Property Market

What’s a good rental yield in Auckland?

What’s a good rental yield in Auckland? See the latest data on median yields, how Auckland compares to NZ, and what investors should expect in today’s market.

Number Crunching

7 min read

The median gross yield in New Zealand is 4.5%. That’s the yield the average property investor is willing to accept.

We’re answering this question because property investors always ask: “What’s a good yield in today’s market?”

In other words, what sort of rental return should property investors expect?

When you see it asked online, most people respond: “Well, it depends.”

It depends on your strategy; it also depends on where and what you buy.

It’s not a straightforward answer, but as a property investor you still want an answer.

Here at Opes Partners we want investors to be as informed as possible. I ran the numbers on all 12,958 Trade Me rental listings to discover what investors are accepting right now.

That way you can make an informed decision with your investment properties.

In this article, you’ll learn what a good rental yield looks like in New Zealand.

A good gross yield depends on where you buy — but across New Zealand, 4.5% is the median

Across New Zealand the median gross yield is 4.5%.

Remember, your gross yield is calculated as:

( Weekly rent x 52 ) / (current value).

But averages can be misleading. What’s more useful is understanding the range most investors are in:

The good news: yields are rising.

When we ran this analysis on July 2025 data and December 2025, gross yields increased across most regions.

They only fell in Waikato and Taranaki.

Northland recorded the largest increase, rising from around 4.6% to approximately 5.3% in the latest data.

Just remember, in smaller regions (such as Northland, Southland and Manawatū-Whanganui) sample sizes are smaller. That means yields can move around more from one data run to the next.

Auckland tends to be more stable, simply because there is more data.

Rental returns vary significantly depending on location.

A “great” yield in one region may be completely normal (or even low) in another.

Take Southland, where the median gross yield is around 5.8%. Property values are generally lower, so yields tend to be higher.

The middle 50% of yields in Southland sit roughly between 5.5% and 6.5%.

Compare that to Auckland, where higher property values typically result in lower yields. In Auckland, the middle 50% of yields range from 3.2% to 4.6%.

This is why you should ignore blanket statements like “any property with a gross yield under 5% is rubbish”. That might be true in one part of the country, but could be completely unrealistic in another.

Otago is another interesting example. While its median yield is relatively high at 5.7%, the range is much wider.

The middle 50% of yields span from 4.2% to 6.6%. That’s because property prices in some parts of Otago are cheap, whereas other parts are expensive.

I get it, it’s tempting to chase the highest yield you can find.

On paper that might make it look like everyone should be investing in the same high-yield regions.

But that’s not how most experienced investors make decisions.

Many deliberately accept lower yields to invest in main centres. That’s where house price growth tends to be more consistent.

Higher yields often appear in smaller towns. While that can mean stronger cashflow, it can also come with:

In the same way a lower-yield property can still be an excellent investment if everything else stacks up.

So far, we’ve looked at gross yields across regions. But yields can also vary within a single council area.

A council can include multiple towns and dozens of suburbs, each with very different property types and tenant demand.

Here’s a Wellington map, showing the highest and lowest yielding suburbs.

What do you see? Generally, properties located in the CBD have higher gross yields.

As properties move away from the inner city, yields fall sharply. They then gradually increase again as properties move further out of town.

This trend is also seen in the Auckland, Christchurch and Hamilton property markets.

Properties in the centre of a city tend to be cheaper. They’re compact, and you’ll find more apartments and townhouses.

Even though they’re smaller, these properties get a good amount of rent.

Suburbs on the CBD’s fringes tend to be more expensive. They’re usually bigger and aren’t affordable for the average renter.

Most people who have the money to live in expensive suburbs can afford to buy their own home. That means there is less tenant demand, which means softer rents.

Think Parnell in Auckland, Fendalton in Christchurch or River Road in Hamilton. That’s why these suburbs have lower yields.

As properties move further out of town, yields pick up.

To get the estimated yield property investors are willing to accept we gather data from Trade Me and OneRoof.

The Trade Me listings show how much rent investors are currently advertising their properties at. We then match that rental information with OneRoof data to see how much those properties are worth.

This shows us the gross yield property investors are actually willing to accept. We then did this for every property on Trade Me.

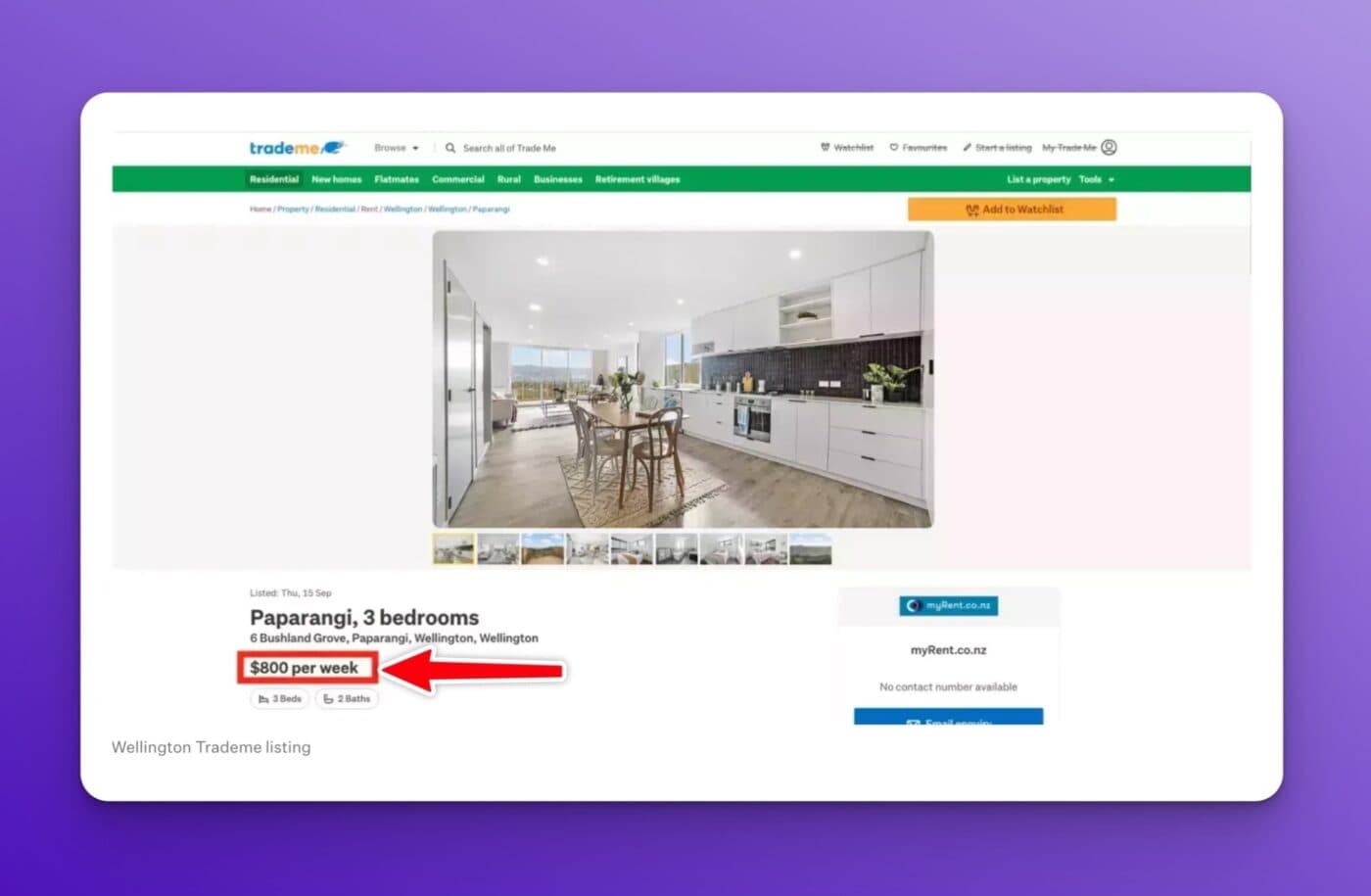

For instance, here is a property available for rent at the time we did the analysis:

It’s a 3-bed New Build townhouse in Wellington, and it’s available to rent for $800 a week.

Then, we cross-referenced this with OneRoof’s estimated valuation.

And in this instance this property is estimated to be worth $920,000, giving it a gross yield of 4.52%. Bang on average for the country.

We then use a computer to do this over 10,000 times. After cleaning up the data we’ve now got figures no-one else has.

If you follow a lot of property investors on social media, you might think: “Why are these numbers so low? The numbers some investors talk about online are higher.”

Some investors calculate their gross yield using the price they paid 10 years ago, not what that property is worth today.

When you calculate the gross yield you should always use the value of the property today.

What you spent isn’t relevant. What matters is the yield you are getting based on what the asset is worth today. That’s because if your house has increased in value you could always sell your property and do something else with the money.

free calculator

Plug in a property's price and rent to calculate its gross yield - and see how it compares to the regional medians you just read about.

Calculate my rental yieldThis data isn’t here to give you a yes-or-no answer on whether to buy a specific property or not. It’s here to help you ask better questions.

Property is a direct form of investment. You’re not buying a whole city or region … you’re buying one specific property. And that property’s rental return will depend on its price, rent, condition and tenant demand.

So when you’re using gross yield to assess opportunities, compare the yield to that region’s range, not a national rule of thumb.

Use gross yield to screen deals, not approve them. Then move on to net yield and cashflow for a fuller picture.

Other tools you can use

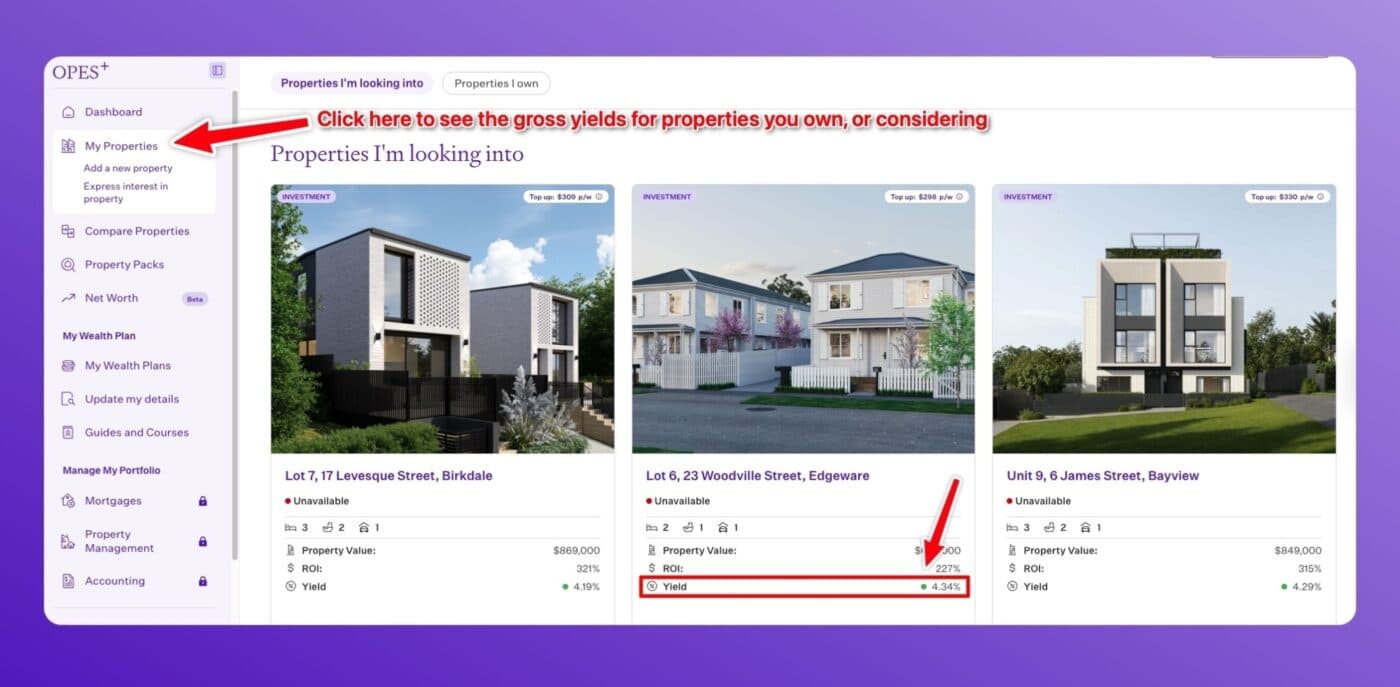

If you’re signed up with Opes+ you can track gross yield directly on the platform. Just head to My Properties to see the gross yield for properties you own, or ones you’re considering.

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Ed, our Resident Economist, is equipped with a GradDipEcon, a GradCertStratMgmt, BMus, and over five years of experience as Opes Partners' economist. His expertise in economics has led him to contribute articles to reputable publications like NZ Property Investor, Informed Investor, OneRoof, Stuff, and Business Desk. You might have also seen him share his insights on television programs such as The Project and Breakfast.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser