Property Investment

How to build passive income through property investment

This is the step-by-step guide that will teach you what it takes to build a significant passive income through property investment using real examples.

Property Investment

5 min read

Author: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Most of us don’t have piles and piles of money that we can do whatever we want with (wouldn’t that be nice).

So we need to make choices about what we spend on.

As a homeowner, you may want to renovate or upgrade your house.

At the same time you might also want to buy investment properties so you can sort your retirement.

Some investors can only get the money from the bank to do one or the other. They face a choice, either:

a) invest for your future

b) spend money to improve your lifestyle today.

But the problem is, it can be hard to prioritise your 65 year old self, when it's 20+ years in the future and you really want a new bathroom for your home now.

In this article, you’ll learn who needs to prioritise investment spending, and the psychological money lies you need to conquer to successfully invest.

For the purposes of this article, “personal spending” doesn’t mean that daily cup of coffee from the cafe, or going out for dinner on the weekend.

It’s the pricey, higher-end spending like:

If you’re borrowing money against your own home, or using cash, to do these things, you may struggle to also buy an investment property.

Video published 2nd August 2022

If you don’t have the money to both invest for your financial future and spend on yourself – then you have to make a choice.

And whatever you choose, you will make a sacrifice.

You either sacrifice now by not having the new boat, the home renovations, or the upgraded property.

Or you sacrifice later – by being poorer in retirement than you otherwise would be.

That’s not to say you should never renovate your home, or spend to improve your lifestyle. You should. Life’s too short to live like a trappiest monk.

But, you need to have a balance between living a decent lifestyle now, while also investing for your future.

Often this means investing in property first to maximise the amount of time you have in the market.

Often Kiwis will prioritise their short term goals, such as renovating the house to have a nicer property now, rather than their long term goals (retirement) simply because the long term goal is too far away.

According to researcher, Carl Davidson, this is because it’s hard to prioritise your 65-year-old self, because they are a stranger to you right now.

He also says that Kiwis (and all humans) have a certain amount of optimism bias, or an “everything will be ok attitude” that is hard wired into our genes. This is one of the top money lies he’s people that people tell themselves.

Why do people have an optimism bias? Because you’re living in your house thinking about ways to improve it. You’re not actively seeing the impact of your retirement – a retirement where you might not have all the choices you want.

According to Opes Partners Managing Director, Andrew Nicol, people tend to focus on the “what might” happen in the future, rather than what will happen.

For instance, you might hold off purchasing an investment property because you “might” want to renovate your house in future. However, what is certain is that if you don’t invest for your retirement, you’ll be poorer in retirement.

You might already think you have a plan for your retirement – a mix of superannuation and KiwiSaver.

While these are both a great start, they aren’t likely enough to fund the sort of retirement most Kiwis want.

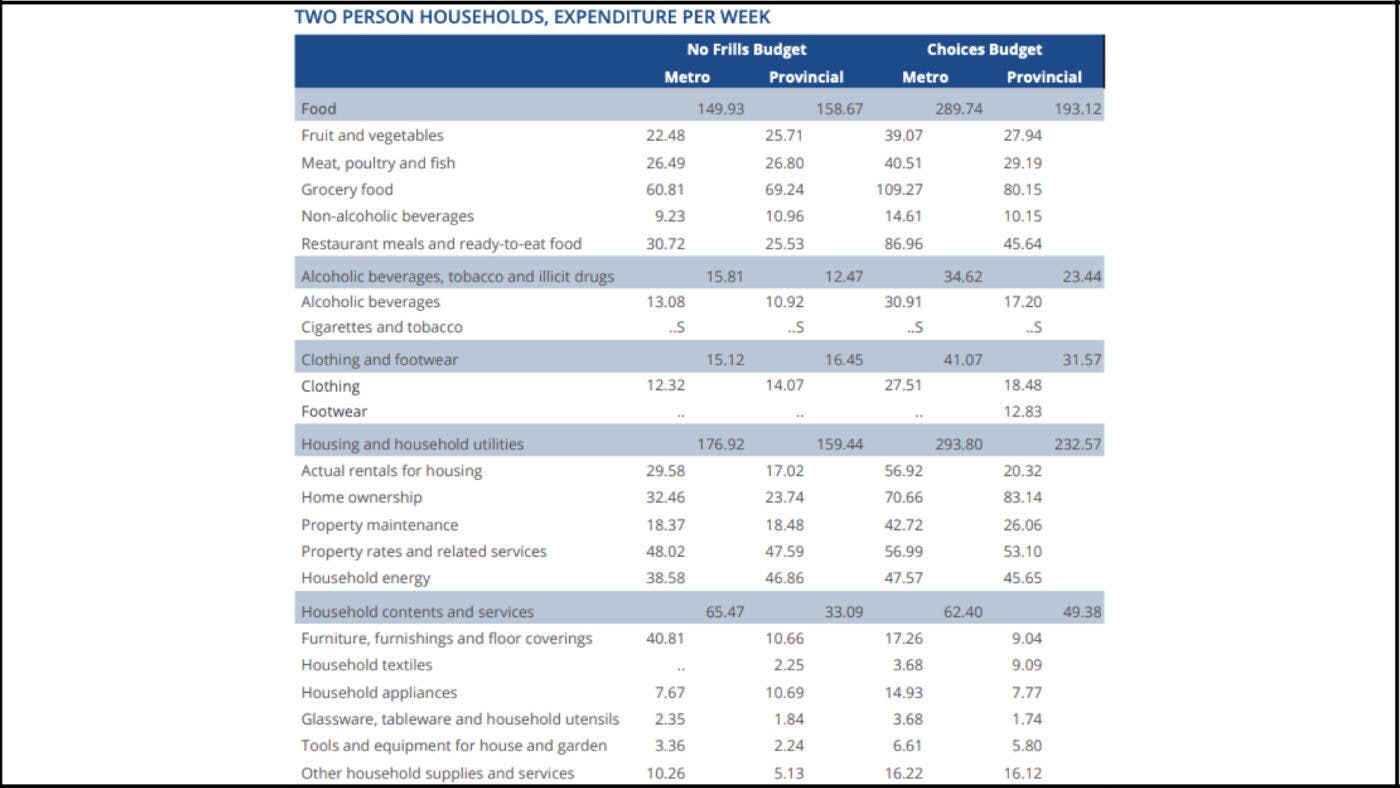

According to the latest NZ Retirement Expenditure Guidelines report by Massey University, the average couple living a ‘Choices’ lifestyle in one of the major cities spends $1,470 per week.

But at the time of the report’s release, superannuation for a couple was just $672 per week. A $798 difference.

Even if you want to live a “no frills” lifestyle in retirement, superannuation on its own does not provide enough, no matter where you live, or whether you’re single or in a couple:

The Massey University report, breaks down in detail how much you can spend each week on different items based on the lifestyle you choose.

The differences are large.

For instance, a “choices” lifestyle you can spend $39.07 a week on vegetables for two people.

Whereas if you were to rely solely on superannuation, this drops down to $17.47 a week.

Here’s what you could buy on the choices lifestyle every week:

And here’s what you could buy based on just the superannuation:

To look at another example, the choices budget has an alcohol budget of $34.62 a week. This drops to $12.29 on superannuation.

Similarly, the difference for eating out at a restaurant with friends goes from $89.96 to $23.88 a week.

So, sure, if you don’t invest in your future retirement you could have a much nicer house – right now. But you could miss out on the necessities and niceties of life, in your retirement.

Video published 23 August 2022

Let’s say you have $125,000 worth of useable equity within your own home.

And you’re considering borrowing all $125k so you can renovate your own home.

If you borrow this money, you’ll have a nicer house.

However, by borrowing this money you’ll have lost out on the ability to spend up to $625,000 on an investment property.

After 15 years, this investment property would have enough equity to contribute $385 a week to your retirement (adjusted for inflation).

This assumes that the investment property will grow in value by 5% a year, and that you’ll spend 25 years in retirement.

So prioritising a single investment property can make a substantial difference to your quality of life in retirement.

To see how a real life couple will achieve a comfortable retirement lifestyle using investment properties, read this case study about Tim and Jo.

This article isn’t designed to be negative, or to tell you to stop wanting nice things.

Instead, it's to encourage you to think about the potential trade-off between personal and investment spending.

If your finances dictate that you need to choose between either investing in property or improving your personal property (or buying a high ticket item), then it’s often a good idea to start investing first. Then, improve your lifestyle later.

That way your investments get more time in the market.

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Laine Moger, a seasoned Journalist and Property Educator holds a Bachelor of Communications (Honours) from Massey University and a Diploma of Journalism from the London School of Journalism. She has been an integral part of the Opes team for four years, crafting content for our website, newsletter, and external columns, as well as contributing to Informed Investor and NZ Property Investor.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser