New Builds

Should I invest in a large-scale development?

So, in this article, we’ll discuss the four common concerns and drawbacks that go along with big developments.

New Builds

7 min read

Author: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Buying a New Build can sometimes mean taking on additional risk. Why?

A) Because you’re buying a building that isn’t yet standing in front of you.

B) Because sometimes you’ll be committed to purchasing a property that you don’t have bank finance locked in for.

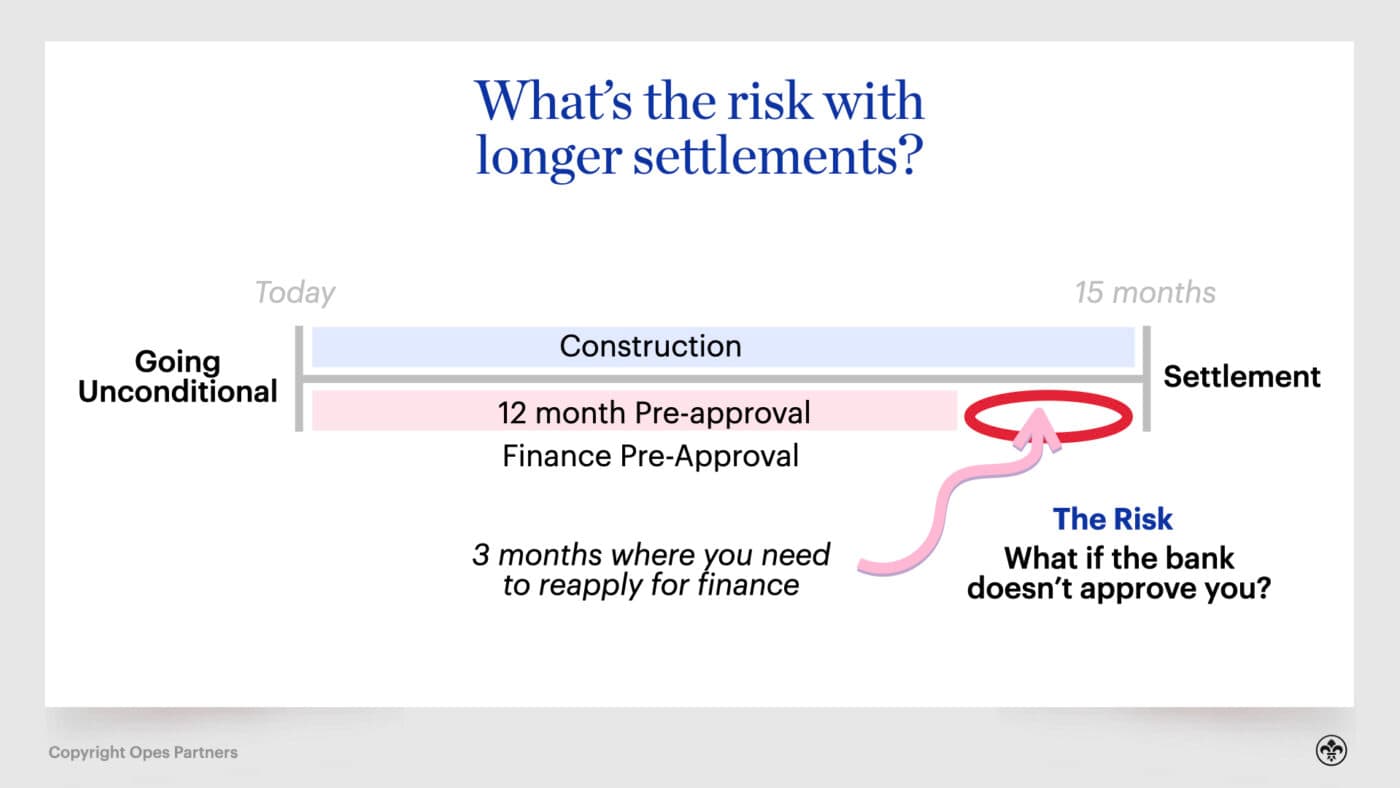

Even armed with a year-long preapproval from the bank, an investor will sometimes need to reapply for finance when it comes to settling on the property.

So it’s natural for investors to worry: What if I can’t get my finance reapproved?

In this article you’ll learn the risks and rewards of buying a turnkey property off-the-plans, along with how to minimise those risks.

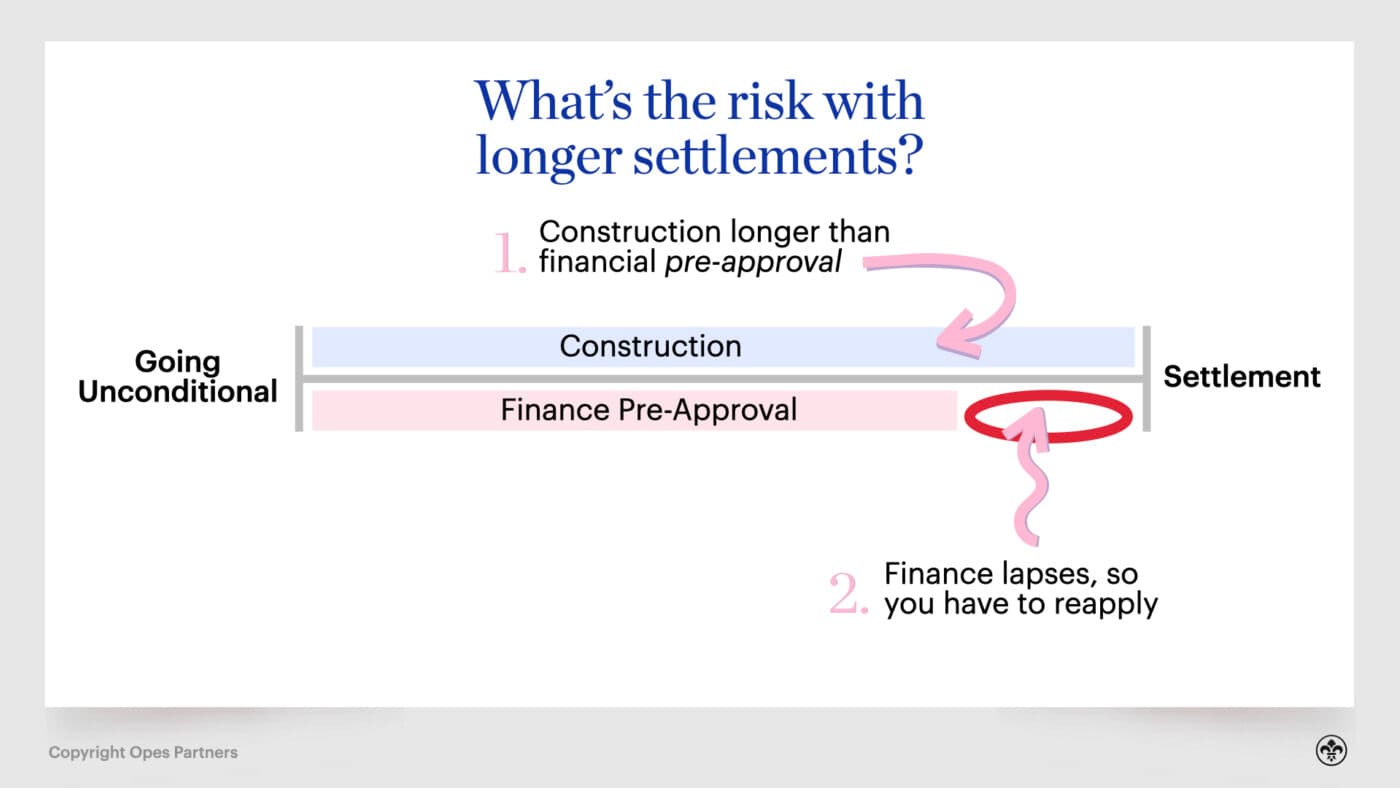

Sometimes when you buy a turnkey property off the plans, the construction period is longer than your finance preapproval period.

What does that even mean? Well, you the purchaser have to confirm and go unconditional on the contract before the property is built.

You then need to wait for the property to be built. And during that period you are unconditional – you can’t back out of the deal.

But, if there is a long time between confirmation and settlement, your finance may lapse. So you have to reapply.

Here’s an example –

Put simply, the risk is that bank rules – or something in your life – changes. Then, once the property is built, the bank won’t give you the money to purchase it.

You’re legally obliged to buy the property, but you perhaps don’t have the money for it. So how do you get around this?

Recently, there has been an increasingly longer lag between contracts going unconditional and settlements taking place.

That’s because:

So, you might be wondering how developers are finding people to buy these properties if they can’t confirm finance before going unconditional.

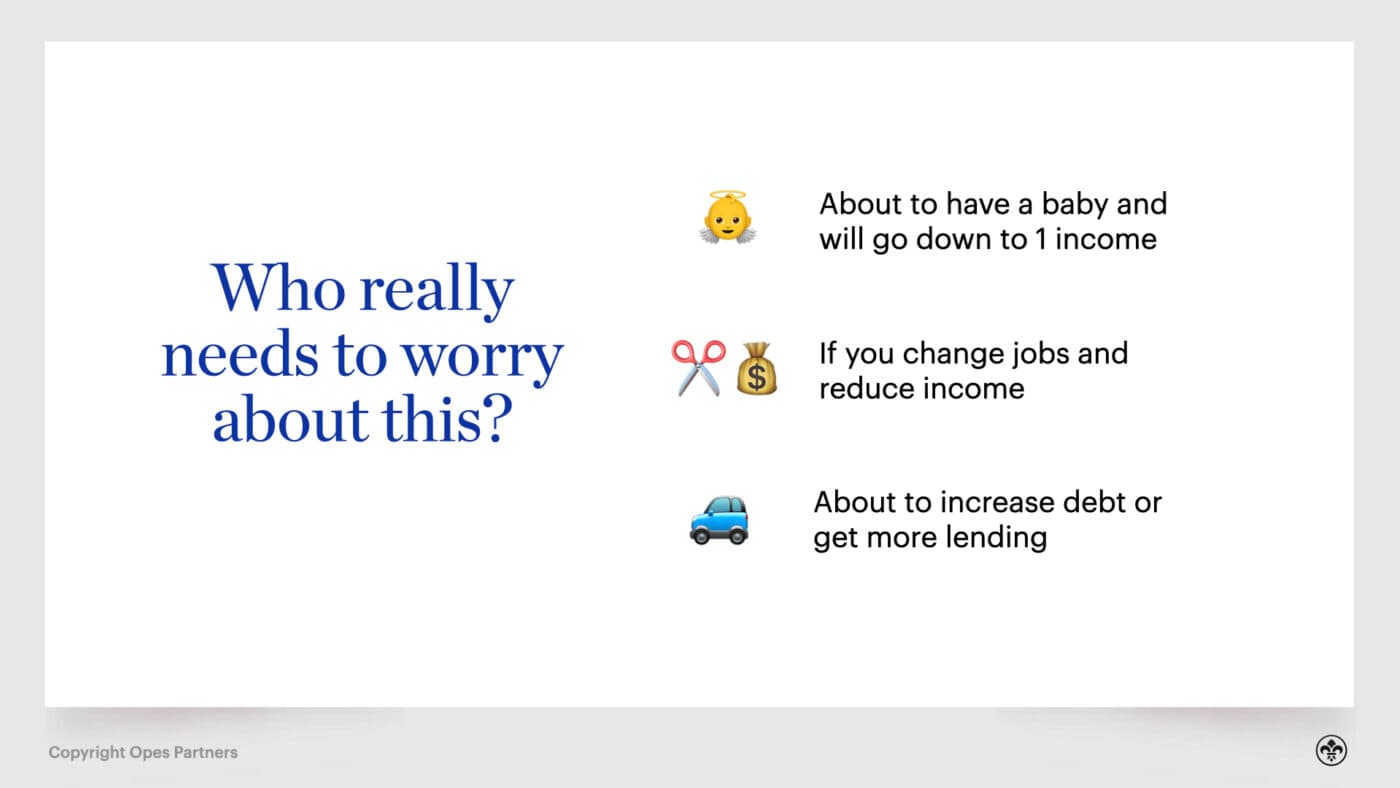

Generally, this risk is only really felt by investors who’s life circumstances are about to change.

Here are some examples of what we mean by this:

Why do these matter? Well in these circumstances the bank might approve your lending today (based on today’s income) but if your income drops, or your expenses rise, they might not approve you in a few months’ time.

So if you’re going to take a hit to your income, a shorter settlement period might be more appropriate, and these longer settlements might not be for you.

But if you’re someone with a stable income and don’t foresee a change in expenses, then you may not be worried about or impacted by this risk.

Even if you are impacted, here are three tactics you can use to give yourself the best shot at getting your lending approved at settlement:

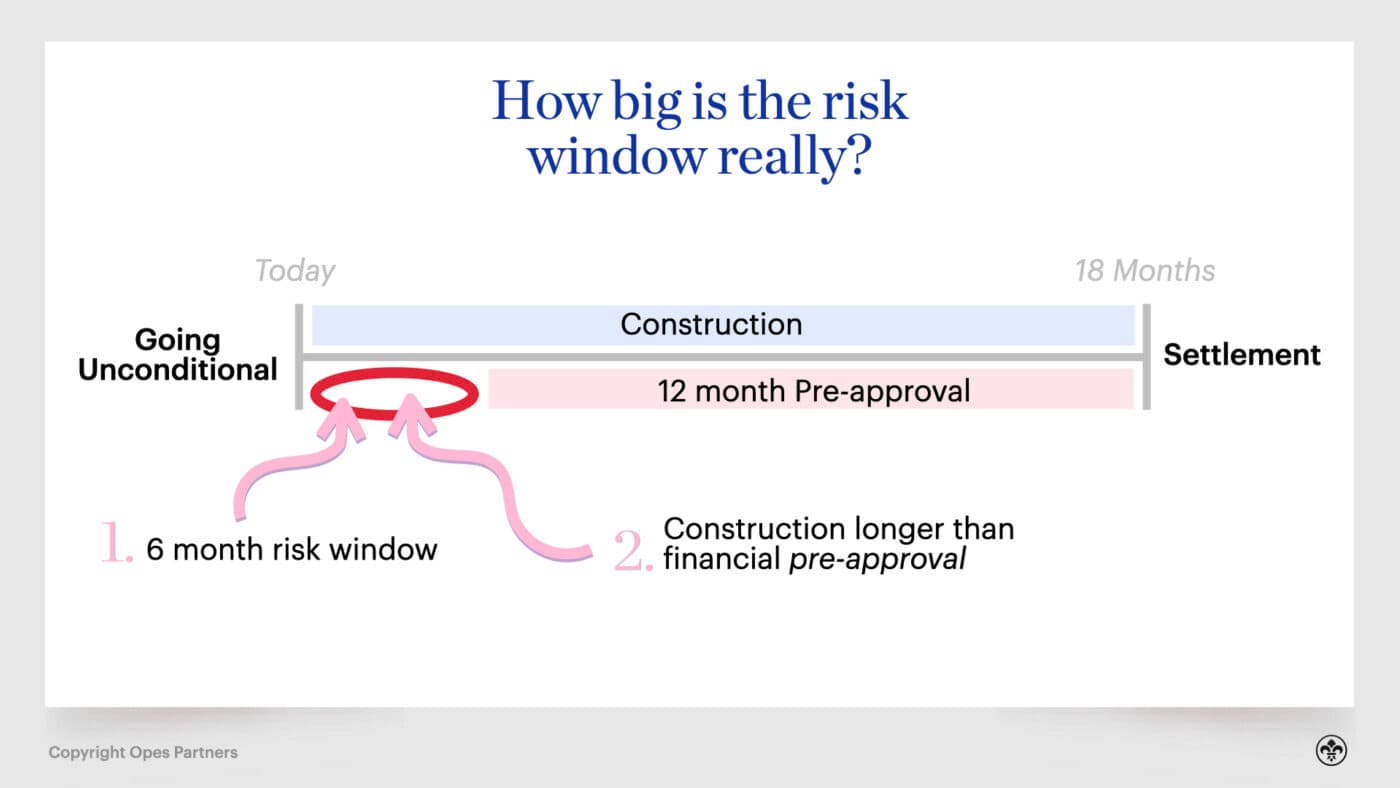

Let’s say you have 18 months to wait for your property to be built and settle. In this situation an investor may think they’ve got to wait 18 months until they apply for finance. So their “risk window” is 18 months.

That’s not the case.

Instead, the risk window is 6 months. That’s because after 6 months you can go and get a 12-month preapproval. That means your finance will still be approved by the time you settle.

That means you only have to worry about a change in circumstances for 6 months rather than 18.

Peter Norris, a mortgage adviser from Catalyst Financial, says a good mortgage broker should check in with you regularly, if not every month.

They’ll make contact with you to make sure that nothing has changed and you’ll still be on track to get the lending sorted when the time comes.

It shouldn’t be a case of let’s get a preapproval and then just leave you be until the house is finished, although he admits a lot of brokers do this, unfortunately.

So, it might be a good idea to suss out what sort of ongoing communication a mortgage broker is going to offer before setting out on this purchasing journey with them.

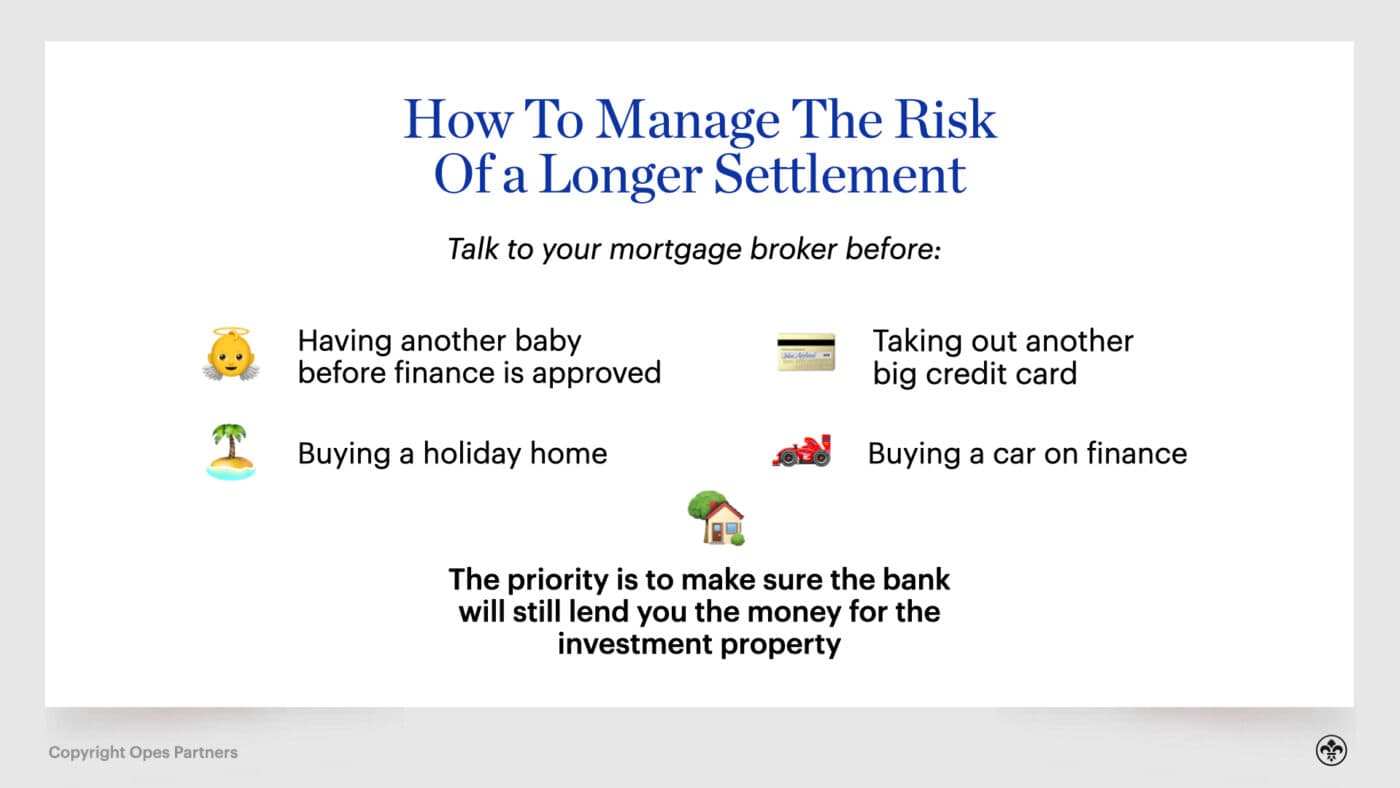

Don’t look at your broker sideways when they start telling you not to have a baby in the next year.

Yes, it sounds odd, but your mortgage broker will tell you, in no uncertain terms, not to make your financial situation worse during the time it takes to settle your building.

The main culprits are things like: extra credit cards; having another child; buying a holiday home; buying a car on finance.

Now it doesn’t mean you can’t do any of these things, but you should talk to your mortgage broker before doing them before it is set in stone.

For example, there is a real-world couple about to buy a New Build set to settle in 2023. The wife in this situation is 9 months pregnant and about to take a year’s maternity leave. The couple has decided to pursue the purchase because by the time the property settles she will be back at work. The finance preapproval will have this included.

This one is optional and won’t apply to all investors.

But a third way to minimise the risk that comes with a New Build is to work with an organisation that will guide you through the process and help you out if it all goes pear-shaped.

That’s what we do here at Opes Partners. So, for instance, if the investors we work with find they can’t settle a property, we’ll often find another investor to purchase the property instead (info on how this works below).

For instance, in early 2020 we were working with an investor who owned a business in Queenstown. She had three properties under contract. But, once Covid lockdowns hit, her business took a hit, and her income decreased.

That meant she could only settle on 2 of the 3 properties. So we found another investor to purchase the third property instead so that she wasn’t put in a tough financial position, or at risk of losing her deposit.

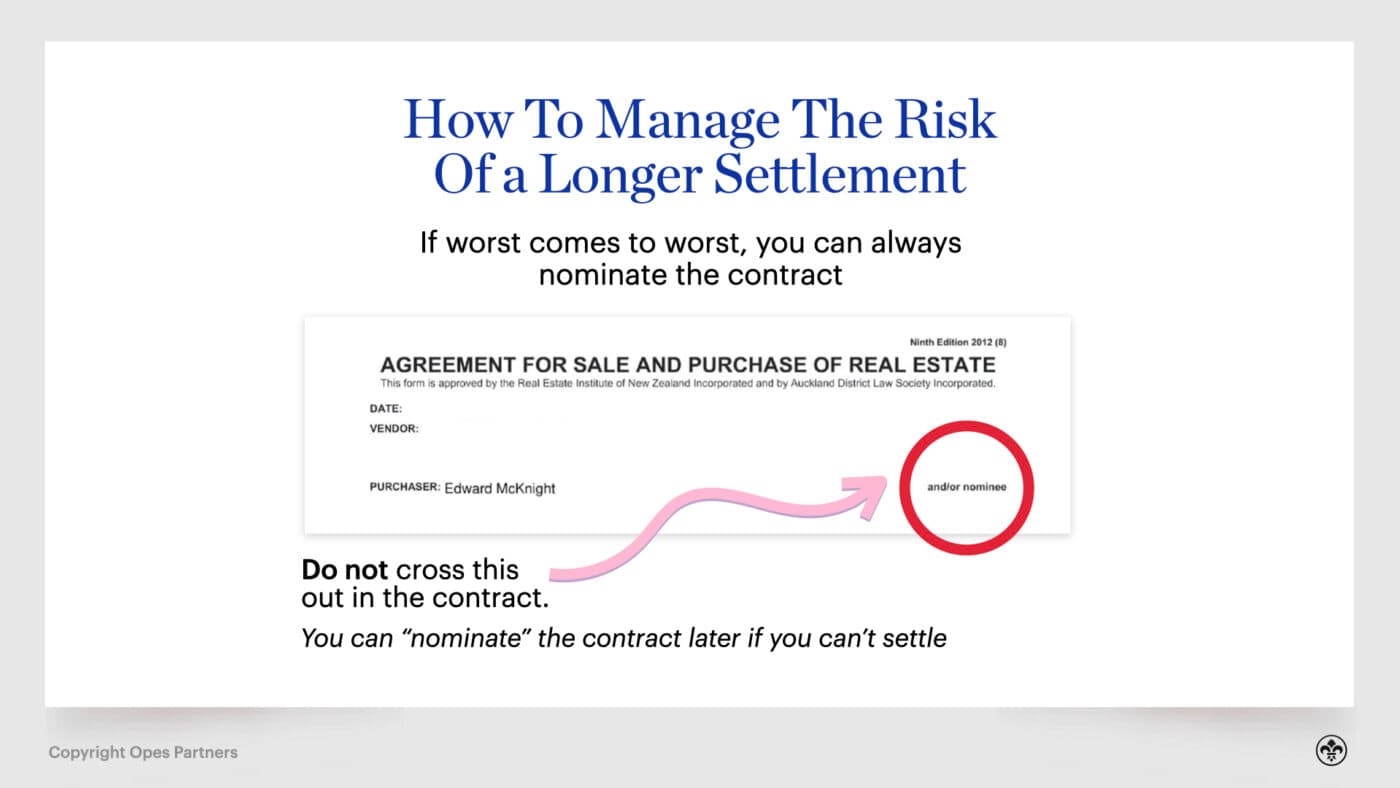

A very real concern for investors is to wonder what happens if the worst-case scenario does eventuate and you can’t settle.

In this instance you can nominate the contract, which means someone else can settle the contract.

In this case you’ll sign a “Deed of Nomination” and the contract gets transferred.

Why would someone choose to take your contract off you? Well, properties often go up in value during construction, so the property has most likely increased in value. In practice that often means the person getting the contract will pay less for the property than what it’s worth.

But what happens if you can’t find someone to nominate the contract to? The absolute worst, worst-case scenario is you lose your deposit. In the 8 years we’ve been running at Opes this has not happened to our investors once.

When they have been in a tough financial situation we have always found someone to nominate the contract to.

As the saying goes: “Where there is risk, there is often reward”.

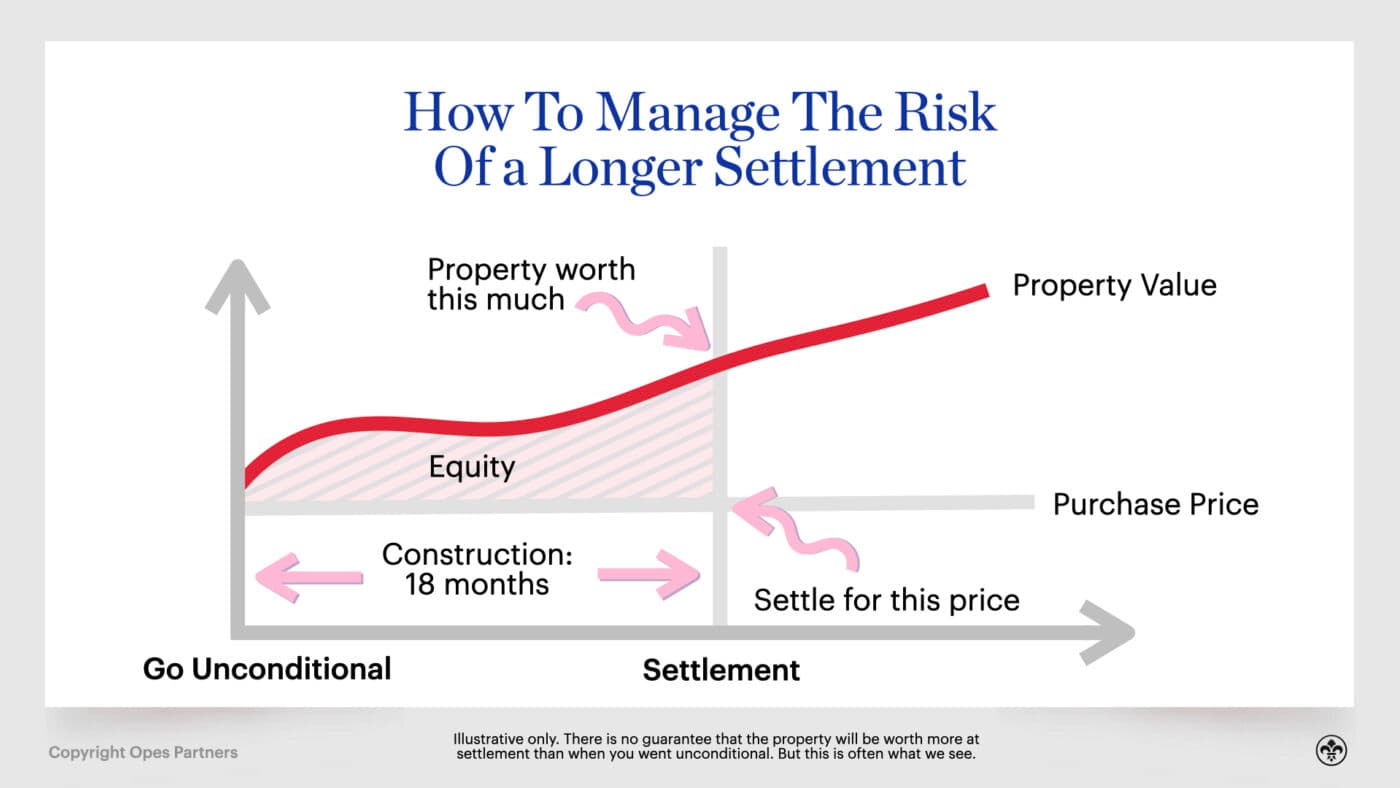

This is not a cliche. There are some definite benefits to a longer settlement.

For starters, the property often goes up in value during construction. That’s for two reasons:

So the benefit is that you only have to put down a 5-10% development deposit and still get the capital appreciation on the property.

And during that time you don’t have to worry about tenants, and cashflow is typically less of a concern.

We’ve often joked that the best construction timeframe is 15 years … if it took 15 years to build the property, the market would likely have appreciated, but you wouldn’t have had some of the risks.

Yes, there is a bit of a risk when buying New Builds, especially if there is a longer time frame between going unconditional and settlement.

It is up to you, the purchaser, to decide whether or not you’re willing to take that risk.

If you are looking to start a family, or change careers in the short term, you should definitely talk to your mortgage broker. In that case you may be better off finding a New Build that settles in the next 3-6 months.

But if you’re in a stable career and more kids aren’t on the horizon, then you might not be put off by a longer settlement period.

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Laine Moger, a seasoned Journalist and Property Educator holds a Bachelor of Communications (Honours) from Massey University and a Diploma of Journalism from the London School of Journalism. She has been an integral part of the Opes team for four years, crafting content for our website, newsletter, and external columns, as well as contributing to Informed Investor and NZ Property Investor.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser