Property Investment

What should my retirement plan look like?

Thinking about retirement? The Epic Guide to Retirement Planning is the guide that will give you the knowledge so you can plan for your retirement in 2026

Wealth

5 min read

Author: Nefe Marson

Financial adviser at Opes. Formerly a senior adviser at one of NZ largest investment firms. Owned 3 properties by 30.

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

A Wealth Gap is the difference between:

Said another way, if you continue doing exactly as you are now … how much money will you have by the time you retire, and will it be enough?

If you aren't on track for your goals – that’s called a Wealth Gap.

Spoiler alert: Most Kiwis have one.

In this article, you’ll learn what a Wealth Gap is, and how to close that gap before it’s too late.

Imagine your perfect lifestyle, where you don't have to go to work. Imagine how much money you need in the bank to make that happen. It might be $1 million (for example).

And let's say you want that dream lifestyle in 15 years.

Now think about your current investing. Is that enough to create that $1 million in 15 years?

If the answer is no ... you have a Wealth Gap.

Because a Wealth Gap is the difference between how much wealth you want (your goal) ... and the wealth you are on track to create.

What happens if you don't close your Wealth Gap?

You'll likely need to spend less money in retirement. That means and missing out on some of the things you want to do.

Or, you might have to work longer to make that dream lifestyle happen.

At Opes Partners, we sit down with over 2,000 Kiwis every year to map out their Wealth Plan.

Almost all of them discover the same thing: they aren’t investing enough to fund the lifestyle they want in the future. They have a Wealth Gap.

The reality? Most of us know we should invest more … we just don’t.

So how do you figure out your Wealth Gap?

Well, you need to run some numbers. And the best way to do this is to create a Wealth Plan.

This shows you where you’re at today, where you want to be, and how to close that Wealth Gap.

You can either calculate this with the help of a financial adviser. (You can book a free meeting here).

Or you can create your own Wealth Plan for free within Opes+. That's our free property investment app.

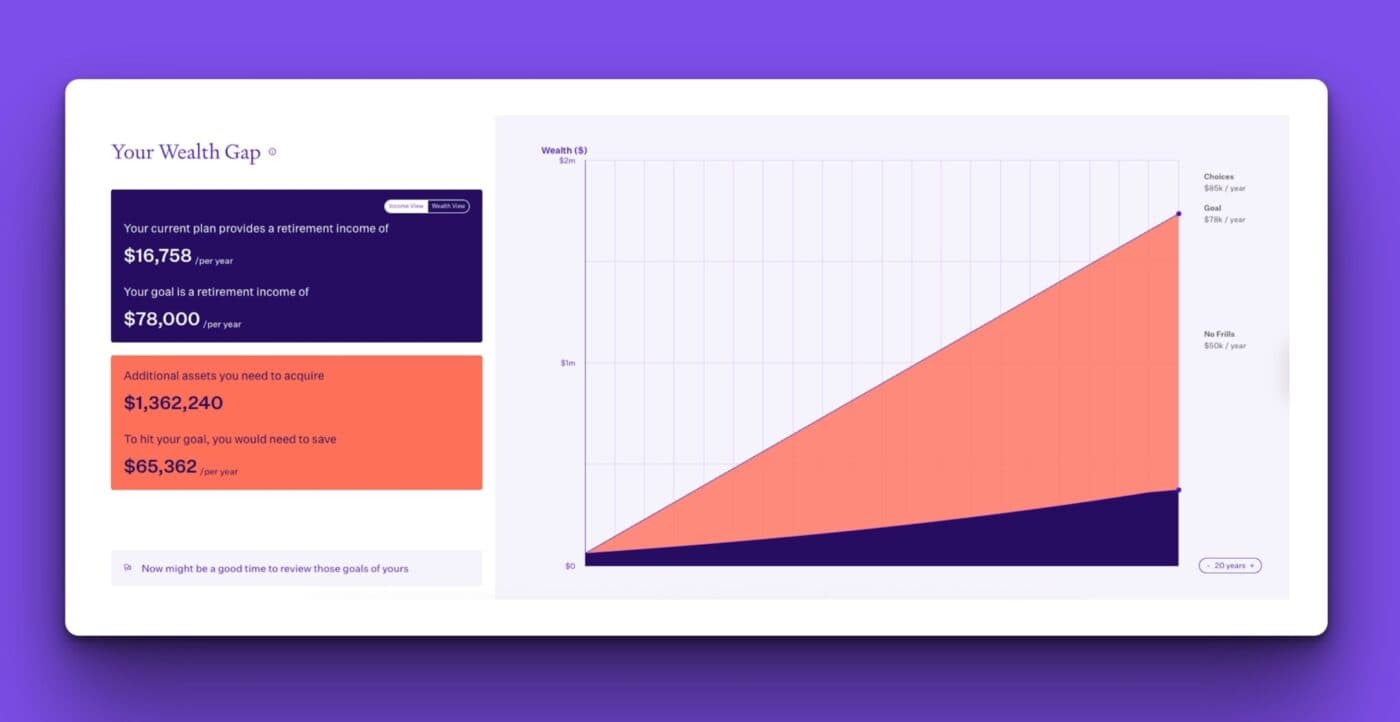

Let’s say, Peter and Sam are both 45. They earn $120,000 a year between them, and have saved $60,000 in KiwiSaver.

They dream of spending $1,500 a week (78k per year) in retirement – a lifestyle that Massey Uni calls the “Choices” lifestyle (i.e. comfortable, not extravagant).

Now, let’s run the numbers using the Nest Egg strategy.

If they keep doing what they’re doing – paying off the mortgage and contributing to KiwiSaver – they’ll be able to spend just $322 a week (16,758 per year).

That's if they don't count the NZ Super and just treat it as a bonus.

That’s $1,178 short every single week. For 25 years.

To close the gap, they need to create $1,362,240 in extra assets by the time they retire.

Shocking? Maybe. But this is the reality for thousands of Kiwis.

Why would they not put NZ Super within their plan? Many of the investors I work with at Opes Partners want to treat NZ Super as a bonus.

Especially if they are under 50.

That's because there is uncertainty about what it'll look like 15+ years time.

NZ Super will probably still be around. But it likely will look different than it does today.

That's why many investors aim to build enough wealth to fund their retirement independently. And then treat NZ Super as a bonus.

To close your Wealth Gap, you need to find a way to build your wealth.

And you get that by investing in more assets that grow in value over time.

This could be shares, funds, savings.

But, the option that a lot of Kiwis choose is investment property.

(That’s what we focus on here at Opes Partners too, so we’ll stick with investment property for the rest of the article).

It’s a misconception that you need 10+ properties to retire well. You don’t.

In practice, most investors find they will be set up for a comfortable retirement with just 2-5.

Let’s go back to Peter and Sam.

They want $1,500. But what they are currently on track for a $560 shortfall.

So, they buy two investment properties:

Fast-forward 20 years and those properties could grow in value substantially.

Based on these projections, Peter and Sam could be on track to spend $1,737 a week.

That’s more than the $1,500 they dreamed of.

NZ Super doesn’t give you enough money to pay for everything you need in retirement.

That’s according to the latest NZ Retirement Expenditure Guidelines report by Massey University.

If you plan to retire at 65 and live until 90 (fingers crossed), you’ve got 25 years of non-working life.

The latest research by Massey University says a relatively cheap ‘no-frills’ retirement lifestyle costs costs $781 a week. That’s for a single person living in Auckland, Christchurch or Wellington.

Because superannuation is currently $538, that means the average retiree living alone will still be $243 a week short.

Now not everyone wants to live the ‘no-frills’ lifestyle.

And similarly, not everyone wants to play rounds of golf and eat out at restaurants. Some people just want a ‘comfortable’ retirement.

Whatever a ‘comfortable retirement’ looks like for you, NZ Super will likely not be enough.

This article has thrown around a lot of numbers… and they can sound really scary.

But this article isn’t designed to be negative. It’s here to get you thinking.

Most Kiwis have a Wealth Gap. That’s normal.

The key is knowing what yours is and having a plan to close it.

That's why you can now calculate your Wealth Gap for free within Opes+. Click here to create your account and build your own Wealth Plan.

Financial adviser at Opes. Formerly a senior adviser at one of NZ largest investment firms. Owned 3 properties by 30.

Nefe is a Registered Financial Adviser at Opes Partners with 7 years’ experience in financial services. Before joining Opes, she was a senior adviser at one of New Zealand’s largest investment firms, managing $13 million in KiwiSaver and managed funds. She’s helped clients invest over $26 million in property and owned 3 properties before her 30th birthday.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser