 4.75%.

The highest 5 year fixed term deposit interest rate is 4.90%. This is currently offered by 3 banks. They are BNZ, Heartland Bank and Rabobank.

These interest rates were last updated on Thursday 02 July 2026.

The interest rates we've stated are accurate to the best of our knowledge at the time of writing. Interest rates are ever-changing, so be sure to double check with your bank before locking in your interest rate.

A term deposit is an investment that generates income. You take your money to a bank and lock it away for an agreed length of time … it might be 3 months, 6 months or a few years.

And in return, you get a fixed return on your money.

For example, if you have $10,000 available, you can choose to put it into a term deposit at say 6% for a year. That means the bank will pay you $600 in interest. At the end of the term, you get $10k back – plus the $600 return.

Term deposits can be a good way to generate income from your money as long as you don’t need access to that cash in the short term.

Even better, you can get paid that return regularly. You can say, “Here’s my money, can you please pay me the return every quarter?” Some banks will even pay monthly.

So in the case of $10k (above), you could get paid $150 every three months.

The interest rate you receive depends on two things:

Most of the time the longer you lock in, the higher the return. On the other hand, the riskier the lender you go with, the higher the return.

Once you’ve locked it in, the rate stays the same for the entire term. That’s great, because you know exactly what your return will be.

Compare that to alternatives like managed funds or shares where you don’t know the return you’ll get in advance.

So, term deposits are lower risk. You get certainty. That’s why they appeal to conservative, low-risk investors.

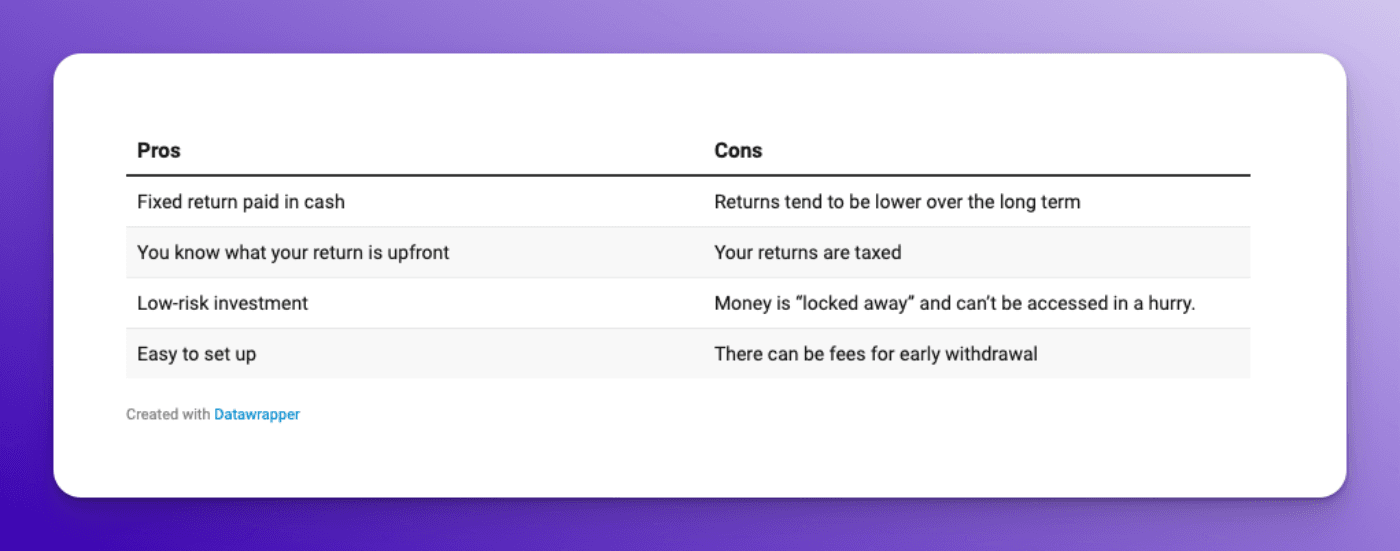

There are pros and cons to term deposits as an investment option. Let’s go through them both.

If you like certainty, or want to sleep at night knowing your money is safe, term deposits can be a good option.

There’s no guessing what your return will be. You get a fixed interest rate set from the get-go. This means you know exactly how much your investment will make, and your return is paid in cash.

And since they’re considered a low-risk investment, there’s little chance of losing money. That’s especially true now that the Depositors Compensation Scheme is coming in.

From July 1 2025 your term deposit is guaranteed up to $100,000.

That means that if you invest $100,000 in a term deposit with a bank, and then that bank goes belly-up, you get your $100,000 back.

Term deposits were already low risk, and this makes the risk even lower for many investors.

Term deposits are also easy to set up. You can do it all through your online bank account without having to speak to anyone. There are no physical forms or signatures.

But, it’s not all upside. Term deposits have some important downsides too.

At the same time, your returns from fixed interest are generally lower than if you invested in a managed fund or shares. That’s because lower-risk assets tend also to get lower returns.

On top of that, your returns are also taxed. For example, if I get a 6% return on a term deposit, this is reduced to 4% once I pay tax (assuming a 33% tax rate).

Then, your returns are further eroded through inflation.

So, if you get a 4% after-tax return and inflation is 2%, your real after-tax return is just 2%.

That’s why term deposits are a good way to generate income but are not generally a good way to build your wealth.

And remember that if you invest in a term deposit, your money is temporarily locked away. You can’t access it in a hurry.

If you need access to the money, like in an emergency, you may have to pay a penalty and wait a certain number of days before it’s released.

Some term deposits also charge fees for early withdrawals, which means you could end up with less than you expected. That’s if you need to access your money before the term ends.

The Official Cash Rate (OCR) is the Reserve Bank’s key tool for controlling inflation.

When inflation is high – like in 2022 when it hit 7.3% – the Reserve Bank raises the OCR. This makes it more expensive to borrow and more profitable to save.

That slows the economy down as people spend less.

From 2021 to 2023 the Reserve Bank hiked the OCR from 0.25% to 5.5%.

A higher OCR means it costs banks more to borrow money. So, banks increase their term deposit rates. So when the OCR is high, term deposit rates are high. When the OCR drops – term deposit rates fall too.

So, if you’ve noticed your term deposit rate changing, it’s likely because the OCR is moving.

Savers loved the high interest rate era.

At 6%, a $100,000 term deposit earned $6,000 in a year. But if that rate falls to 4%, the same deposit only earns $4,000. This is why falling interest rates benefit borrowers but hurt savers.

One thing that often confuses people about term deposits is tax.

Yes, your interest rate is fixed – say 4% or 5% – but that return isn’t yours to keep in full.

Term deposits earn income. When you earn income – you pay tax.

This is taxed at your marginal income tax rate.

This works through something called Resident Withholding Tax (RWT). It’s the tax your bank deducts from your interest before paying the rest to you.

You tell the bank your RWT rate, and it should match your marginal tax rate.

If it doesn’t — and your income pushes you into a higher bracket — you might owe the IRD more at the end of the tax year.

Banks are supposed to take care of this automatically, but that doesn’t mean they always get it right. Sometimes they deduct too much, and you get a refund later. But if they deduct too little, you’ll end up with a surprise tax bill.

That’s exactly what happened to me. A few years ago my dad gave me a pretty big lump of cash towards my house deposit.

The house wasn’t ready for 18 months, so I put the money into term deposits earning 5.5%. I made over $7,000 in interest. Great, right?

Not so fast. At tax time, I got a $1,000-plus bill from the IRD.

Turns out the bank had been taxing me at 17.5%, but my actual tax rate was 33%.

I called IRD to ask how that could happen. Surely the bank would know what rate to apply, but I didn’t realise it was my responsibility to check.

So, the moral of the story: check your RWT rate with your bank. Update it if needed, and don't assume everything will be OK.

So, aside from checking that your RWT rate is correct, there’s another way to save on tax: investing in PIEs.

No, not mince pies, a Portfolio Investment Entity (PIE). This works much like a regular term deposit. But there’s one big advantage – the tax rate is lower. While interest from a standard term deposit is taxed at your marginal rate (which could be as high as 39%), PIE term deposits are taxed at a capped rate of 28%.

This tax rate is called your Prescribed Investor Rate (PIR), and it’s based on your income. If you earn over $48,000, a PIE could lower your tax from 30–39% down to just 28%. Those savings can add up.

For example, take that $7,000 in interest I got from my term deposit. At my marginal tax rate of 33%, I owed $2,310 in tax. If I’d used a PIE instead, I would have only paid $1,960.

That’s an extra $350 in my pocket.

And since PIE tax is final, I wouldn’t have faced a top-up bill at the end of the year either!

PIEs work best for higher earners, particularly those making over $70,000. If your income is below $48,000, the tax savings are smaller or non-existent.

Just keep in mind, PIE term deposits can sometimes offer slightly lower interest rates or less flexibility, so it’s worth comparing your options before locking anything in.

Different banks offer different term deposit interest rates. Here’s why:

Big banks (like ANZ, BNZ) often offer lower rates. Smaller banks and non-bank lenders offer higher rates to compete. That’s because they are smaller and slightly higher risk.

Banks with lower credit ratings are seen as riskier, so they offer higher rates to attract deposits (more on this below).

If a bank needs more money so they can lend money out, it will offer higher rates to bring in deposits.

So, should you always go with the bank offering the highest return?

Tempting, I know, but not necessarily the best move. Higher rates usually mean higher risk. And that leads to the next obvious question: how do you know which banks are riskier?

Term deposits themselves aren’t graded, but the banks behind them are.

Credit rating agencies rank them in much the same way your high school exams were marked.

A top-tier AAA rating means the bank is very safe and very unlikely to fail.

At the other end, a rating of BB+ or lower means there’s a higher risk involved, and you might want to think twice.

A bank’s credit rating gives you a good indication of how safe your money is. The higher the rating, the more secure your deposit.

Most banks list their credit ratings on their websites, so it’s easy to check before you lock in a term deposit.

Find out how property stacks up against your savings rate in a free, no-obligation session with a financial adviser.

Book your free session

Mortgage broker for over 10 years, property investor and Managing Director at Opes Mortgages

Peter Norris, a certified mortgage adviser with 10+ years of experience, serves as the Managing Director at Opes Mortgages. Having facilitated over $1.2 billion in lending for 2000+ clients, Peter is a respected authority in property financing. He's a frequent writer for Informed Investor Magazine and Property Investor Magazine, while also being recognized as BNZ Mortgage Adviser of the Year in 2018 and listed among NZ Adviser's top advisers in 2022, showcasing his expertise.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser