Mortgages

How do I get a mortgage and pay it off?

This 9,500-word Epic Guide to Mortgages is the definitive article on how to get a mortgage and pay it off faster, today in 2026. The Ultimate Guide.

Mortgages

9 min read

A revolving credit is a type of mortgage, where a small part of your home loan acts like a big overdraft.

And instead of paying interest on the full amount, you only pay interest on the balance you haven’t repaid.

In New Zealand, it’s commonly used as a tool to pay down debt faster.

But revolving credits can be hard to grasp.

In this article you’ll learn exactly what a revolving credit is, how you set one up, and if using one could be right for you.

A revolving credit mortgage is a single account that works like an overdraft on a home loan rate, where you only pay interest on the balance you still owe.

Let’s say you convert part of your mortgage into a revolving credit. It will act like an overdraft that’s already maxed out, and you still have to pay it back.

The debt doesn’t go away… it just changes shape.

Here’s an example of how it works.

You have a $600k mortgage, and you choose to convert $15k of that debt into a revolving credit.

Now:

You now set about paying off that -$15,000 like you would an overdraft to bring it back to $0.

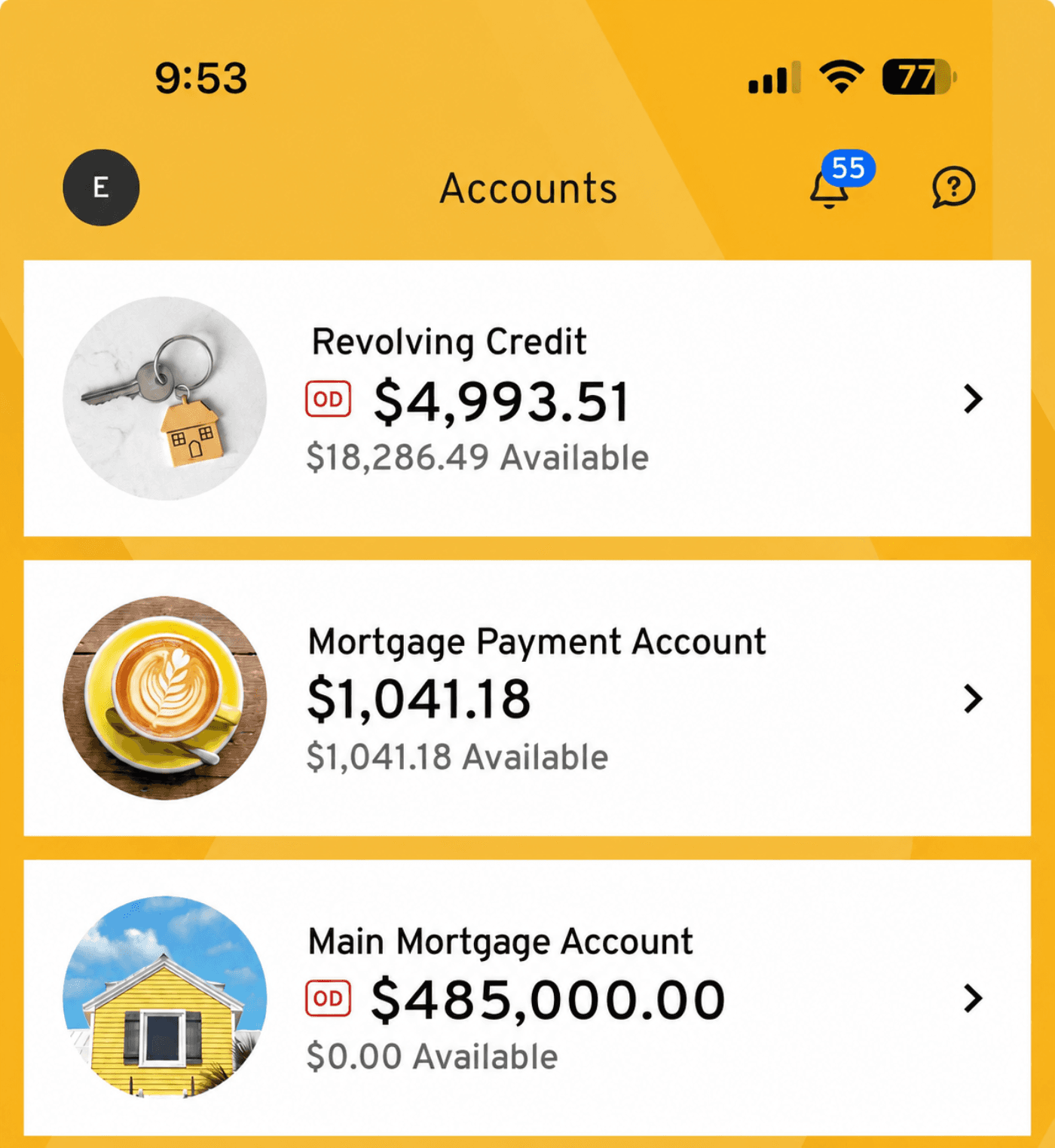

Here’s what a revolving credit could look like in your bank app. This example comes from ASB:

In this example the investor has a $485,000 main mortgage. You can also see their mortgage payment account.

This is where the payment for that main mortgage comes from (in this investor’s set-up). However, some investors set up that payment to come directly from the revolving credit account.

Then you can also see the revolving credit. They currently owe just under $5,000 on that revolving credit and have just over $18,000 available. That means the total revolving credit limit is about $23,000.

That $18,000 they have available (and have saved up) is helping them save on interest. They’re only paying interest on the $4,993.

There are a few important differences though:

There are two types of revolving credit:

| Type | What it means |

| Reducing | Your available limit reduces over time, so you are gradually forced to pay it down (it’s like a standard principal-and-interest loan) |

| Non-reducing | Your limit stays the same, so you need to be disciplined about paying it down yourself (like an interest-only loan) |

As a rough guide, revolving credit limits often start from around $5,000 and can go up to about $200,000–$250,000, depending on the bank and your situation.

To set up a revolving credit you can work with a mortgage broker or directly with your bank.

Work out how much extra cash you can realistically put towards the mortgage over the next 12 months.

That becomes the rough limit on the revolving credit.

Then your salary and spare cash flow through that account, which helps reduce the balance you’re charged interest on.

The simplest way to think about a revolving credit is as a goal-based savings plan for your mortgage.

Here at Opes we call this the Mortgage Buster strategy.

Instead of waiting until you’ve saved a lump sum to pay extra off your mortgage, you create that lump sum upfront using a revolving credit.

| Step | What happens |

| 1 | Set up a ~$15,000 revolving credit (choose a limit that suits you) |

| 2 | It immediately reduces your main mortgage by $15,000 |

| 3 | Put your spare cash into the revolving credit until it’s paid off |

| 4 | Once it’s repaid, take that money and use it all to pay off your bigger mortgage |

| 5 | Repeat the process |

For instance, let’s say you can put an extra $300 away a week. This adds up to $15,600 in a year, but we’ll say $15,000 to keep things simple.

If your mortgage was $600k, putting an extra $15,000 a year towards it could save about $279k in interest over the life of the loan.

That would help you become mortgage-free about 13 years earlier.

That’s based on a 5% interest rate and 30-year mortgage.

By setting up your mortgage this way you are setting yourself a goal of how much extra you want to save in a year.

However, revolving credits give you more flexibility compared with just committing to a higher repayment. That’s because you can take money in and out as easily as a transaction account.

There are different ways investors can set up their revolving credit. One way is to keep it separate from your normal spending account, then just use a revolving credit to park your savings.

Another way is making your revolving credit account your normal everyday spending account.

Here’s how that second option works:

Let’s say you earn $2,000 a week.

Step 1: You start with a revolving credit balance of -$15,000.

Step 2: Your salary lands in the account. That immediately reduces the balance to -$13,000.

Step 3: During the week your bills and spending come out of the account. As that happens the balance starts moving back towards -$15,000.

But interest is calculated every day, then charged once a month. So any money you have in there saves you interest (as long as it’s in your account).

Step 4: At the end of the week you might have $300 left in there, so the balance is reduced to -$14,700.

Step 5: The next week your salary lands again and the cycle repeats. Over time that leftover $300 a week steadily pays the revolving credit down towards zero.

Revolving credits can help you pay less interest and keep access to spare cash, but it only works well if you’re disciplined.

| Pros | Cons |

| Flexible – money you put in can usually be taken back out again. | Higher interest rate – revolving credit is usually on a floating rate, which is often higher than fixed rates. |

| Can reduce interest – while your salary or savings sit in the account, they reduce the balance you’re charged interest on. | Easy to overspend – because the money is available, some borrowers keep redrawing it. |

| Useful in emergencies – if your car breaks down or an unexpected bill comes up, you may be able to access the money again. | Not suited to the whole mortgage – most people only use revolving credit for a smaller portion of their loan. |

That’s why most borrowers don’t put their entire mortgage on revolving credit.

Instead, a mortgage adviser will usually help you choose a realistic limit. This might be enough to make progress on the mortgage, but not so high that you’re paying floating rates on more debt than necessary.

Revolving credit isn’t just for paying down your mortgage. It can also be useful when you need access to money but won’t spend it all at once.

#1 – New Build deposits

When buying a New Build you often pay a 10% deposit upfront and the remaining 10% deposit at settlement. A revolving credit can give you access to the full deposit from day one, while only charging interest on the amount you’ve actually used.

#2 – Renovations

If you’re planning a $50,000 renovation, you probably won’t spend the money all at once. Rather than paying interest on the full amount from day one, you can draw down the revolving credit as invoices come in.

#3 – Spare cash

Money set aside for emergencies, holidays or other savings can sit in your revolving credit until you need it. That keeps the money accessible while reducing the interest charged on your mortgage.

If you’re thinking about using a revolving credit, you might also like to consider an offset account.

Offset accounts are similar to a revolving credit (I like to think of them as cousins).

They both reduce the amount of mortgage interest you pay, but they do it in different ways:

With a revolving credit you typically have one account; it’s one big overdraft.

With an offset account your mortgage stays in one account, and your savings sit in separate everyday accounts.

The bank then “offsets” those savings against your mortgage balance.

I once spoke to an investor who really liked to bucket their money. They had to have:

They didn’t want to put all of this money together and dump it into a revolving credit account.

Instead, they used an offset set-up so they could keep their money buckets separate, but they could still use that money to save on mortgage interest.

For example, if you have a $30,000 offset loan and $20,000 sitting in linked accounts, you only pay interest on the $10,000 difference.

| Revolving credit | Offset | |

| How many accounts | 1 | 2 |

| How it works | Your mortgage works like a big overdraft. Money goes in and out of one account. | Your mortgage sits in one account, while your savings sit in separate linked accounts. |

| Best for | People who are disciplined with money and live by a budget. | People who like to bucket money into separate accounts. |

| Commonly used for | Personal mortgages | Investment mortgages |

| Main risk | Easy to spend the money again. | You may still need to make repayments, even when fully offset. |

ANZ, ASB, BNZ, Kiwibank and Westpac all offer revolving-style products, but offset accounts are mainly offered by BNZ, Kiwibank and Westpac.

So almost all banks have revolving credits, but not all banks have offsets.

They also all call their revolving credits and offsets different names:

| Bank | Revolving credit | Offset account |

| ANZ | Yes: Flexible Home Loan | No |

| ASB | Yes: Orbit | No |

| BNZ | Yes: Rapid Repay | Yes: TotalMoney |

| Kiwibank | Yes: Revolving | Yes: Offset home loan |

| Westpac | Yes: Choices Everyday | Yes: Offset available |

Peter Norris, Managing Director at Opes Mortgages (BNZ Mortgage Adviser of the Year 2018, $1.2 billion-plus in lending facilitated), says:

“A revolving credit only works if you don’t spend the money you’ve saved.

“The flexibility that makes it useful and gives you easy access to your funds … is also its biggest risk.

“The money you’ve diligently saved isn’t locked away. It’s sitting there, easy to dip into for a holiday or a new TV.

“Some advisers only half-jokingly call them ‘revolting credits’ because they often don’t work as well in real life as they do on paper.

“If you know you’d struggle to leave the money alone, you’re better off simply increasing your minimum mortgage repayments.

“Once that money is paid down, there’s no easy way to pull it back out and spend it.

A revolving credit suits disciplined budgeters. If that’s not you, choose a structure that removes the temptation.

A revolving credit may suit you if you:

It may not be the right fit if you:

Mortgage broker for over 10 years, property investor and Managing Director at Opes Mortgages

Peter Norris, a certified mortgage adviser with 10+ years of experience, serves as the Managing Director at Opes Mortgages. Having facilitated over $1.2 billion in lending for 2000+ clients, Peter is a respected authority in property financing. He's a frequent writer for Informed Investor Magazine and Property Investor Magazine, while also being recognized as BNZ Mortgage Adviser of the Year in 2018 and listed among NZ Adviser's top advisers in 2022, showcasing his expertise.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser