Number Crunching

LVR calculator – How to calculate LVR

Quickly calculate your loan-to-value ratio and find out how much you can borrow

Mortgages

10 min read

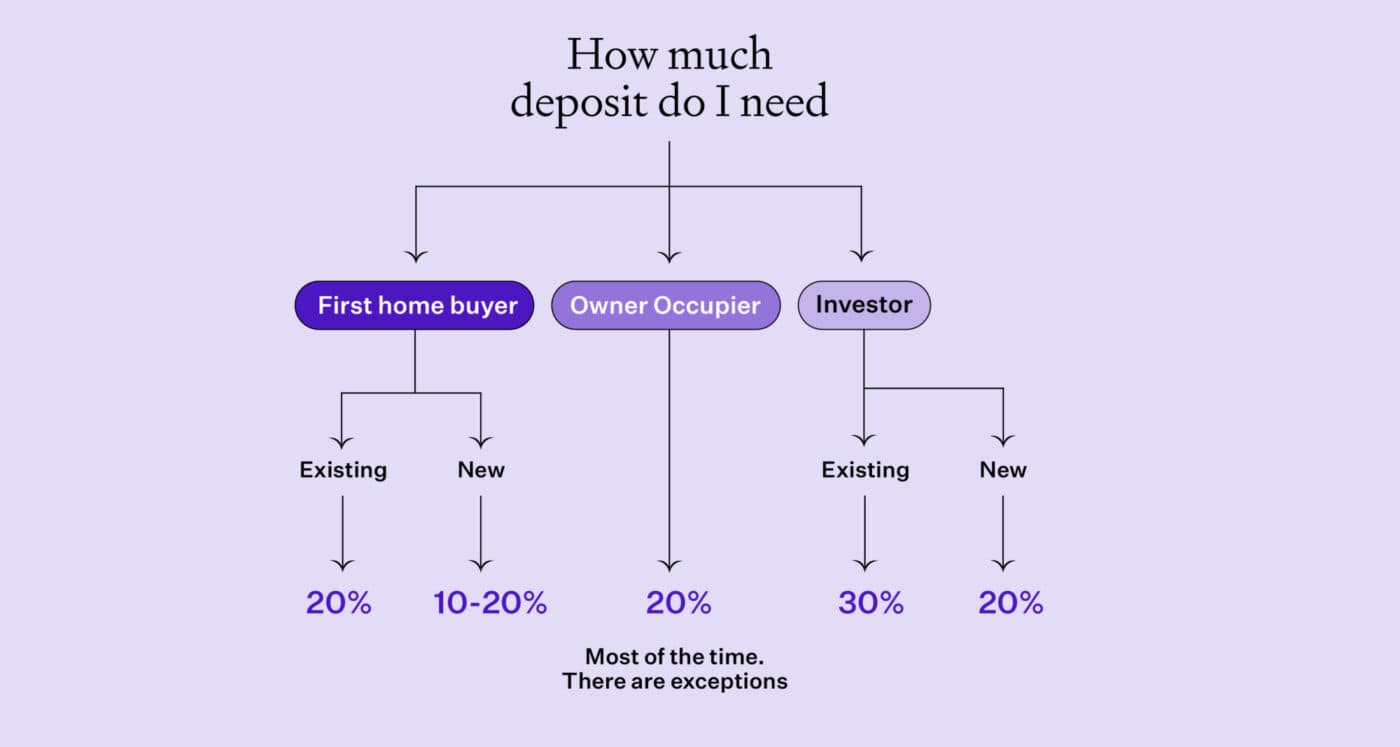

The Loan-to-Value Ratio restrictions (LVRs) dictate how big a deposit you need to buy a house. These are set by the Reserve Bank of New Zealand.

In 2026, Kiwi property investors need a 30% deposit to buy an existing property and a 20% deposit for a New Build, while owner-occupiers generally need a 20% deposit.

| Buyer type | Property type | Minimum deposit | Speed limits and exemptions |

| Owner-occupiers | Existing property | 20% | Up to 25% of each bank’s lending can be at a lower deposit. Kāinga Ora First Home Loans are exempt from LVR restrictions. |

| Property investor | Exisiting property | 30% | Up to 10% of each bank’s lending can be at a lower deposit. |

| Property investor | New Build | 20% | New Builds are exempt from the LVR restrictions. |

The Reserve Bank sets the LVR rules to limit low-deposit lending. This is to make the financial system safer.

In this article you’ll learn what LVRs are and how they impact how much deposit you need to buy a house.

The most recent LVR change was on 1 December 2025, when the Reserve Bank eased its “speed limits”.

This means banks can now lend to more borrowers with smaller deposits.

Up to 25% of each bank’s owner-occupier lending can be to people with less than a 20% deposit.

And up to 10% of each bank’s investor lending can be to people with less than a 30% deposit.

For New Build nothing has changed; investors still generally only need a 20% deposit.

LVRs aren’t the only borrowing restriction the Reserve Bank has set.

Since July 2024, the Reserve Bank’s Debt-to-Income (DTI) rules have also capped the amount you can borrow to:

In practice, borrowers need to satisfy LVR and DTI rules.

LVRs determine how much deposit you need, while DTIs determine how much you can borrow based on your income.

For buyers with smaller deposits, LVRs are often the main hurdle. For borrowers with plenty of equity, the DTI limit may become the bigger constraint.

Just keep in mind that in addition to meeting the Reserve Bank’s requirements, you also need to meet the individual bank’s lending criteria.

Read our full guide to Debt-to-Income Ratios.

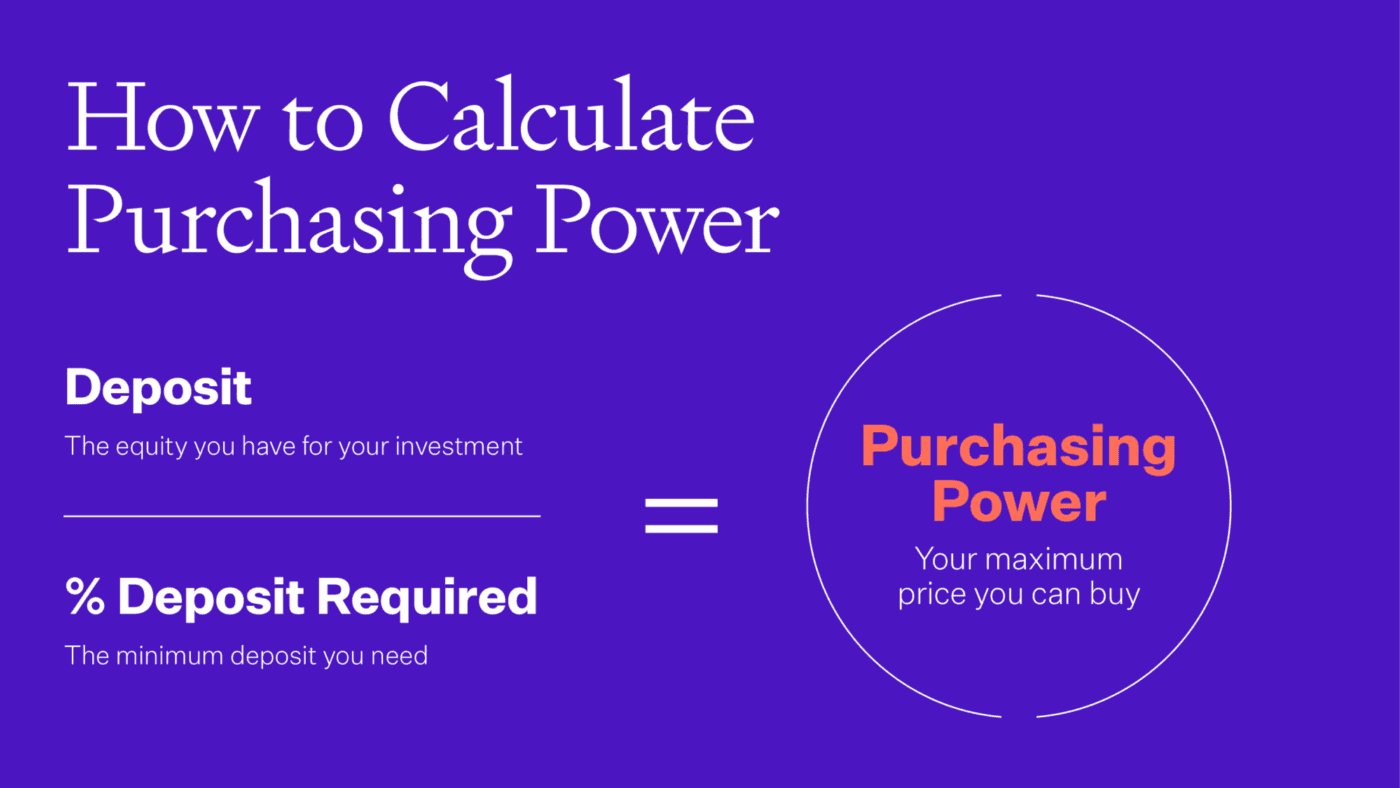

To work out how much you can potentially afford, divide your deposit by the minimum deposit the bank requires.

That gives you your maximum purchase price under the LVR rules.

The formula is: Your deposit ÷ deposit required = maximum purchase price

Let’s say an owner-occupier and an investor have the same deposit – $200,000.

The owner-occupier could usually buy a property worth up to $1 million, while the investor buying an existing property could usually buy up to $667,000.

| Buyer type | Deposit required | Calculation | Maximum purchase price |

| Owner-occupier | 20% | $200,000 ÷ 0.20 | $1,000,000 |

| Investor buying an existing property | 30% | $200,000 ÷ 0.30 | $666,667 |

That is one of the main ways LVR rules affect buyers. Even with the same deposit, investors are often limited to a lower purchase price than owner-occupiers.

Use our LVR calculator to work out your deposit requirement and potential maximum purchase price.

LVR restrictions do affect the market, but usually less than people think.

As property prices rise borrowers’ loans make up a smaller percentage of the property’s new (higher) value, so your LVR goes down.

So, as house prices rise, property owners can typically borrow more anyway.

That’s partly why when LVRs came back in (2021) they had little impact on house price inflation.

If we think back to when the Reserve Bank increased the deposit investors needed from 20% to 40%, the bank only expected LVRs to lower house price inflation 1-2%.

That doesn’t mean house prices alter by only 1-2%.

It means that if house prices were going to go up 10% anyway, they now rise 8-9% instead.

Peter Norris, Managing Director at Opes Mortgages (BNZ Mortgage Adviser of the Year 2018, $1.2 billion-plus in lending facilitated), says:

“I think LVR restrictions are likely to ease at some point. If they do I expect the investor deposit requirement to move from 30% down to 25% before it ever goes back to 20%.

“That’s because LVRs are one of the Reserve Bank’s main tools for controlling risk in the housing market.

“They can tighten them when the market is running hot, or loosen them when they want to stimulate lending again.”

There are a few situations where low-deposit lending is still possible under the LVR rules.

New Builds are the biggest exemption. The Reserve Bank’s LVR restrictions do not apply. So it’s up to the bank how much they are willing to lend.

This matters most for investors. In practice, an investor may only need a 20% deposit for a New Build instead of 30% for an existing property.

On a $700,000 property that’s the difference between needing $140,000 and $210,000.

In some cases investors can purchase a New Build with as little as a 10% deposit through the major banks, although that often comes with paying a higher interest rate.

The Reserve Bank allows banks to do a limited amount of low-deposit lending outside the usual LVR rules.

From 1 December 2025:

In practice, most of this low-deposit lending goes to first-home buyers.

Banks can sometimes lend above the usual LVR limits if the extra borrowing is used to bring a property up to code.

That could be if a property needs a bigger mortgage to be repaired after it has been damaged (when a bank allows you to borrow more than the normal limit, so the property can be improved).

Short-term bridging loans are also exempt. This is when a homeowner buys their next property before selling their current one.

Because bridging finance is temporary, the Reserve Bank does not treat it the same way as long-term lending.

If you refinance your mortgage to a new bank you are also exempt from the LVR restrictions. That’s as long as you are not increasing the size of the loan.

This means borrowers can still switch banks and shop around rather than being stuck with the same lender because of the LVR rules.

Kāinga Ora First Home Loans allow eligible buyers to purchase with a 5% deposit (there are some income caps). You can only get the loan if you earn less than $95,000 a year as a single buyer, and $150,000 (combined) for a couple.

To be eligible you generally need at least a 5% deposit, be buying your first home, and meet those income caps set by Kāinga Ora.

This means eligible first-home buyers can still borrow at lower deposit amounts.

Peter Norris, Managing Director at Opes Mortgages (BNZ Mortgage Adviser of the Year 2018, $1.2 billion-plus in lending facilitated), says:

“If an investor does not have a 30% deposit that does not always mean they can’t invest.

It might mean:

“If none of those options suit, another route is to refinance (i.e. switch banks).

“In some cases switching banks can help an investor release more equity or access a lender with a more flexible policy, which can make it easier to move forward with a purchase sooner.

“So, if you don’t have a 30% deposit, the answer is not always to ‘wait longer’. It may be the right property type, lender, or loan structure gives you another path into the market".

LVR restrictions have been around since 2013.

But the important thing to know is that they don’t stay the same for long.

Since they were first introduced the Reserve Bank has loosened them, tightened them, and removed them altogether. Then they brought them back again.

For example, investor deposit requirements have been as high as 40% at some points, then reduced to 35%, and now sit at 30%.

During Covid-19 LVR restrictions were removed altogether, although that didn’t last long. They were reintroduced less than a year later.

| Year | What changed |

| 2013 | LVR restrictions introduced |

| 2015 | Auckland investor deposit set at 30% |

| 2016 | Investor deposit increased to 40% nationwide |

| 2018 | Investor deposit reduced to 35% |

| 2019 | Investor deposit reduced to 30% |

| 2020 | LVR restrictions removed during Covid |

| 2021 | LVRs reintroduced. Initially the investor deposit was 30%, then lifted to 40% |

| 2023 | Investor deposit reduced to 35% |

| 2024 | Investor deposit reduced to 30% |

So while today’s rules matter, they are not permanent.

The Reserve Bank changes LVR restrictions depending on what is happening in the housing market and the wider economy.

That means the deposit rules investors face today could look different again in the next 1–2 years.

Mortgage broker for over 10 years, property investor and Managing Director at Opes Mortgages

Peter Norris, a certified mortgage adviser with 10+ years of experience, serves as the Managing Director at Opes Mortgages. Having facilitated over $1.2 billion in lending for 2000+ clients, Peter is a respected authority in property financing. He's a frequent writer for Informed Investor Magazine and Property Investor Magazine, while also being recognized as BNZ Mortgage Adviser of the Year in 2018 and listed among NZ Adviser's top advisers in 2022, showcasing his expertise.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser