Number Crunching

What is a good gross yield in New Zealand? [2026]

Find out where the highest and lowest gross yields in NZ are for property investors. This article breaks down the data so you can make better decisions.

Property Investment

6 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Properties with high yields don’t always make you as much money as you think.

Everyone wants to make as much money as possible. So, if a property advertises a 6% yield, investors flock to it.

I used to be the same. I thought that a higher yield always meant a better deal.

But after seeing hundreds of real-world investments, I’ve learned something important. A high yield on paper rarely tells you whether a property will actually make you money.

In this article, you’ll learn why gross yield so often misleads investors. And why a lower-yielding property can genuinely leave you better off financially.

A high gross yield can look attractive, but it doesn’t tell you how much money you’ll actually make.

When investors talk about yields, they’re often talking about the gross yield:

Gross yield = (weekly rent × 52) ÷ property value × 100

So, if a property rents for $570 a week and is worth $600,000, that’s a 4.9% gross yield:

($570 x 52) / $600,000 x 100 = 4.9%

Nice and simple. Tidy.

But here’s the problem: the gross yield ignores everything that costs you money.

It doesn’t include:

So, while gross yield is fine as a back-of-the-napkin check, it’s not serious financial analysis.

What you really care about is the net yield. That is what’s left after your operating expenses (but before the mortgage).

The reason net yield ignores your mortgage is that some property investors have bigger cash deposits than others. While the property will have the same operating expenses, no matter which investor owns it.

And the issue is that higher-yielding properties can come with higher costs.

Higher yield properties often come with higher costs, like:

Older properties are more run-down, and so often don’t get premium prices. That’s why they often have higher gross yields. But then they also cost more to maintain.

A brand-new property might only need $500 a year spent on maintenance. Why? Because well, everything is new (e.g. hot water cylinder, heat pump, etc.).

An older one? That can easily be $3,000 a year, driven by things like old plumbing, tired appliances, and more frequent callouts for repairs.

Properties need to be maintained over time. And older high-yield properties often need more maintenance. But often investors keep putting it off for as long as possible (deferred maintenance).

Let’s say you buy a property where the roof needs replacing in 10 years. That roof could cost $30,000. A financially responsible investor, in this situation, would set aside $3,000 a year for that future expense.

When you combine that with higher ongoing maintenance, you can quickly be looking at $5,000 a year (roughly $100 a week) just to be sensible and prepared.

Most investors don’t do this. And that’s why cashflow becomes lumpy.

I recently worked with a client in Auckland who tried to refinance an older property. The deferred maintenance was so severe that the bank wouldn’t lend against it.

That’s a consequence people don’t think about when they’re chasing yield.

Some high-yield properties look great until you realise that they come with higher costs.

Often, higher-yield properties are multi-income or dual-key. That means there are two units on the same property. These can come with:

Again, none of this shows up in the gross yield number. Which is why you need to look at the net yield.

Let’s compare two real properties at a similar price point.

Property #1: 12 & 13 Attlee Place, Gisborne.

Two one-bedroom homes on the same title, up for $560,000.

I found this property on Trade Me by searching for “high yield” investments.

This rents for $760 a week. So, the properties have a gross yield of 7.1%.

Property #2: 10 Hammond Place, Christchurch.

A New Build two-bedroom, two-bathroom townhouse priced at $549,000.

This is expected to rent for $515 a week. And so has a gross yield of 4.9%.

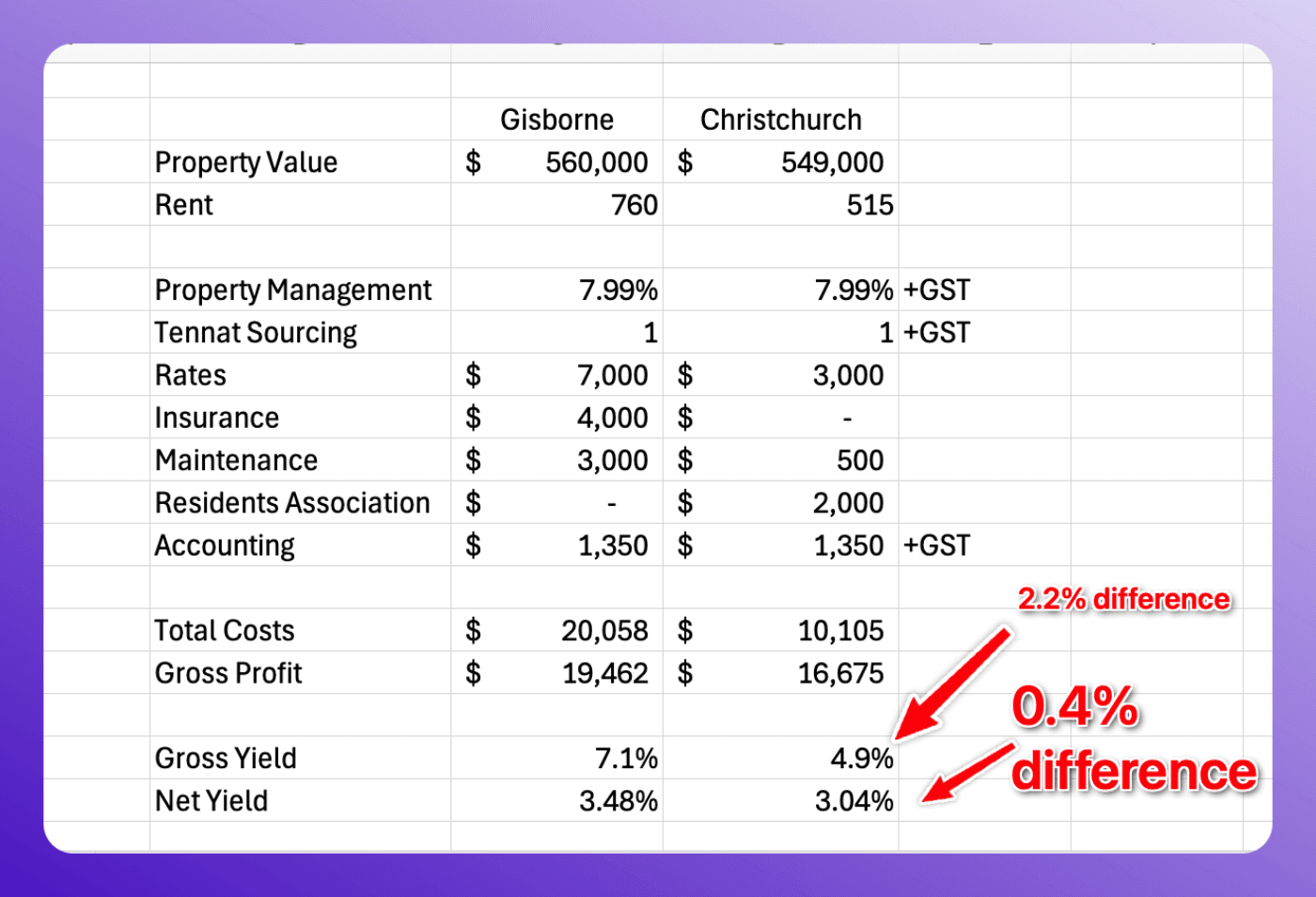

These properties cost a similar amount of money. But the Gisborne property has a 2.2% higher gross yield and earns an extra $245 a week. Sounds tempting.

But now we need to factor in the costs.

| High Yield (Gisborne) | Lower Yield (Christchurch) | |

|---|---|---|

| Rent (per week) | $760 | $515 |

| Property Value | $560,000 | $549,000 |

| Gross Yield | 7.1% | 4.9% |

Because this Gisborne property has 2 units, the rates are higher than if it were just one property. Call it $7,000, compared to the Christchurch property that would likely pay $3,000 in rates.

Then there is insurance. Two older units might pay $4,000 in insurance. Whereas townhouses usually get a bulk discount through the residents’ association, which might cost $2,000.

Then there is maintenance. Look at the Gisborne property. Both dwellings are old and tired, with ageing kitchens, roofing issues, and clear signs of ongoing maintenance.

This might need $3,000 a year of maintenance. Whereas a new property might only need $500 a year at the start.

When you add it all up, the gross yield on the Gisborne property might be 7.1%. But once you take out the operating costs, the net yield is only 3.5%.

Compare that to the newer property. The gross yield was 4.9%. But the net yield is 3.0%.

Now let’s be really honest. The newer property still has a lower net yield (in this example).

But if you’re looking at the gross yield, the difference between the two properties is 2.2%. A big difference.

Once you look at the net yield, the difference is just 0.4%. Still a difference, but a much smaller one.

Similarly, if you just look at the rent, you’d think that the higher-yield property will get an extra $245 in rent per week.

That’s true, but once you factor in the additional costs, the difference is only $54 a week. Still a difference. But not as tempting as it was at first.

Once you know the real numbers, you can consider other things like:

The older Gisborne property would require a $168,000 (30%) deposit. Whereas the new property only needs a $109,800 (20%) deposit.

The older property is more likely to have issues with roofs, hot water cylinders, and other larger capital projects. These could cost tens of thousands of dollars.

In my experience, yield properties (like the Gisborne property) tend to appeal to investors. Not so much to home buyers. So, they typically increase in value more slowly.

That doesn’t mean you should always buy a newer property. It’s just to say that once you look at the net yield (what I consider the real numbers), you can consider which property would suit your portfolio.

A 6% gross yield might genuinely be a great deal.

But before you let the number seduce you, you need to add up all the costs. That’s including the ones most investors don’t think about until it’s too late.

Gross yield isn’t useless; it’s just incomplete.

And investors get into trouble when they stop the analysis there.

A 0.4% net yield gap is a very different decision to a 2.2% gross yield gap. Make sure you're looking at the right number.

Free personalised wealth plan · $390 value

Get a personalised wealth plan from an Opes adviser - they'll look at the full picture for your situation, not just the gross yield.

Get your free wealth planFounder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser