Reviews

Top 5 property management companies in Christchurch (2026)

In this article, you’ll learn our top picks for property managers in Christchurch, along with some unique points about them.

Property Management

6 min read

Author: Tiffany Bracey

Property Manager Team Leader at Opes Property Management Auckland.

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Many property investors get rental appraisals, then ask “Can I trust this appraisal?”

After all, just because a property manager says a property will rent for $750 … doesn’t mean it actually will.

In this article, you’ll learn:

A rental assessment is an estimate of what your investment property will rent for. Property managers create these, often as a way to drum up business.

You ask them what they think your property will rent for. They give you their opinion for free, and then you might decide to use them.

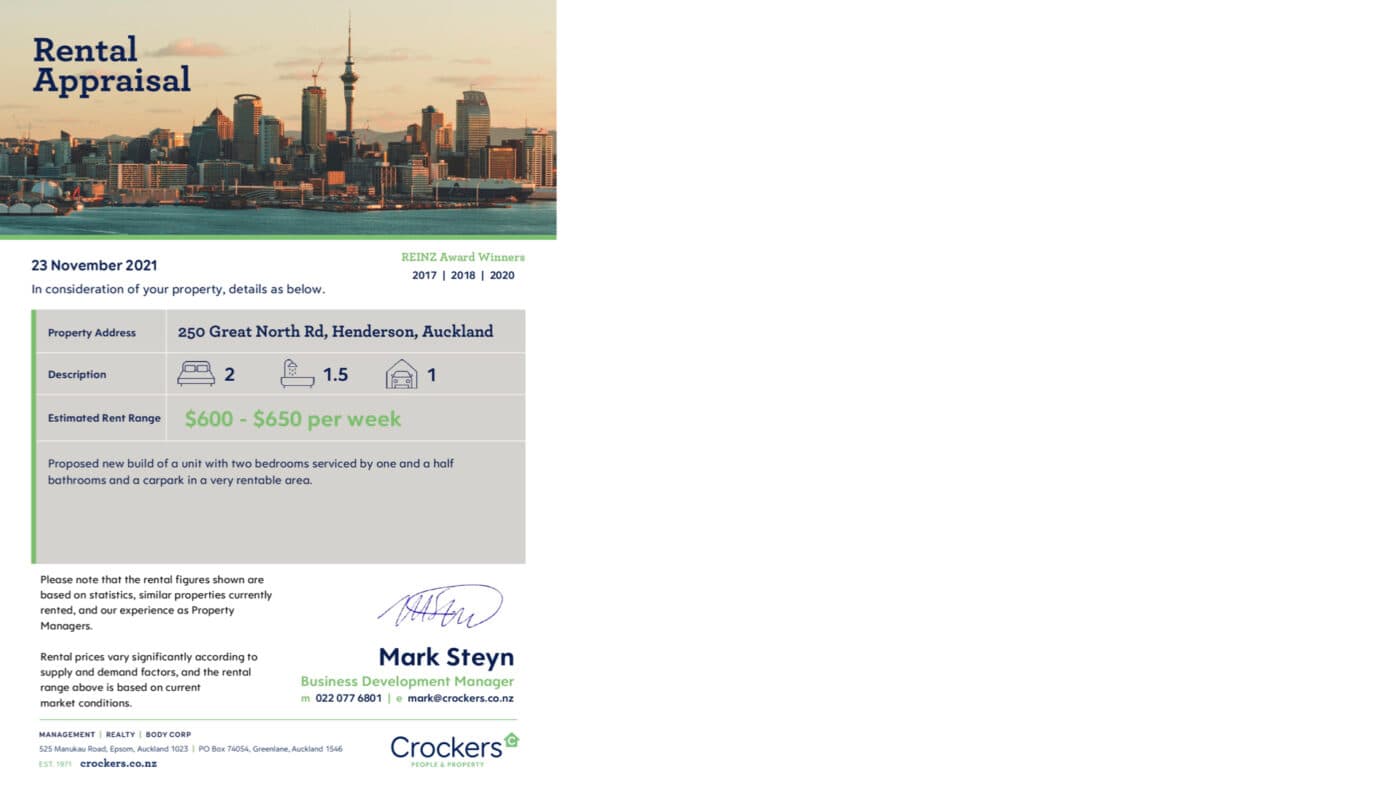

This is usually delivered in a formal letter to you from the property manager.

Here’s an example –

Property investors use them to:

In any case, the goal is to give you the information so you can make an informed decision.

But you need to know that rental assessments are based on what’s going on right now.

They can’t predict that the market might change next week. After all, the rental market can change week to week.

A rental appraisal may not take into account the market unexpectedly cooling down.

When a property manager creates an appraisal they look at:

Most property managers will create your rental assessment based on several steps. Here’s what usually happens –

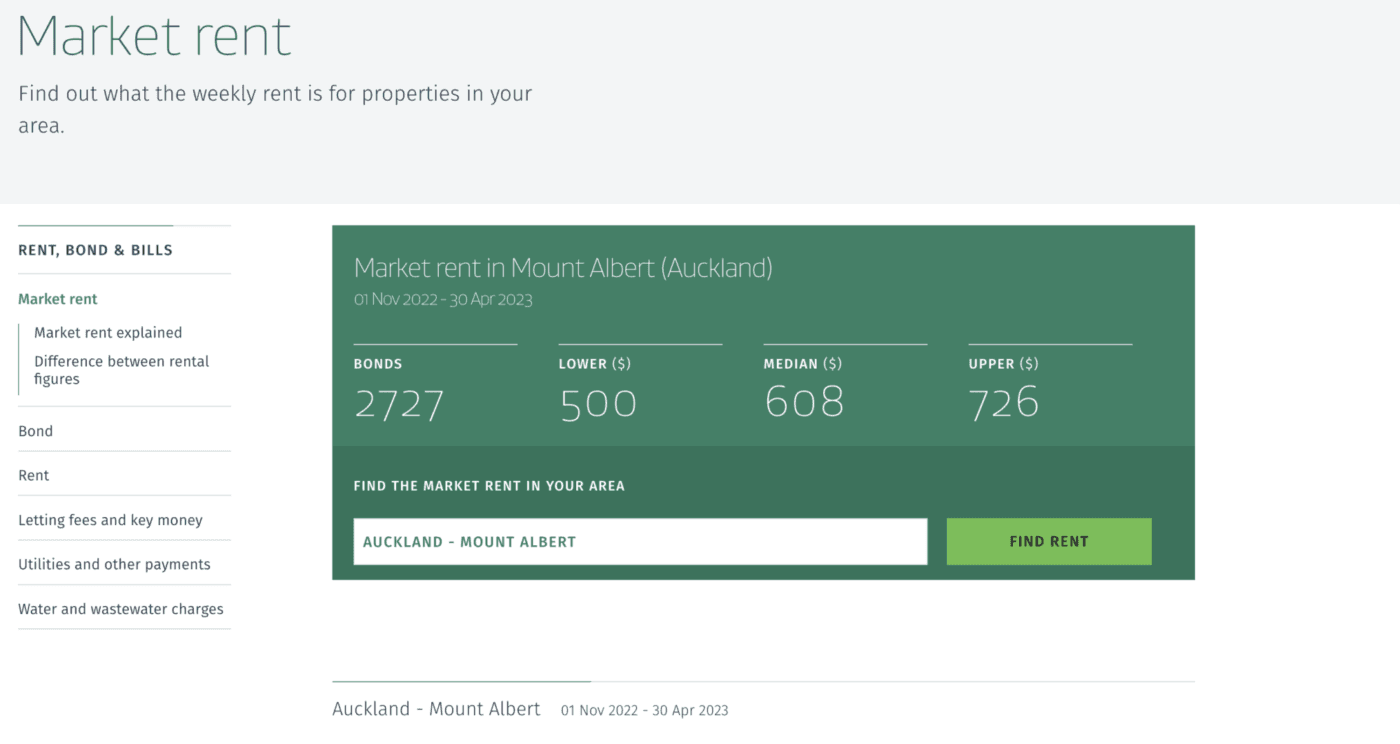

First up, they’ll look at the data on the Tenancy Services website.

Here they can access the information from actual bonds lodged in the last 6 months. So, what people are actually paying for rentals in the real world.

You can type in the suburb you want to look at, and find out the market rent for that area.

For instance, here’s a look at Mount Albert in Auckland. As you can see, it’s broken down into lower and upper quartiles, as well as the median.

But it is often broken down further into property type. For instance, whether the property is a townhouse or an apartment, and how many bedrooms there are.

But, this is only provided for areas where there is enough data. So it’s more likely you’ll find granular data in larger cities than tiny towns.

Here’s something else to look out for. The data from Tenancy Services can be old.

It includes data from bonds lodged over the last 6 months, but there can sometimes be a 1-month delay between when a landlord receives the bond and when they lodge it.

So, sometimes Tenancy Services data can look low.

A good property manager will also check out Trade Me. It’s a good way to suss out the competition.

By looking at other listings, property managers can see what’s on offer. What other properties are being advertised for, and how many properties are available.

Let’s say a similar property is being advertised for $500 a week. There is a good chance your property will rent for $500 a week too.

But this is only useful when comparing similar properties.

This process wouldn’t be useful if comparing a 1960’s weatherboard house with a New Build townhouse.

Which is why Step 3 is so crucial.

The trouble with Trade Me is that properties come on and are taken off all the time.

And once a property is off the site, the link expires. You can’t see the details again.

That’s why property managers think about similar properties they’ve rented in the area or what they’ve seen online in the past.

They deal with properties and tenants, day-in and day-out. So, they know things that a one-off Trade Me search doesn’t.

For instance, they’ll know:

They also have a good idea of what properties will be in more demand in a particular area.

The older the rental appraisal, the less accurate it is.

If you get a rental appraisal and plan to find a tenant 4 weeks later, it’ll be pretty accurate.

It wouldn’t be 100% accurate. After all, you won’t know the actual rent until a tenant signs a contract. But it should be pretty good.

But, if you buy a New Build it could take 12 to 24 months before the property is built.

That’s a pretty big window in a market that moves week to week.

So, by the time you get to settlement the market will have changed. That original rental appraisal probably won’t be accurate anymore.

Rents might have gone up, but they could have stayed the same or gone down.

Some property managers will factor in the expected annual rent increases. But again, there is no guarantee the market will increase at the same percentage every year.

Sometimes property investors make mistakes when relying on rental appraisals. Here are the common mistakes we see here at Opes Partners.

Some property managers suggest a higher rental amount to get your business.

After all, managers give these to try and get you to use their service. That’s fine. It makes sense.

But sometimes they pump this up so you think, “They think they’ll get me a higher rent … so I’ll use them.”

And then when the property goes on the market, nobody wants to rent it.

In this case, the rent will be reduced. You might have to wait weeks before you get the rent hitting your bank account.

For example, a 1-bedroom property in central Auckland was given a rental assessment of $600-$630. The tenant who eventually signed, rented it for $495.

In this case, the original appraisal was completely over the top.

It can depend on what company you use.

More well-known property management companies know their reputation is on the line. This means they are less likely to quote an unrealistic rent just to get your business.

Be cautious when you get a rental appraisal from a developer’s property managers.

There is a higher chance they will give you an unrealistic rental projection. This is to make the property seem more attractive as an investment, in the hope you buy it.

This doesn’t mean the rental assessment will always be skewed. Not all developers are out to get you.

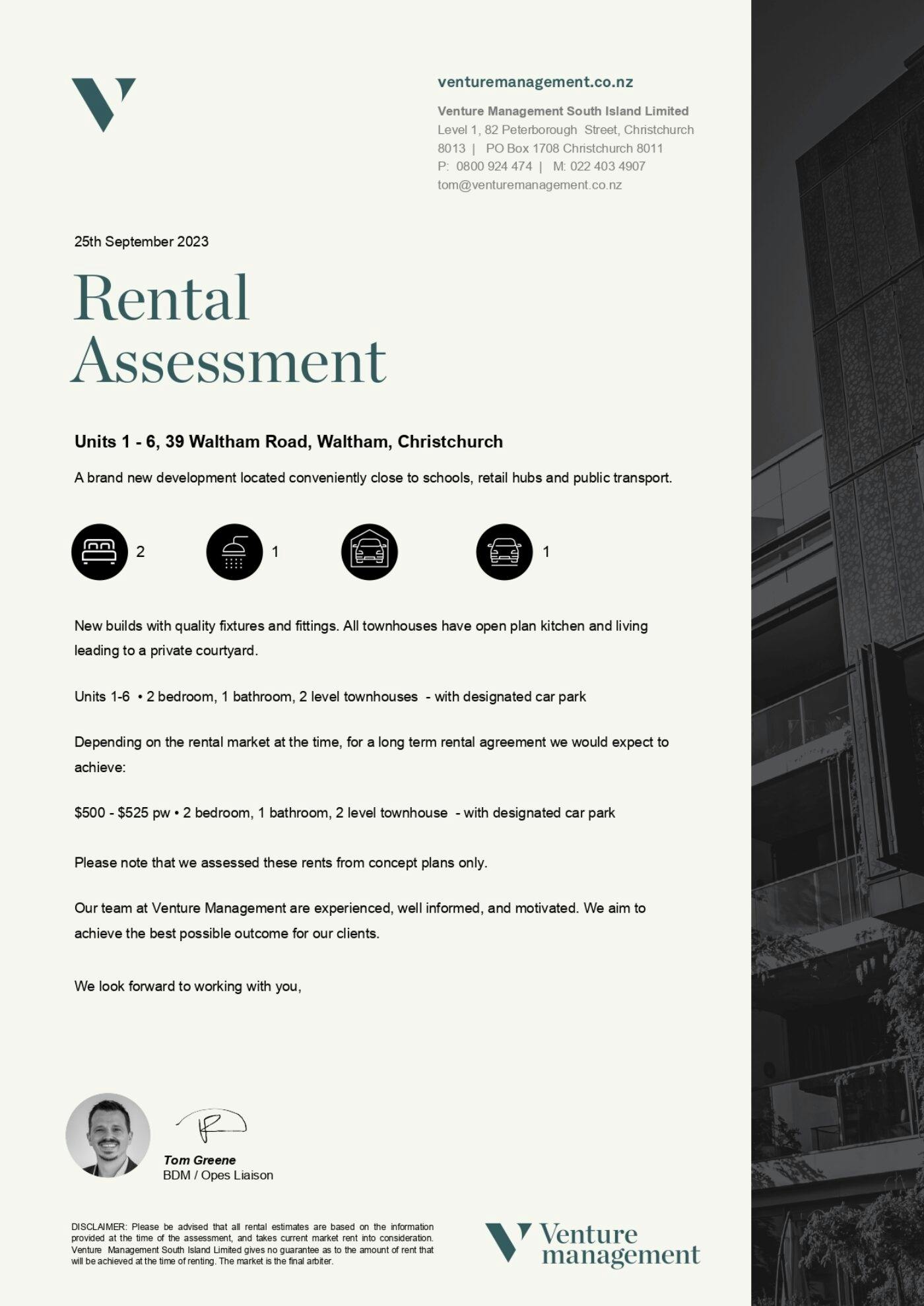

For instance, Opes Property Management does all the rental assessments for us here at Opes.

In our case our property managers lean on the more conservative side. This is to protect their reputation, and ours.

And they also provide more context in their appraisals so you can check their work –

Rental assessments aren’t gospel, but they can give you an idea about what your property will rent for.

Just don’t treat them as a guarantee. Just because a property manager says you’ll get $480 - $500 for a property, it doesn’t mean you 100% will get that amount.

Property Manager Team Leader at Opes Property Management Auckland.

Tiffany is an experienced property manager who understands the importance of strong systems to deliver top-tier service. She is committed to staying ahead of the ever-changing compliance requirements under the Residential Tenancies Act 1986.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser