Number Crunching

How much is my home worth?

A step-by-step guide on resources to help evaluate your home's market value in 2026.

Property Investment

6 min read

Author: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Reviewed by: Louis Fraysse

Louis is a registered financial adviser with an MBA from Massey University.

In New Zealand, CVs (Capital Values) are set by councils roughly every 3 years and can quickly become outdated.

As of June 2026 properties are selling anywhere from 19% below to 35% above their CV, depending on the region. The gap reflects when valuations were last updated, not whether a property is cheap or expensive.

That’s a bit annoying if you’re trying to figure out how much to offer on a house.

Opes Partners tracks whether properties are generally selling above or below CV. And the data on this page is updated every month.

In this article, you’ll learn where houses are selling above and below CV, why CVs can be so far off, and how to actually to use them when you’re buying a house.

CVs can be useful as a rough guide, but they’re not the same as market value.

CVs feel official because they come from the council. But really, they’re just council estimates used to work out how much you pay for your rates.

Sure, they can be useful as a rough guide for what a house is worth. But they don’t always reflect what a property would sell for today.

But they’re not the same thing as market value.

CVs are mainly used to help councils calculate rates. They are updated en masse, at a specific point in time.

That means they may already be months or years out of date by the time you’re looking at a property.

That’s why two things can be true at once: CVs can be useful as a rough guide, but they can also be wildly different from what buyers are actually paying.

But there are massive extremes. Properties in some parts of the country are selling well above CV; properties in other parts are selling well below CV.

For instance, in June 2026 the average property in Otorohanga District sold for 19% below CV.

So, if a property in Otorohanga District has a rateable value of $1 million, there is a decent chance it will sell for around $810,000 ($190,000 less than the CV).

Other councils where properties are selling close to or below CV are Wellington City, where they are selling 10% below, and Ruapehu District, where properties are selling 7% below CV.

However, in Mackenzie District, the average property sold for 35% above CV.

Properties in Westland District and Gore District are also selling 25% above and 17% above CV, respectively.

That doesn’t mean properties are undervalued in Otorohanga District or overvalued in Mackenzie District. It has more to do with how and when the CVs were set.

This map shows where houses are selling above and below their CV. Hover over the map to explore your area. Or, use the table at the end of this article to search for the data in your area.

CVs are often out of date, sometimes even on the day they are launched.

But that doesn’t mean they are useless.

As a buyer, the CV can still give you a rough starting point, especially when the listing doesn’t include an asking price.

| Pros | Cons |

| Gives you a rough price guide | Often out of date |

| Helpful when there's no asking price | Can mislead buyers and sellers |

| Easy to find on listings | Not the same as market value |

| Can help with negotiation | Buying a property "below CV" doesn't always mean "good deal". |

The reason CVs are so tempting is that buyers often don’t get much else to work with.

A property might be listed as “auction”, “price by negotiation”, “deadline sale” or “tender”. That means the agent isn’t putting the seller’s expected price on the listing.

And even if you call the agent, they might still be cagey. They may not give you a clear idea of what the property will sell for, even though you know they’ve probably had that conversation with the seller.

So buyers look for clues.

They check the CV. They look at Homes.co.nz. They compare whatever numbers they can find online.

That’s understandable. Buyers just want to know how much a property might cost. They want to avoid the disappointment of thinking they can afford a house when actually, it’s going to sell for much, much more.

The CV gives you something to anchor to. It can also be useful in a negotiation. A buyer might say: “I don’t want to pay more than the CV.”

Even if everyone knows the CV is out of date, it still gives you a reason to push back.

But this is where buyers need to be careful.

A property selling below CV can feel like a bargain. But that doesn’t automatically mean it is. You might still be paying more than the property is really worth in the current market.

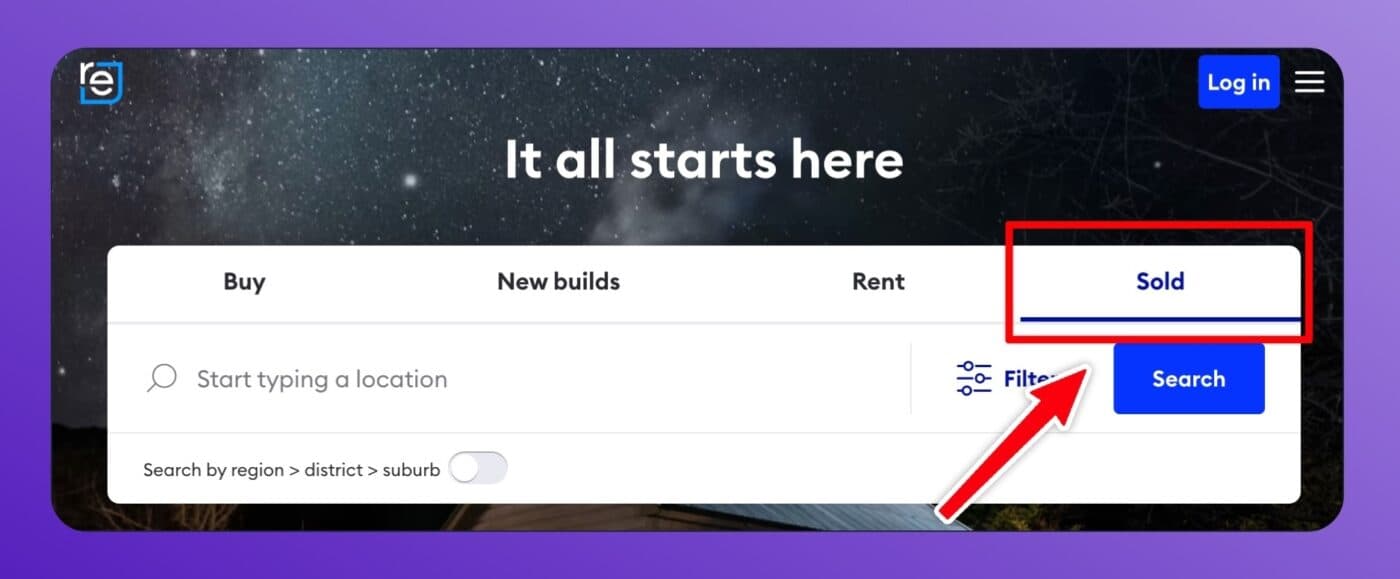

A better place to start is by looking at what similar properties have recently sold for, because that shows what buyers are actually paying.

You can find these sales on websites realestate.co.nz.

Use the tool to look at properties that have sold recently in the same area, then compare them with the property you want to buy.

For example, say the property you want to buy has a CV of $1 million.

But when you look online, you find three similar properties nearby have recently sold for $890,000, $910,000 and $920,000.

That tells you the CV might be too high.

But then you need to go one step further.

Compare those homes to the one you want to buy. If the property you want to buy isn’t as nice, maybe it should sell for less. If it’s been renovated or has better views, maybe it should sell for more.

It takes more time. But that’s how you become an educated buyer.

Most councils update their property valuations around every 3 years.

If a council only recently updated its valuations, there’s a better chance those estimates are more accurate.

The property market may not have moved much since the valuations were set.

But if the valuations are old, the market could have moved considerably.

That’s when CVs become less useful.

Councils don’t physically value every property. There’s no council worker with a clipboard walking past everyone’s house.

They generally use data companies to estimate values at scale. Think of it a bit like Homes.co.nz, OneRoof or Valocity, where you type in an address and the website gives you an estimated value.

Some councils use companies like Quotable Value or Opteon to provide these estimates.

That means CVs are usually computer-generated estimates. They’re not a valuer walking through the front door, checking the kitchen, looking at the view, and deciding what the property is worth.

Buyers should generally ignore CVs, or at least take them with a very small grain of salt.

People pay attention to them because they assume that, since the council came up with the number, it’s the official value of the property.

But that’s not really the case.

A CV might arrive in November, but the actual calculation could have been done six months earlier. So it’s really telling you what the property may have been worth back then, not what it’s worth today.

And because CVs are usually updated years apart, they can jump around quite a bit. That can be a shock if you’re not closely following the property market.

So I think of a CV as a Homes.co.nz estimate of your property, except it’s already out of date.

You wouldn’t look at a value on Homes.co.nz and think that’s exactly what the property will sell for. And you wouldn’t look at what the estimate was 18 months ago and think that was accurate either.

But that’s what buyers are doing when it comes to CVs.

That doesn’t mean CVs are completely useless.

They can still be a bargaining tool. Some sellers will even challenge their CV to get it higher before they list their property because they know buyers use it as a shortcut.

But ultimately, buyers are better off looking at recent comparable sales and making their own judgment.

Most people probably won’t do that because it takes more work.

They’ll keep looking at CVs, even though they’re not the best guide.

But if people want the data, here it is.

Free monthly report

Ed McKnight tracks house prices across every region and tells you what's actually happening - so you always know where the market stands.

Sign up for the reportResident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Ed, our Resident Economist, is equipped with a GradDipEcon, a GradCertStratMgmt, BMus, and over five years of experience as Opes Partners' economist. His expertise in economics has led him to contribute articles to reputable publications like NZ Property Investor, Informed Investor, OneRoof, Stuff, and Business Desk. You might have also seen him share his insights on television programs such as The Project and Breakfast.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser