Property Types

Townhouses vs houses vs apartments – What goes up in value faster?

Want to know what sort of properties you should invest in? See the data about which grows in value faster – houses, townhouses or apartments.

Property Types

5 min read

Author: Scott Collings

Qualified builder. 6 years’ experience building + 6 years project managing residential developments.

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

A 2-bedroom townhouse can be a good investment for first-time NZ investors. They are often affordable and popular with tenants.

They’re also one of the most common types of investment property being built and sold, so there is usually plenty of choice.

But, that can also worry investors. Maybe there are now too many of them.

In this article, you’ll learn the pros and cons of 2-bedroom townhouses. That way you can decide for yourself if they are a good fit for you.

A 2-bedroom townhouse can be a great first investment property. Just don't buy based on price alone — location, tenant demand, and build quality matter too.

A 2-bedroom townhouse usually costs somewhere between $550,000 and $800,000. This is based on Opes Property’s current stock list, as at 1st June 2026.

But it depends on where you buy and what comes with the property.

| City | Property type | Typical price |

| Auckland | 2-bed townhouse | $600,000 - $800,000 |

| Christchurch | 2-bed townhouse | $550,000 - $700,000 |

Take Christchurch as an example.

Most 2-bedroom townhouses we see tend to sell for between $550,000 and $700,000.

In suburbs such as Spreydon and Riccarton, prices generally sit at the upper end of that range.

But how the house is built matters too.

For example, one development we recently recommended to investors had a median sale price of $551,650. These were entry-level properties. They had 2 bedrooms and a carpark.

However, another development had homes that cost around $659,000. The higher price came because the properties were built to a higher spec and included garages.

Many property investors assume that townhouses don’t appreciate in value as fast as a standalone property. But this isn’t necessarily true.

Historically, townhouses and standalone houses in New Zealand have increased in value at a very similar rate.

Yes, there is a slight difference in favour of houses, but there’s very little in it.

On average, Auckland houses beat townhouses by about 0.7% per year in this example. That’s based on REINZ data from January 1992 – February 2026.

While there is a difference, you can often buy a townhouse in a more central area than a standalone house because the cost is substantially lower.

Similarly, there’s nothing to suggest that a 2-bedroom property is going to go up in value slower than a 3-bedroom or 4-bedroom townhouse.

In Auckland, the price of 2 bedroom townhouses went up faster than townhouses with 3 and 4 bedrooms. This is based on REINZ data between 2010 and 2025.

That doesn’t mean you should rush out and buy a 2-bed as opposed to a 3-bed. But intuitively, you might have thought it was the other way around.

According to Stats NZ, townhouses, flats, and units made up 43.8% of all new homes consented in New Zealand in the year ended January 2026.

This demand is likely supported by wider changes we see across the country.

| Why demand is increasing | What it means |

| People are settling down later | More people are single for longer and don’t need a large home |

| More people are living alone | Smaller properties become more practical |

| Houses are more expensive | More affordable properties need to be built |

| Families are getting smaller | Fewer people need 3- or 4-bedroom homes |

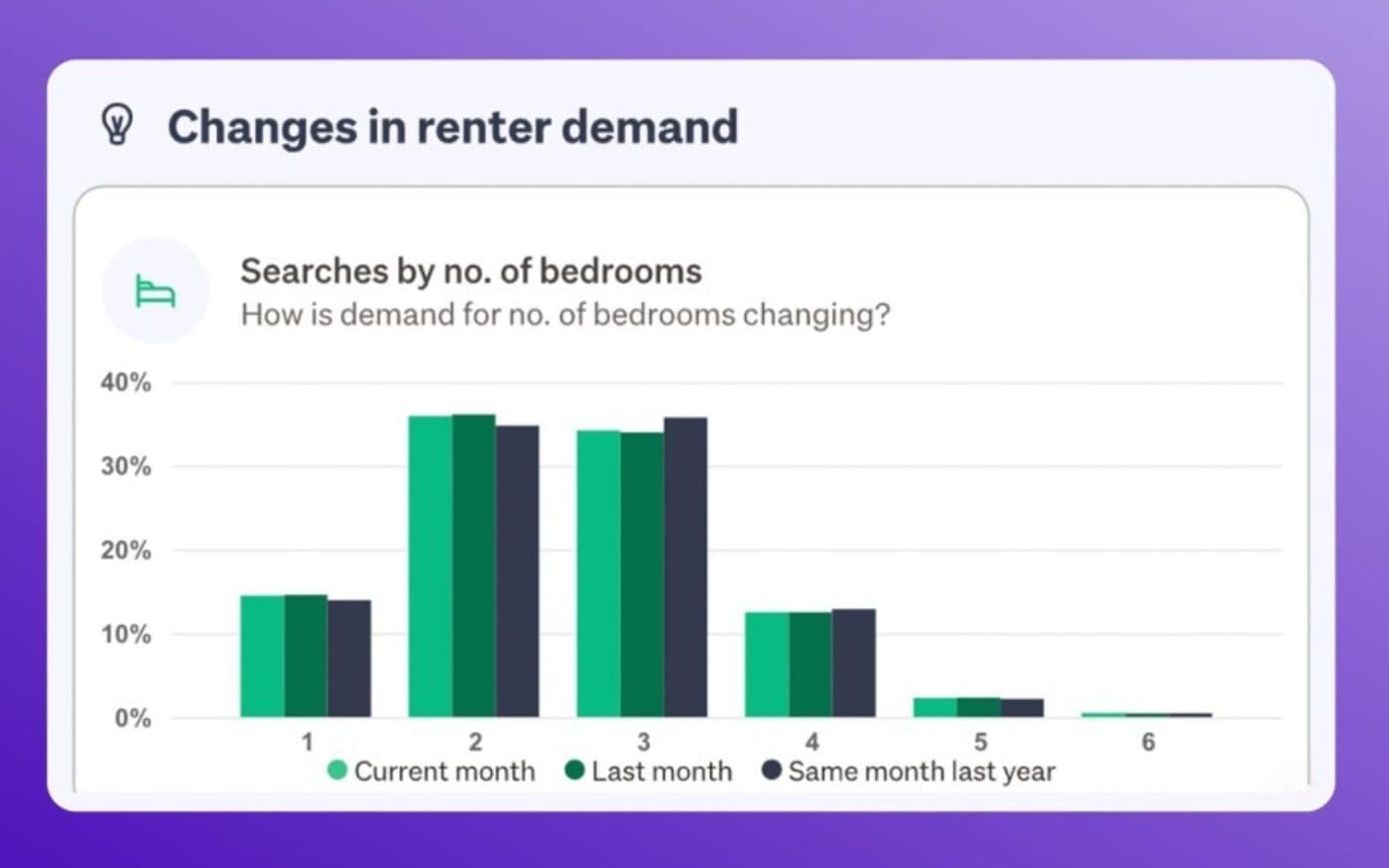

If you look at TradeMe’s data, you can see that 2-bedroom properties were the most popular searches among tenants in May 2026.

Townhouse living is only popular in larger cities. This is where populations are large, land is scarce, and people are used to living closer to their neighbours. Houses are expensive, so locals look for more affordable properties.

Take a look at this map of New Zealand. It shows the percentage of new dwelling consents that were townhouses in each council area for the 12 months to February 2026.

56% of new dwellings consented in Christchurch City were townhouses. But, only 2% of new dwellings consented in Ashburton District were townhouses. This is according to Stats NZ.

So, while a townhouse in a major city might be acceptable to tenants, if you are investing in a rural area townhouses may not be accepted as the norm.

A 2-bedroom townhouse can be a good fit for investors who are just getting started and who want an affordable way to build their portfolio.

Rather than putting all their money into one expensive property, they may be able to buy multiple lower-cost properties.

That said, townhouses only work in certain locations. They aren't often suited to investors targeting smaller towns or rural areas.

And if you’re a renovations-focussed investor, townhouses may not be for you. While you can renovate the interior, it’s harder to change the exterior of the property.

| Pros | Cons |

| Affordable | Concerns about over-supply |

| Strong fit for main centres | Less suitable for smaller towns and rural areas |

| Popular with tenants | Harder to renovate |

At Opes Partners, we have reviewed thousands of investment properties over the last decade. Through that we’ve learned that a 2-bedroom townhouse can be a good investment. But they’re not the right fit for everyone.

They can be a practical way to get into the market because they’re more affordable, while appealing to a range of tenants.

But that does not mean every 2-bedroom townhouse is a good investment. Location matters, and so does the quality of the development.

Qualified builder. 6 years’ experience building + 6 years project managing residential developments.

Scott has a background in construction. He progressed from a qualified builder to roles in project, construction, and finally development management. He brings this experience to his role as Opes' Property Development Liaison Manager, making sure investors can access high-quality properties.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser