Property Market

What’s a good rental yield in Auckland?

What’s a good rental yield in Auckland? See the latest data on median yields, how Auckland compares to NZ, and what investors should expect in today’s market.

Property Market

5 min read

Author: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Reviewed by: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

The median property investment yield in Christchurch is 4.8%. That compares to a median yield in New Zealand of 4.5%

We’re answering this question because property investors always ask: “What’s a good yield in today’s market?”

In other words, what sort of rental return should property investors expect?

When you see it asked online, most people respond: “Well, it depends.”

It depends on your strategy; it depends on where and what you buy.

It’s not a straightforward answer, but as a property investor you still want an answer.

Here at Opes Partners we want investors to be as informed as possible. I ran the numbers on all 12,958 Trade Me rental listings to find out what investors are accepting right now.

That way you can make an informed decision on your investment properties.

In this article, you’ll learn what a good rental yield looks like in Christchurch.

Here at Opes, we aim for 4.5-5% gross yield for a growth property in Christchurch. In Rolleston and Waimakariri, we aim for 4.3-4.6%.

For a yield property you would want to aim for a yield of 5.5% to 6.3%.

Remember, your gross yield is calculated as:

( Weekly rent x 52 ) / (current value).

The median gross yield in Christchurch is 4.8%.This is based on our analysis of 379 Christchurch City properties.

If you have a gross yield under 4.3%, you’re in the bottom quartile of investors. That means you’re in the bottom 25% of investors when it comes to yield.

But if your gross yield is over 5.4%, you’re in the top quartile. You’re in the top 25% of property investors in Christchurch City.

For comparison, the wider Canterbury region has a median gross yield of 4.7%.

Overall, Canterbury and Christchurch yields tend to be higher than Auckland, but lower than some other parts of the country.

But the “right” yield also depends on the type of property you’re buying.

A 4.5% gross yield is good for a growth property, like a townhouse. But a 5% gross yield would be bad for a yield property.

For standalone houses in places like Rolleston and Kaiapoi (Selwyn and Waimakariri District) we aim for a gross yield between 4.3-4.6%.

Find out instantly how much your property will earn or cost you per week

Find out nowTo get the estimated yield property investors are willing to accept we gather data from Trade Me and OneRoof.

The Trade Me listings show how much rent investors are currently advertising. We then match that rental information with OneRoof data to see how much those properties are worth.

This shows us the gross yield property investors are actually willing to accept. We then did this for every property on Trade Me.

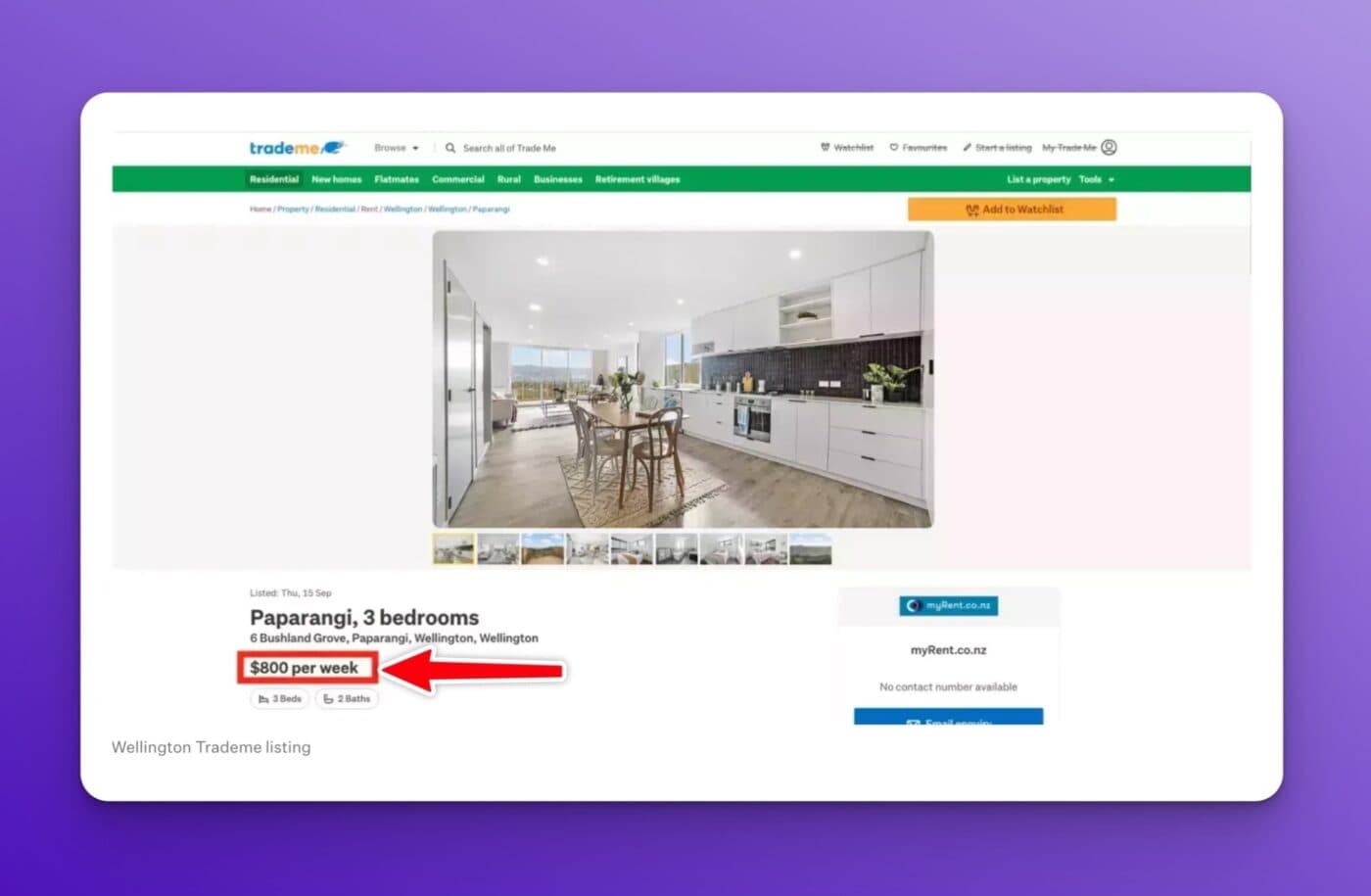

For instance, here is a property available for rent at the time we completed the analysis:

It’s a 3-bed New Build townhouse in Wellington, and it’s available to rent for $800 a week.

Then, we cross-referenced this with OneRoof’s estimated valuation.

And in this instance, this property is estimated to be worth $920,000, giving it a gross yield of 4.52%. Bang on average for the country.

We then use a computer to do this over 7,000 times. After cleaning up the data, we’ve now got figures no-one else has.

If you follow a lot of property investors on social media, you might think: “Why are these numbers so low? The numbers some investors talk about online are higher.”

Some investors calculate their gross yield using the price they paid 10 years ago, not what that property is worth today.

When you calculate the gross yield you should always use the value of the property today.

What you spent isn’t relevant. What matters is the yield you are getting based on what the asset is worth today. That’s because if your house has increased in value you could always sell your property and do something else with the money.

Christchurch yields have been steadily declining. In 1993, they were about 7.17%; today they are closer to 4.06%.

This graph uses a different data set, which is why the number is different from the above.

The reason yields have declined is that property prices have risen faster than rents. Historically, house prices have gone up by around 6% per year. At the same time, rents have increased by about 4-5% per year.

This is important. Sometimes property investors read investment books that are decades old. The specific yields mentioned in a 30-year-old book won’t be relevant today.

What was a realistic yield 5 years ago may be unachievable in today’s market.

This data isn’t here to give you a yes-or-no answer on whether to buy a specific property or not. It’s here to help you ask better questions.

Property is a direct form of investment. You’re not buying a whole city or region… you’re buying one specific property. And that property’s rental return will depend on its price, rent, condition and tenant demand.

So when you’re using gross yield to assess opportunities, compare the yield to that region’s range, not a national rule of thumb.

Use gross yield to screen deals, not approve them. Then move on to net yield and cashflow for a fuller picture.

Other tools you can use

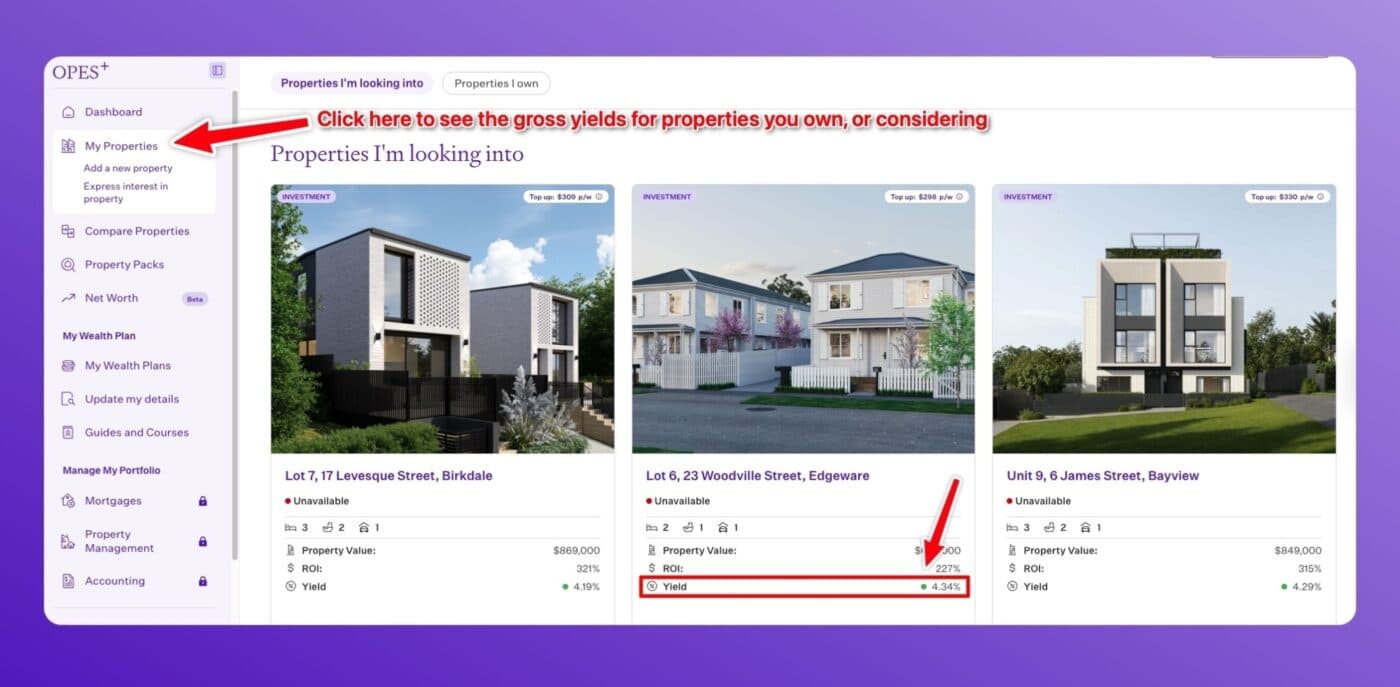

If you’re signed up with Opes+ you can track gross yield directly on the platform. Just head to My Properties to see the gross yield for properties you own, or ones you’re considering.

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Ed, our Resident Economist, is equipped with a GradDipEcon, a GradCertStratMgmt, BMus, and over five years of experience as Opes Partners' economist. His expertise in economics has led him to contribute articles to reputable publications like NZ Property Investor, Informed Investor, OneRoof, Stuff, and Business Desk. You might have also seen him share his insights on television programs such as The Project and Breakfast.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser