Law

How do I invest in New Zealand … as a Singaporean National?

Discover how Singaporeans can invest in NZ property. Understand benefits and exemption from government approval via the Overseas Investment Office.

Law

7 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Peter Norris

Mortgage broker for over 10 years, property investor and Managing Director at Opes Mortgages

Are you wondering "Can foreigners buy property in NZ?"

Overseas people usually cannot buy a house or land in New Zealand, but there are exceptions. Generally, New Zealanders, Australians and Singaporeans can buy property in New Zealand.

Other foreigners can also buy a property in NZ, but the options are very limited or you need to apply for government permission.

Why’s this? In 2018, the newly-elected Labour government introduced a foreign buyer ban.

While that sounds tough, the legislation does not have as much teeth as it may seem.

This article breaks down who can buy an investment property in NZ, and what you can buy.

There are lots of benefits to buying an investment property here as a foreigner.

There are many pros to buying an investment property in NZ.

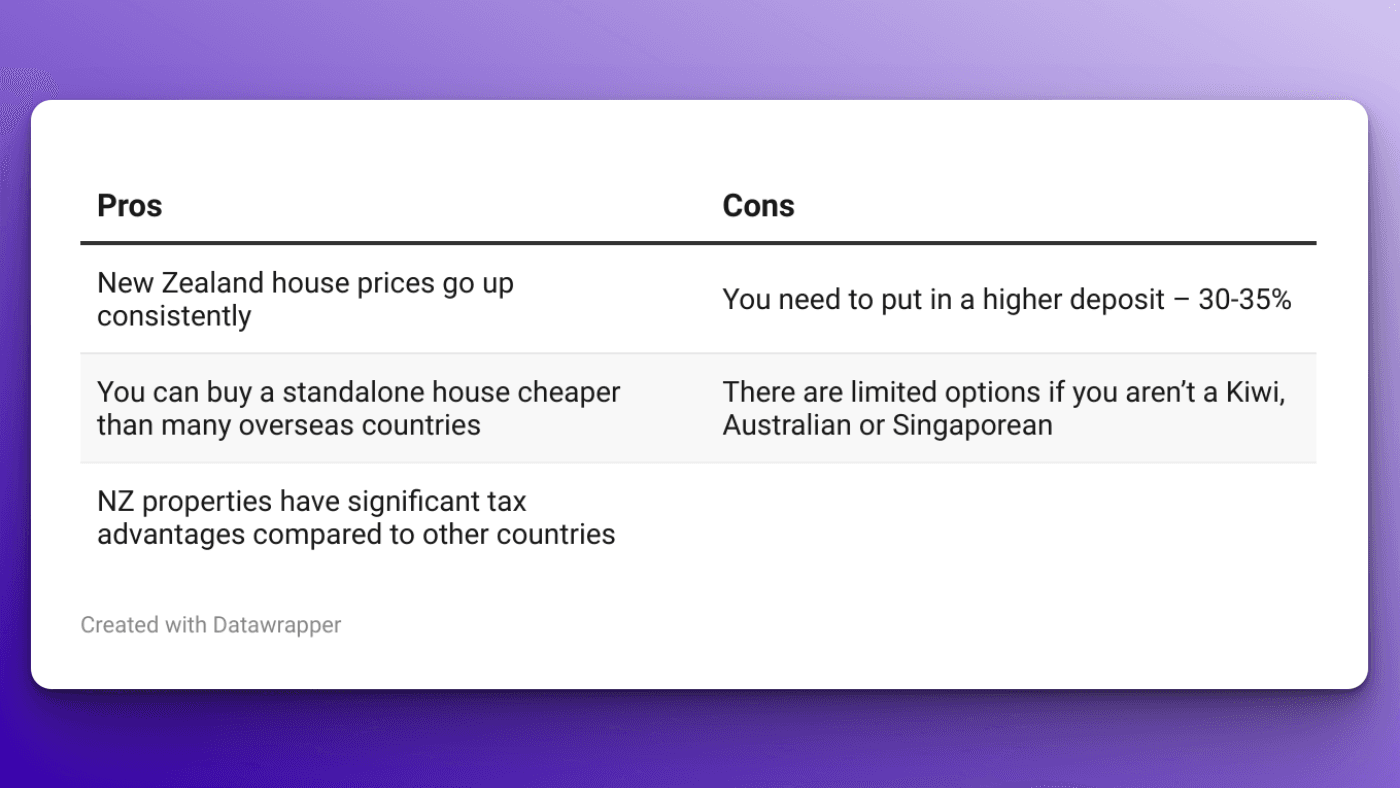

Our house prices have tended to increase consistently. Since 1992, Auckland house prices have risen 6.9% a year.

Outside our largest city, house prices have risen on average 6.2% per year.

On top of this, standalone houses are cheaper than some other countries. You can currently buy a 4-bedroom standalone house in Canterbury for NZ$750k - $800k.

Some people – especially from Singapore – like to purchase these properties. That’s because they are significantly cheaper than if they were to buy an equivalent property in Singapore.

But the biggest surprise for foreign investors is the lack of taxes. New Zealand doesn’t have any stamp duty; you don’t have to pay tax when you buy a house.

That is significantly different to Australia and Singapore. A foreign investor buying an $800k property in Melbourne would need to pay over $100,000 in stamp duty.

NZ also doesn’t have capital gains tax, like Australia does.

And, for many investors, NZ property offers significant tax advantages compared to other countries.

That said, banks need higher deposits for foreign investors. Almost all will ask for 30-35% because they’re considered a higher risk.

On top of this, if you aren’t a NZ, Australian or Singaporean citizen, you don’t have many options. You can generally only buy certain apartments and townhouses that are government-approved.

If you're wondering "Can foreigners buy property in New Zealand?", the answer depends on your residency status.

Buyers fall into one of three categories, and this will determine what you can purchase.

Here is a simple flow chart that can help you understand what property types you can buy within NZ.

Let’s go through each of these categories.

If you are a New Zealand citizen you can buy any sort of residential or commercial property.

You’ll face no restrictions through the Overseas Investment Act. It doesn’t matter if you’re in the country or not.

This also applies to Australian and Singaporean citizens so long as you are not purchasing “sensitive” land.

Sensitive land tends to be farmland, rural, or land by a river, sea, reserve or lake. Usually, a property lawyer will pick up if the land you’re attempting to buy is sensitive.

Permanent residents of NZ, Australia and Singapore can also buy residential property.

The only condition here is that you are “ordinarily resident” within NZ.

This means you must:

Let’s say Lisa is a permanent resident in NZ, but she’s spent the last 6+ months overseas contracting for her company.

Lisa’s no longer an “ordinarily resident”. She can’t freely buy residential property and will fall into another category.

This applies to anyone who:

If you fall into this category, you can only buy one property, and it can’t be used as an investment until:

At that point, you become an “ordinarily resident” again. Then you can convert it into an investment property.

This will not be a good way to purchase your first investment property in NZ, particularly if you have no intention of moving here.

That’s because you won’t meet the conditions of approval.

If you don’t meet any of the above criteria, there are two types of residential properties you can still buy.

A developer building a large apartment block can apply for an exemption certificate. This allows them to sell up to 60% of their units to overseas buyers.

The requirements are largely the same as for apartment developments.

However, a hotel developer doesn’t need an exemption certificate.

But the foreign buyer does need:

That stops overseas buyers from purchasing a hotel unit and then choosing to live in it for a large part of the year.

Here at Opes, we are currently seeing a lot of foreign buyers purchasing property in New Zealand.

There is a pair of teachers living in Hong Kong, earning Hong Kong dollars. There’s another one on a cruise ship. But the majority live either in Australia, England or Singapore.

Based on this experience – here are the challenges we see foreign investors facing when they are buying in NZ:

Jo and Steve live in London. Jo is a Kiwi and Steve is Canadian. They want to buy property in New Zealand.

The banks won’t be so keen on having Steve (as a Canadian) on the loan documents. This means his income might not be considered in the application.

So, this can add a layer of complexity. Ideally, Jo would have a strong enough income to service the mortgage herself.

Many banks generally won’t lend money to foreign buyers who are self-employed.

Similarly, they usually won’t include any bonus or commission income. So, if you are in a role like sales, where the bulk of your salary is commission, you may find it hard to buy a property in NZ.

When you apply for a mortgage, NZ banks want to know how much income you earn, and what your expenses are.

Because you aren’t in the country, banks need even more information to feel comfortable lending to you.

So, if you’re in a non-English speaking country you may need your tax returns and bank statements translated.

This adds complexity and costs.

Yes, any foreign buyer can buy an investment property within New Zealand. But, some foreign buyers will face more restrictions than others.

If you’re an NZ, Australian or Singaporean citizen, you have more options compared to someone who is Estonian, for example.

Founder, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser