Property Market

What's happening with NZ house prices right now?

Get the latest insights on New Zealand’s property markets, including trends, growth areas, and investment opportunities across regions.

Property Investment

2 min read

Author: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Reviewed by: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

As of May 2026, the major New Zealand banks predict house prices will change by -2.20% to +1.07% in the year to March 2027.

The median prediction from ANZ, ASB, BNZ, Westpac, and the Reserve Bank is that house prices will increase by -0.50% over that period.

No one knows with certainty where house prices will go. But getting a range of opinions can give us a sense of what might happen.

That’s why we look at all the big banks' forecasts here at Opes Partners and pull them together in one place. That way, you can get a sense of what may happen to house prices.

After all, property investors and homeowners always want to know: “Where are house prices going? What are the banks’ house price predictions?”

This table shows each bank’s prediction between March 2026 and March 2027.

Let’s dig into the details of each bank’s prediction.

The Reserve Bank puts out its house price forecasts every 3 months. This happens when they release their Monetary Policy Statement.

Here is the latest forecast they released in February 2026.

The Reserve Bank predicts that house prices will go up 1.07% in the year to March 2027.

ANZ frequently puts out new house price predictions. They update these often and summarise them in their monthly report – Property Focus.

ANZ predicts that house prices will go down -2.20% in the year to March 2027.

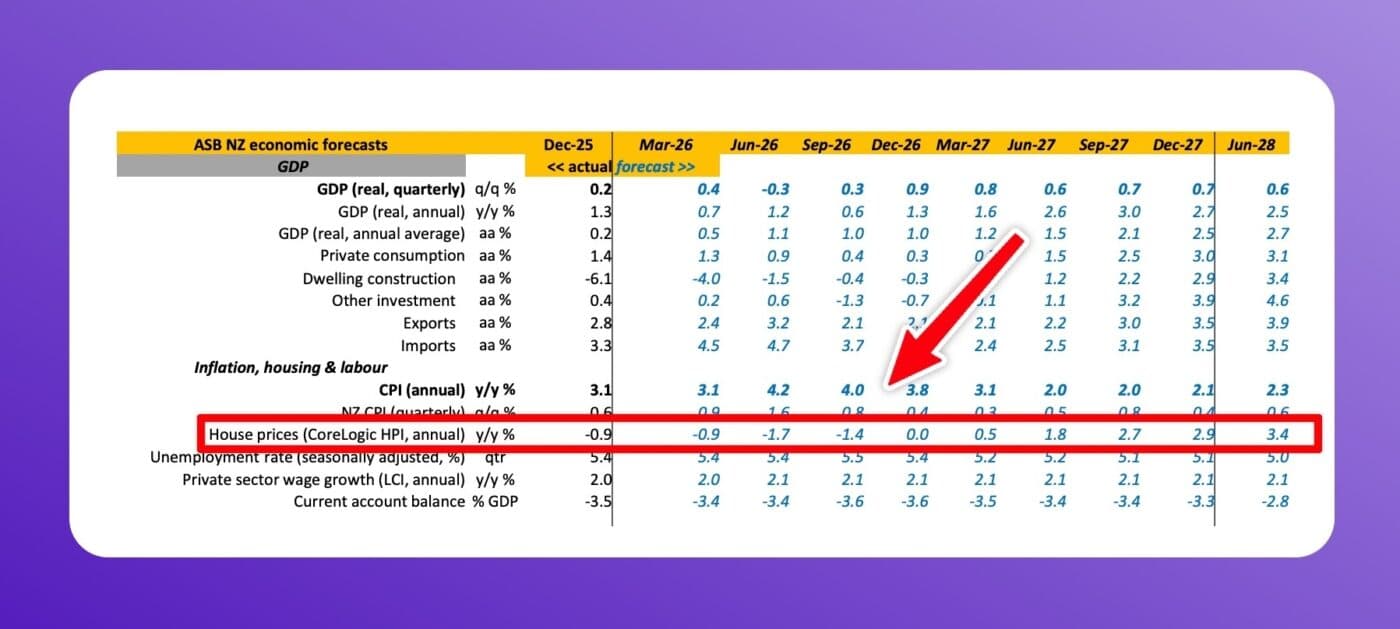

ASB releases new house price predictions every quarter. These are part of their Quarterly Economic Forecasts. Though in truth, sometimes they come out once every 4 months.

They published their latest forecast in March 2026. This showed that they think house prices will increase by 0.50% in the year to March 2027.

They don’t release their spreadsheets like the Reserve Bank, ANZ and Westpac do. But they do release a range of predictions, like this:

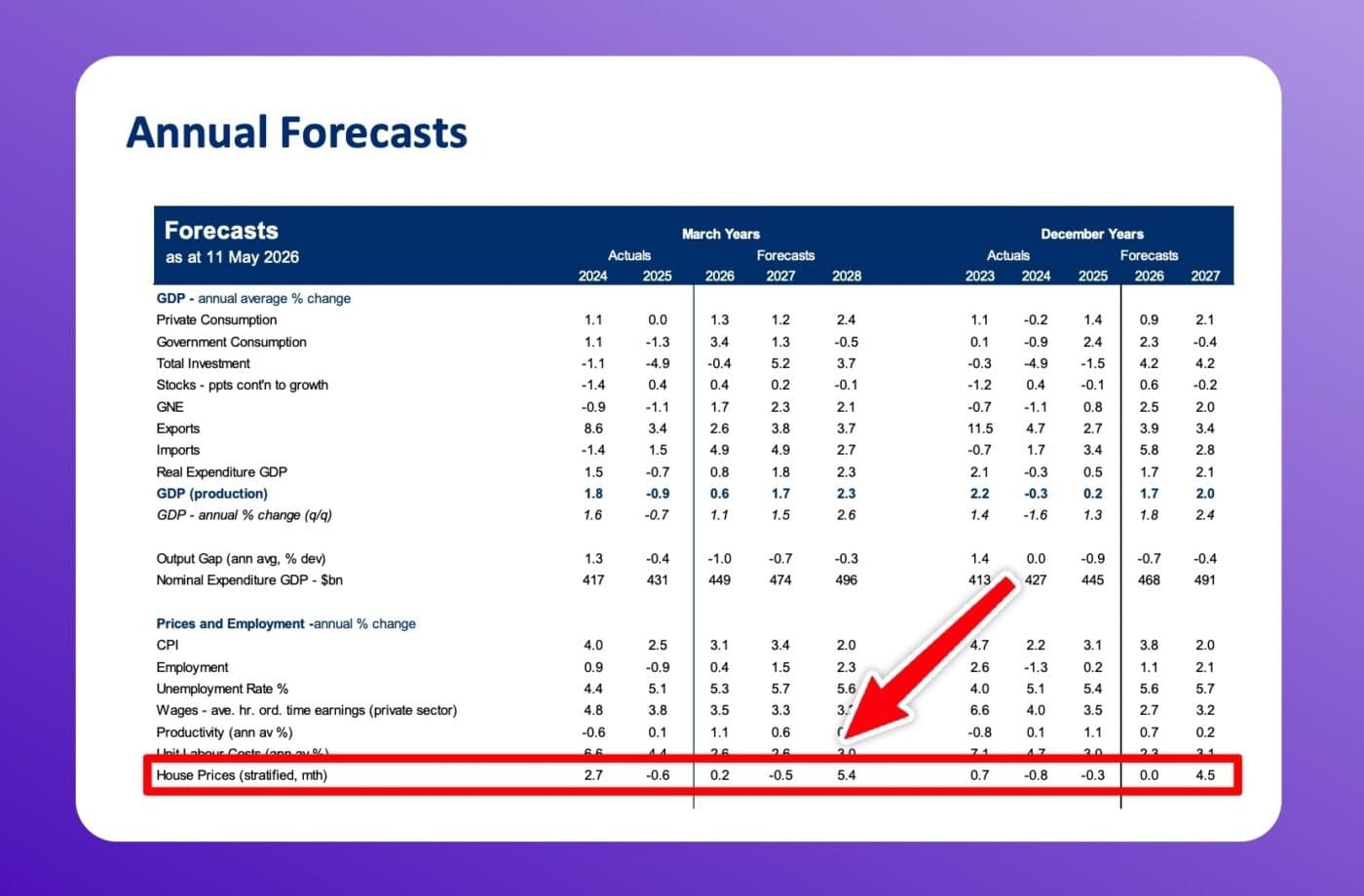

Like ASB, BNZ doesn’t release a spreadsheet with their forecasts. But they do regularly update their predictions in their weekly Markets Outlook report.

The latest forecast I’ve seen came out in May 2026. At that point, they thought house prices would go down by -0.50% in the year to March 2027.

Here’s an example of one of their Markets Outlook reports.

Westpac is one of the only banks that releases all their forecasts in a spreadsheet. This means we can see more closely where they think house prices will go.

Westpac released its most recent forecast in May 2026. At that point, Westpac thought that house prices would go down by -0.80% in the 12 months to March 2027.

A while back, I spoke with an investor named Mark. He was in his early 50s, based in Wellington, and had been sitting on the fence about buying another property.

At one of my property seminars, Mark asked, “With prices the way they are, do you think now’s the right time to buy – or should I wait?”

We had a good chat about house price predictions at the time. I showed him how the data suggested prices were stabilising and were forecast to grow steadily over the next few years.

But what really struck him was when I explained that prices had already hit their low point in his area.

Mark told me, “I’ve been waiting for the bottom, but I didn’t realise we’d already passed it.”

Three months later, I got an email from him. He’d bought a new-build townhouse in Lower Hutt. He told me he felt confident because he wasn’t guessing anymore - he had the data to back him up.

For Mark, understanding house price predictions wasn’t about timing the market perfectly. It was about having the confidence to make a decision based on facts, not fear.

And maybe it’s the same for you.

Either way, understanding where the market’s heading can help you make smarter decisions.

To be honest, I don’t really look at one bank and think: “Yup, that’s the one I trust”.

I don’t see one bank as more credible than another.

A few years ago, I made a video showing that a random number generator was more accurate at predicting house prices than some bank economists. So, you can't look at any of these forecasts and think that this is the amount of money you will definitely make.

Instead, I look across all the forecasts and ask: What’s the general mood here? What’s the overall direction they’re pointing in?

Because the truth is, these forecasts will not be accurate. World events will happen, interest rates will move, and that will throw these forecasts off.

The other thing to note is that, in the short term, each bank will have its own view of house prices, whether they are up or down.

But when you look at most bank forecasts over the long term, they nearly always point in the same direction. Up.

They might disagree on when that growth starts. They might disagree on how strong it’ll be. But over time, most of them still expect house prices to rise.

That doesn’t mean they know exactly when it’ll happen. They’ll all have a crack at calling it. But usually the bigger pattern is the same: short-term noise, long-term growth.

The median forecaster says house prices will decrease by -0.50% in the year to March 2027.

So what would happen if you bought an $800k property in Auckland and it went down in value by -0.50% next year?

By the end of the year, it might be worth $796,000. You lost $4,000.

Based on the bank's forecasts, here’s what the returns would look like.

Free monthly report

Ed McKnight tracks every bank's house price predictions and tells you what's actually changed - sent to your inbox every month.

Sign me up for the reportResident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Ed, our Resident Economist, is equipped with a GradDipEcon, a GradCertStratMgmt, BMus, and over five years of experience as Opes Partners' economist. His expertise in economics has led him to contribute articles to reputable publications like NZ Property Investor, Informed Investor, OneRoof, Stuff, and Business Desk. You might have also seen him share his insights on television programs such as The Project and Breakfast.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser