Property Investment

Which property investment strategy should I use?

Thinking about investing in property? You're probably wondering if you should buy and hold or buy and flip. This article will help you make the right decision.

Property Investment

73 min read

Author: Andrew Nicol

Founder, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

If you want to learn how to invest in property in New Zealand, you’re in the right place.

This guide is a free, step-by-step resource that walks you through the full property investment journey. That’s from choosing a strategy to buying your first (or next) investment.

It’s also a living guide. We update it regularly and keep improving it over time, including:

Think of this as your reference guide. If you get stuck or have a question later, you can come back here anytime.

Have a question or comment? Leave it in comments at the bottom of the page — we read them and use them to improve the guide.

If you ignore all the noise, most residential investors use one of two strategies:

Your strategy matters because it determines what you buy, how you fund it, and how hands-on you need to be.

| Strategy | Buy and Hold | Buy and Flip |

| What you do | Buy a property Rent it out Hold on to it for the long term | Buy a property Renovate Sell it quickly for a profit |

| How you make money | The house rising in value (capital growth) & cashflow (sometimes). | Increase in value after you renovate. |

| Time commitment | Low – medium. | High. |

| Works for | Busy people, long-term wealth builders. | Hands-on investors who already know how to renovate. |

Neither strategy is better than the other. Both will help you achieve your property investment goals over the long term.

The question is: which is the right strategy for you? Let’s dive into them both a little more.

If you want something that fits around a normal job and family life, buy and hold usually wins. If you want a project and know how to renovate, then the buy and flips could be for you.

The ‘Buy and Hold’ strategy is the most common approach used by property investors in New Zealand.

Here’s why:

Put simply, this strategy makes investment accessible and realistic for everyday Kiwis who have kids, jobs and busy lives.

The ‘Buy and Hold’ is a strategy that is achievable alongside your main job. ‘Buy and Flip’ is like taking on an extra job.

There are usually 3 key steps in the Buy and Hold property investment strategy:

Rule of thumb: A buy-and-hold property should be boring in a good way. You don’t want major surprises, like an imminent roof replacement or a failing hot water cylinder.

Here are the pros and cons of the Buy and Hold strategy.

| Pros | Cons |

Less time consuming. Costs less to get started. You don’t need money for renovations. Lower risk. You’re not relying on selling quickly. | Takes longer to build equity. You don’t get the money until years in the future. |

Pro #1 – It’s the least time-consuming

Buy and Hold is close to a “set and forget” strategy.

If you buy a property that’s ready to rent (often a New Build) you can get started without doing any work.

Even if you renovate, the busy part is usually short ... then it becomes hands-off again.

How? Most investors pay a property manager to handle tenants and day-to-day issues.

Pro #2 – It’s often the most accessible

Buy and Hold is usually easier to start because you often need:

For example, many investors choosing this strategy will buy a New Build. The deposit on a New Build is 20%, compared with 30% on an existing property.

On a $600,000 property, that’s:

Flipping can also require extra cash for renovations.

Pro #3 – It’s often lower risk

Property prices move in cycles, and time can smooth out mistakes.

Buy and Hold is often lower risk because:

Flipping can still work ... it’s just less forgiving if costs blow out or the market shifts mid-project (more on this in the next section).

Con #1 – It takes longer to build equity

Many Buy and Hold property investors make the bulk of their money through the property going up in value.

While this can build a substantial amount of wealth in the long term, it takes a lot longer than what might look like a quick 3-month flip.

Con #2 – You don’t get paid immediately

You might renovate and see the property value jump by $50,000. Sure, you feel like a genius ... but that profit is often locked inside the property until you refinance or sell.

With flipping, you sell and can access cash straight away (after costs and tax considerations).

Here are my top tips to success with the Buy and Hold strategy:

#1 – Buy for long-term capital growth

Choose the right location and property type. You’re looking for an area with strong housing demand, which could lead to higher house prices.

#2 – Make sure you can hold for 10+ years

The Buy and Hold strategy works best if you can afford to keep it through the ups and downs, often for 10 years+. If you need to sell within 3 years it’s more likely the house value could have dropped.

Flipping is one of the property investment strategies Kiwis often think about first.

That’s usually because it’s the most visible. We watch TV shows like The Block, where contestants have dramatic before-and-after transformations.

But as good as the Flipping strategy looks from the comfort of our couches, we must respect and understand what it requires to be successful.

Buy and Hold can fit around your job. Buy and flip can become your job.

There are usually 5 key steps in the Flipping property investment strategy:

Here are the pros and cons of the Flipping strategy.

| Pros | Cons |

Creates equity immediately. You get the money (almost) straight away. Personal satisfaction from doing up an old house. | You only get paid once (it’s one and done). Projects can go over budget. Renovations can cost more than you expect. It’s easy to make expensive mistakes. Time intensive (requires a lot of effort). Need to invest in areas near you. |

Pro #1 – You can create equity quickly

A ‘Flipping’ strategy is one of the quickest ways to create immediate capital gain (equity).

That’s because once you finish the renovation the property should be worth more than the cost of the house and the renovations (if done correctly).

One rule of thumb many Flippers use is that if they spend $1 on renovations, the value of the house should go up by at least $2.

So, if you buy a house for $500,000 and spend $50,000 on the renovation. Most Flippers would want the house to rise in value by at least $100,000 (twice the renovation cost). That means they’d aim to sell the house for at least $600,000.

Pro #2 – You get the money (almost) straight away

Once you sell the property you get your rewards in cold, hard cash (after selling costs and tax). You can go out and spend that on whatever you want.

A Buy-and-Hold investor’s gains are “locked” into the property equity. Not as much fun, and not as easily accessed.

Pro #3 – You get the satisfaction of completing the project

There’s a real emotional payoff in transforming a tired property. Just remember that TV producers will sometimes edit out the stress, delays and cost overruns.

Con #1 – It’s “one and done”

Once you sell a property, the deal is over. You don’t get any ongoing benefits of the rent coming in or the property growing in value over time. Whereas Buy and Hold investors continue to earn a return from their properties.

Con #2 – Renovations often cost more than you expect

Many projects run over budget. One surprise can wipe out your profit. For instance, what happens if your builder pulls down a wall and realises there’s an electrical issue and the house needs rewiring? That could cost tens of thousands of dollars.

That could turn a profitable project into a loss-maker.

Con #3 – It’s easy to make expensive mistakes

If you’re not experienced, it’s easy to:

This is called over-capitalising; when you pay for upgrades that buyers don’t pay extra for.

Con #4 – It takes a lot of time (and it’s stressful)

Flips usually only make sense if you do a chunk of the work yourself. That means nights, weekends, decision fatigue, and a project hanging over your household.

Con #5 – It’s hard to do if the property isn’t near you

If you’re hands-on you generally need to buy close to where you live. It’s much harder (and more expensive) to manage a renovation from another city.

Here are my top tips to success with the Flipping strategy:

#1 – Find a property you can add value to with your skills

Make sure you find a property that you have the skills (or ability) and budget to improve. And focus on areas that tend to increase the property’s value. Things like repainting the interior walls of a house often make a bigger difference than painting the outside.

#2 – Have a list of “must dos” vs “nice to haves”

Don’t overcapitalise on all the fancy trimmings … this is an investment property and you want to get the most bang for your buck. Focus on improvements that buyers reliably pay for. Avoid bespoke or over-personal finishes.

#3 – Be conservative with your numbers

If the deal doesn’t work on paper with conservative assumptions, it probably won’t work in real life.

Buy and Hold: You buy a property, rent it out, and keep it long term while it grows in value over time.

Buy and Flip: You buy a property that needs work, improve it (repairs, upgrades, renovation), then sell it soon after. The “flip” is the sale.

Key differences:

1. How investors make money

| Buy and Hold | Buy and Flip |

| Your gains usually build up slowly as the house goes up in value (plus rent over time). | You get paid after you renovate and then sell the property (after costs and tax). |

2. What investors tend to buy

| Buy and Hold | Buy and Flip |

| A property that’s easy to own long term (low-surprise maintenance, strong rental demand). | A property that needs love with value-add potential. A property you can improve cost-effectively. |

3. Your role

| Buy and Hold | Buy and Flip |

| Set up the property and then manage lightly (often with a property manager). | You’re running a project – planning the work, managing trades, timelines and the budget. |

Still undecided? This 30-second checklist will point you in the right direction.

Buy and Hold might work for you if you …

Buy and Flip is more likely a fit if you …

Before you invest in property you need to answer one practical question: Where will your deposit come from?

For most New Zealand investors the answer is either:

While there are other strategies, these are the ones most people use. But to understand how much deposit you need you first need to know about the Loan-to-Value Ratio restrictions.

Most investors don’t “save” their first investment deposit. They borrow it against their home

The Reserve Bank’s LVR rules state how much deposit most investors need.

Remember, a Loan-to-Value Ratio compares the size of a loan to the value of a property.

So, if a bank lends you 80% of a property’s value, you must provide the remaining 20% as a deposit.

At the time of writing, the LVRs are:

| Property type | Maximum loan | Minimum deposit |

| Owner-occupied home | 80% | 20% |

| Existing investment property | 70% | 30% |

| New Build investment property | 80% | 20% |

Let’s say you’re looking at a $600,000 property.

Now let’s flip the question around. Instead of asking, “How much is the property?” ask, “How much deposit do I have?”

If you have $100,000 deposit:

| Investment property type | Deposit required | Maximum purchase price |

| Existing property | 30% | $333k |

| New Build | 20% | $500k |

Two identical properties. Two very different deposits. That single rule can be the difference between waiting years and investing now.

But remember, these rules change.

Since this guide was originally written in 2019 the LVR restrictions have moved from 70%, to not existing, then back to 70%, then again to 60%, to 65% and now back to 70% where they sit today.

And they have moved at least 8 times since they were first introduced.

Around 9% of Kiwi adults own an investment property. From my experience most of them don’t have $100,000+ in cash lying around to invest in property.

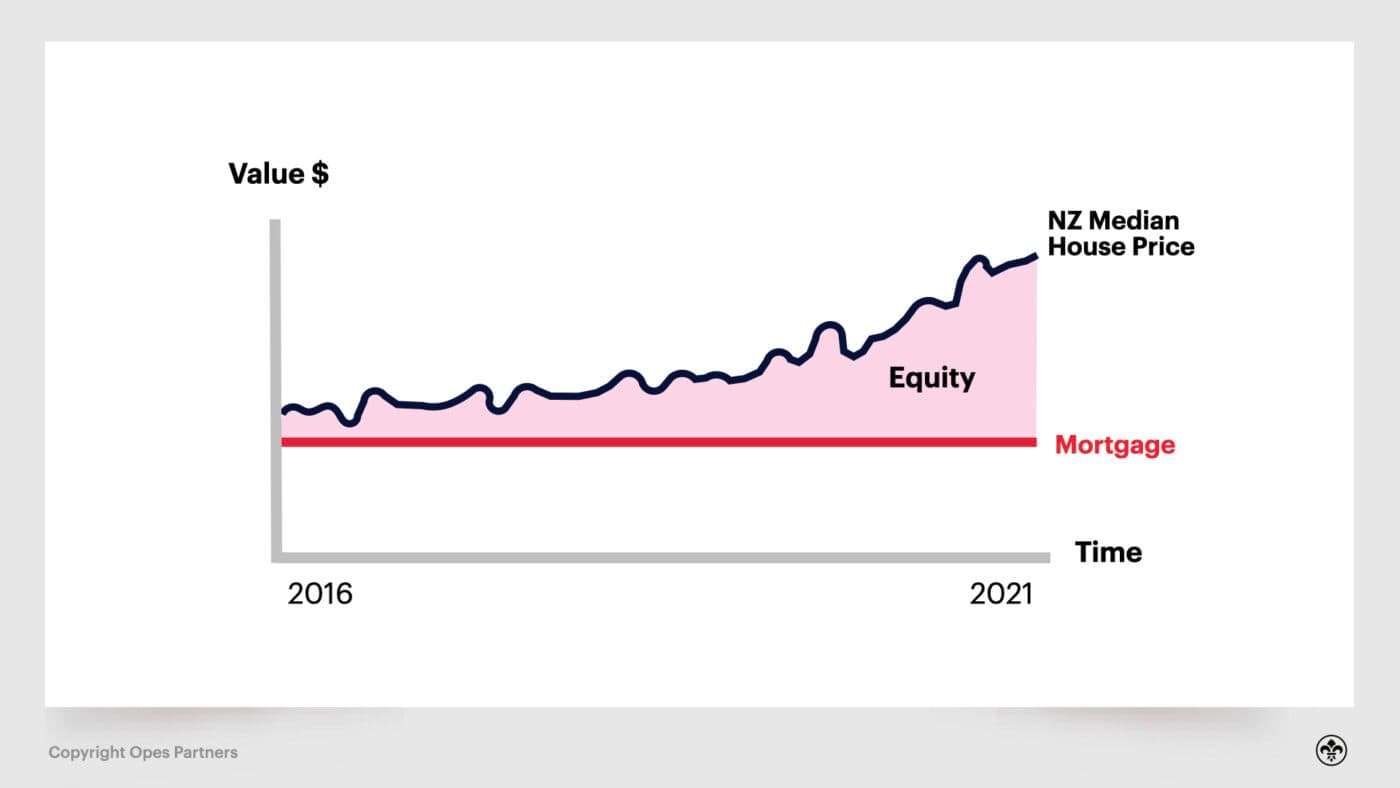

In reality, most investors don’t save their way into multiple properties. Instead, they use the wealth locked away in their home. That’s called equity.

Equity is the difference between what a property is worth and how much debt is secured against it.

As property values rise and you pay off your mortgage, your equity grows.

Here’s how to release that equity to buy an investment property.

Equity grows in two ways:

Here’s a simple example.

Imagine you bought a home in January 2016 for $600,000 and used a 20% deposit.

Over the next few years, two things usually happen:

By 2026, the numbers might look like this:

| Property value | $950,000 |

| Mortgage | $396,000 |

| Equity | $554,000 |

So, your original $120,000 deposit didn’t just sit there … it grew to $488,000 in equity.

Now, just because you have equity doesn’t mean you can borrow all of it.

Banks will generally lend owner-occupiers up to 80% of the property’s current value.

So in this example:

| 80% of $950,000 | $760,000 |

| Existing mortgage | $396,000 |

| Potential additional lending | $364,000 |

That’s $364,000 is what’s called your usable equity. That’s how much you could potentially use as the deposit for an investment property although, of course, you still have to meet the bank’s income and lending criteria.

If you have $364,000 of usable equity, then you could potentially spend:

| Property type | Deposit % | Max purchase price |

| Existing investment | 30% | $1,213,333 |

| New Build investment | 20% | $1,820,000 |

And no, that doesn’t mean you should buy a $1.8 million property. And it doesn’t mean the bank will definitely let you borrow the money.

In practice, most investors spread this across multiple properties (perhaps one in Auckland and one in Christchurch) rather than concentrating everything in a single asset.

But the key point isn’t how much you must spend, it’s the possibility that equity creates.

If you want to figure this out quickly, you can use the equity and leverage calculator on our website

Otherwise, here’s how to do the math in your head or on your phone

| For existing properties | Deposit / 0.3 |

| For New Builds/owner occupiers | Deposit / 0.2 |

If you don’t have enough savings and you don’t own property yet … it can feel like the door to investing is closed.

It’s not, but it does mean you’ll need to think differently.

There are two common ways people bridge the gap:

If you don’t own property yet, you can lean on your parents’ equity.

In simple terms this option works exactly the same way as using your own equity … except you’re just using someone else’s.

Your parents have likely owned their home for many years and it’s grown in value. That growth may have created usable equity.

This isn’t usually a gift. Families using this option typically draw up a clear repayment agreement to protect both sides.

Remember the Loan-to-Value Ratio (LVR) rules:

Banks are allowed to do some lending outside these limits.

That means you might still be able to get a loan, even if you don’t quite meet the standard deposit requirement. You’ll simply be classified as a high LVR borrower.

For example, some first home buyers have got on the ladder using a 10% deposit; some investors purchase with less than 30%.

But there is a trade-off. Lower deposits usually mean higher interest rates and stricter lending conditions. They also mean less buffer if property values fall.

If you want to choose this option, the best advice is to talk to a mortgage adviser.

Many people assume: “I need to save another $150,000 before I can invest.”

Often, that’s not true.

The real question becomes: “How much usable equity do I already have?”

So, you have chosen a property investing strategy and have an idea of how much you can afford to invest. Now, it’s time to decide where to look for an investment property.

This chapter will focus on the Buy-and-Hold investment strategy for finding and analysing properties, as this is the more common strategy. If you’re a Buy-and-Flip investor, the way you look for properties will be different.

Property investors are, effectively, going into business for themselves - a business that provides rental accommodation.

Now, the reason residential property is an attractive asset is because you can earn money in two different ways because you are operating in two separate markets.

Simultaneously you can achieve:

Because your property investing business will operate in these two separate markets, you need to ensure the property you choose (your product) can work in both.

For this your property needs to achieve:

Both of these are market-led. This means you need to start, not by looking at a specific property, but finding the market you want to operate in.

Since each region’s property market operates somewhat independently, you need to choose a city.

If you choose to live and work in one city, you usually can’t live in a property in another city.

For instance, if you want to live in Auckland because you've got a job, or want to be close to your kids, you're going to buy or rent in Auckland – maybe Hamilton at a stretch. But there’s no way to practically live in Christchurch.

In economic terms, properties in different cities are not good substitutes for one another. A house in Gisborne is not a good substitute for a house in Auckland, especially if you’re someone who wants to live in Auckland.

So, the property market is very closely tied to the long-term prospects of a city. Do people want to live there? Do people want to move there? Is the population increasing or decreasing? Are enough houses being built to keep up with demand, or is there a supply shortage forming?

This is why before choosing a property to invest in, you must decide which region or city you want to target.

When it comes to capital growth, it’s often more important to pick the right city, rather than the right property.

Let’s take another example to illustrate this.

Say you find a great property. It’s well-built, has 3 bedrooms, 1 bathroom and a large section, and it only costs $221,250.

The question now is: Should you invest? The answer: It depends … where is it?

If that property is in a tiny town like Patea (in South Taranaki) where the average house is worth only $221,250 – then the answer is likely to be “no”.

This is because you’re not likely to achieve stable increases in the value of your property over the long term.

Patea as a town has:

This isn’t to disparage or put down Patea as a place to live. It’s a great little town and Ed – one of this guide’s authors – grew up playing squash at the local club. However, it doesn’t have the fundamental factors most property investors are looking for.

Will property prices ever increase in a small town like this? Yes, there is likely to still be some growth but it will be driven by external factors. For example, low-interest rates and the bump the whole of New Zealand saw after the Covid-19 pandemic.

But, which would give you the greater confidence to invest:

The bottom line is you must find the right town or city to invest in first, before you start looking for the right property within that city.

So, how do you do that?

Below we outline the 6 factors to look for when choosing a city or town to buy an investment property in.

Note: All the data shared below is available free elsewhere on this website. So be sure to check out our property market pages to dig further into the data.

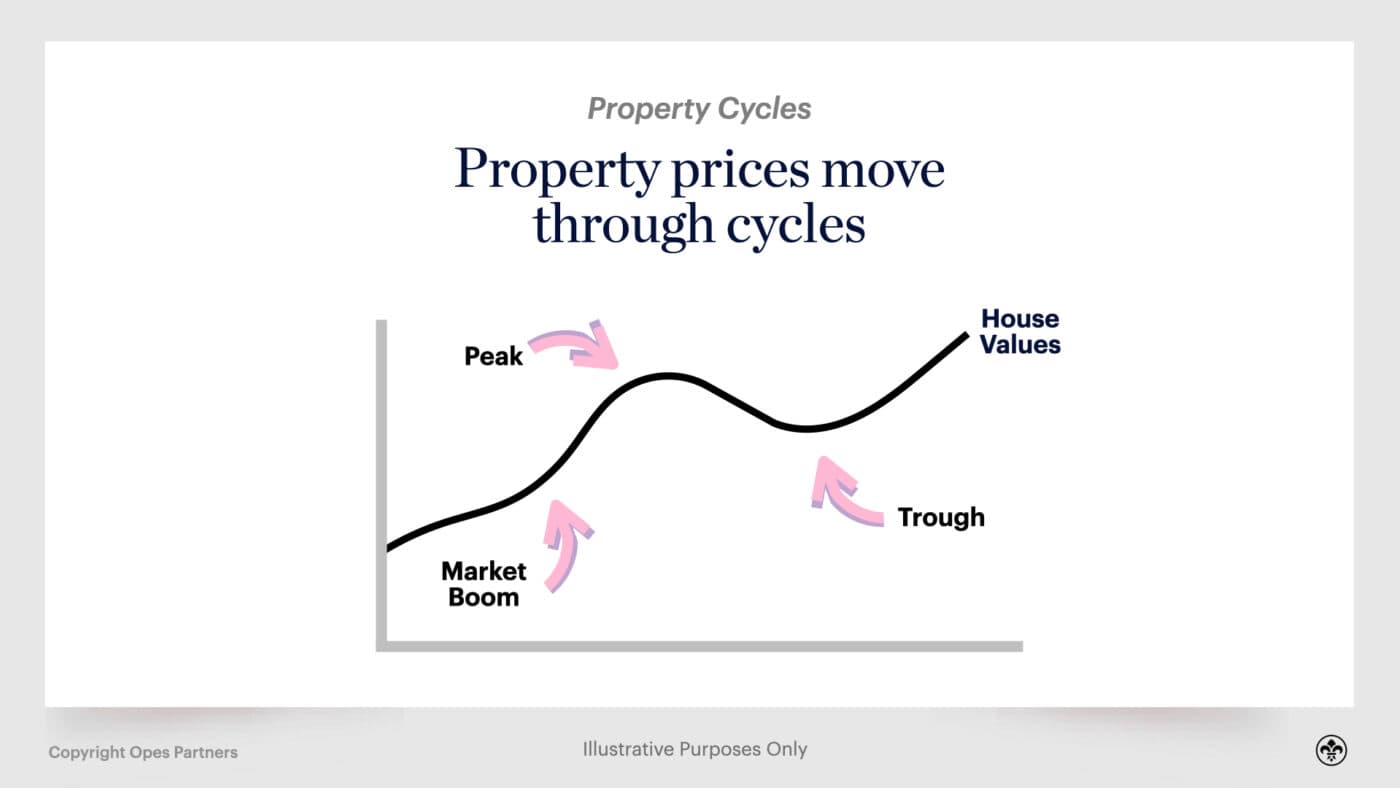

It’s often said all assets (including property) move through economic cycles. Sometimes prices are booming and there is confidence in property. Other times that confidence wanes and prices start to droop.

But, as we said above, because properties in each city aren’t good substitutes for one another, each region operates within its own property cycle. To say this in another way, property prices in Auckland might be going berserk, while those in Wellington are relatively flat. This happened between 2012 and 2016.

However, between 2016 and 2020, Wellington property prices increased quickly while Auckland remained stagnant.

So, it’s imperative we as property investors locate regions that are in an attractive part of their property cycle.

The way we do this is by asking:

Let’s go through an example to talk through the theory of those two points.

Over the last 30 years (1992 - 2022), Southland’s median house price has been 47% of the New Zealand median price.

So on average if the New Zealand median house price was $500,000, Southland’s would be $235,000.

But markets go through different cycles and sometimes a region’s property prices will be above that average. For instance, right now Southland’s median house price is 50.8% of New Zealand’s median price.

So house prices are 7.19% above their long-term average in this model.

Does this mean Southland’s property prices will crash? No.

Does this mean house prices in the region might not increase in the future? No.

But, it means there may be better opportunities in other parts of the country to find a good investment property if we are looking for healthy medium-term capital growth.

So you may wonder, where are the most undervalued and overvalued regions in New Zealand right now?

Here’s a list of NZ’s 15 most populous regions with where they sit under this model:

If you’re looking for the most up-to-date data, you can find it in the property markets’ section of this website. Here’s a list of the regions we cover:

It’s all very well finding an undervalued region, but some parts of that region may be more undervalued than others.

Let’s not forget, some of New Zealand’s regions are massive. The Waikato region, for instance, goes all the way from the top of the Coromandel Peninsula down to the bottom of Turangi in the Taupo District. That’s over a 4-hour drive.

So, we need to break the larger regions down into council areas to better target our search for investment properties.

For instance, here is the Canterbury region broken down into each council area. The map then shows where each council area is within its property cycle.

You can see the most undervalued region as at July 2022 was Waimakariri, which is 26.55% below its long-term average.

Whereas the MacKenzie District is 25.28% above its long-term average.

Both districts are in Canterbury, which is seen as undervalued by this model. However, right now, one district appears to be more attractive for property investment compared with the other.

The next step is to look closely at population projections.

When you eventually come to sell your investment property, you want to ensure it will have increased in price.

One indicator of this is population growth. More people = more demand for housing = higher house prices. You can see that trend in the data when we graph annual population growth with annual house price growth.

So, it is important to look at the projected population for the city you are analysing.

Take the Auckland property market over the 19 years between 2000 - 2019.

Between those years, the city’s population grew by 389,000 people – that's 25%, or the size of Christchurch. Over those 19 years property prices increased from $240,000 to $860,000 – which is 250%.

It took 19 years for Auckland to add the size of Christchurch to its population. But the same level of population growth (around 390,000) is expected to be added to the city over the next 9 years.

What is that going to do to the demand for housing? How will that impact house prices? What will higher numbers of people in the city do to rents?

Well, it’s likely to have a positive impact on property investors who already own property in the city.

By now you are probably also picking up population growth is often distributed around a region. What do we mean by that?

Well, over the next 25 years (2018 - 2043), Canterbury’s population is expected to grow by about 19%. But that doesn’t mean the population in every part of Canterbury is going to increase by that amount.

Take a look at the breakdown of population growth by council area.

Here you can see some areas are expected to see enormous population growth. Selwyn District’s population is projected to grow 60%+ over this period, while Kaikoura’s population is projected to shrink 4.36% over that time.

What’s the lesson here?

As well as looking for a good region to invest in, you also want to dig deeper to consider what’s happening in each council area.

The other side of having more people in the city is ensuring they have the income to support higher house prices.

You might have a large population base, but if houses are unaffordable to buyers then there won’t be much room for growth in property prices.

There are two factors to consider:

There are a couple of ways economists try to track economic strength. GDP, which is growth per person (per capita), is something you’ll often read about in the papers.

But what you really care about isn’t how much businesses are doing in a region. What you do really care about is the income real families are earning. This where you might consider average (mean) household income growth.

Let’s talk about the Bay of Plenty region, since they haven’t got a mention so far in this guide.

Over the 21 years between 1998 and 2019 (the years we have current data for) the average household income in Tauranga increased 4.14% per year.

Over that same time-frame, household incomes in the Kawerau District (a small district also in the Bay of Plenty) grew by only 2.99%. That’s the slowest in all of New Zealand.

So, if you were considering an investment property in the Bay of Plenty region, putting all other factors aside, which would you rather invest in? Which area is going to be able to support higher rents? Which area will have the income to support higher house prices? Which area is likely to be more prosperous in the future?

If you’re like most property investors, you’ll probably gravitate towards Tauranga in this instance.

There’s a joke in property investment circles, which is: “You can’t use capital gains to pay your mortgage”.

It’s true, even if your property is increasing in value, you still need to be able to pay the mortgage. You’ll really feel the pain if you purchase a property where the rental yield is so poor you have to pay tens of thousands of dollars a year to top up the bank account.

So, a big part of becoming a successful residential property investor is ensuring you can hold the property over the long-term so you can achieve capital gains over time.

This is why when analysing a target city, you should compare rents with house prices to ensure they meet your investment appetite.

For instance, Auckland currently has an average rent every week of $611 for three bedroom homes, according to Barfoot and Thompson (August 2021). But the average sale price for that type of property was $1,060,000. That is a 3.0% gross yield (accounting for no vacancy).

Whereas Rolleston has an average rent every week of around $490 for 3 bedroom homes, and the average sale price for 3-bed homes is $675,000. This is a 3.77% gross yield.

This means it is much more affordable to Buy-and-Hold in Rolleston over the long-term. Not only is there a cheaper entry price, but there is relatively more income achieved each week to pay for expenses. Some expenses, like interest payments to the bank, are often proportional to the price of the property bought.

But this doesn’t mean you shouldn’t buy in Auckland. It just means if you do invest in Auckland, you need to be aware it will require more investment to get the capital gains.

Although gross yield isn’t always the most useful calculation when looking at a particular property (as we will discuss below), it is still useful when analysing a city or suburb to invest in.

So, finally, you’ve found a good city with good fundamentals. Now you need to make sure you can actually afford to purchase there.

The affordability of housing changes drastically around the country, and even within a region.

For example, take a look at the Waikato region to see how affordability can vary.

The average property in the Waikato region sold for $711,000 in July 2021, according to REINZ.

But the average property value in the Thames-Coromandel District is $1,085,000 (the most expensive council area in the Waikato), and the average property in the Waitomo District is only $300,389, according to propertyvalue.co.nz.

So, property investors will find some areas very affordable, but other areas more expensive. It’s important to keep this in mind as you’re searching for rental properties.

On your quest to look for high-quality investment properties, it’s important to note: Not every city or region is going to tick every box on this list.

After looking at the data, you’ll need to make a judgement call about where you believe is the best place for you to invest. That will be different for each individual.

For instance, if you have lots of money to invest, you might choose to purchase in Auckland. Property prices there are high and yields relatively low. But it’s got high population growth, good incomes and abundant industry.

If your affordability is low, on the other hand, you might only be able to purchase in a region where both prices, income and population growth are lower.

But, armed with these tools, you should be able to analyse a region and then make an informed decision.

If you would like extra credit, your next step might be to start digging into suburb level data, which means identifying specific areas where you want to look for investment properties.

That’s where you might look at a pair of maps, like the ones below, to identify suburbs that have had high capital growth in the past, and also relatively high yields.

For instance, here is a map of Auckland showing the suburbs that have achieved the highest capital growth between January 2000 and today.

And here is a map showing the current gross yields broken down by suburb.

This suburb level data is broken down for each of the four main cities in New Zealand– Auckland suburbs by price, Wellington suburbs by price, Christchurch suburbs by price, and Hamilton suburbs by price.

Before you jump onto Trade Me to go shopping for an investment property, you need to know what you’re actually looking for.

Investment properties can look similar on the outside. But they can perform very differently.

A townhouse, a house, an apartment and a piece of land can all be “investment properties”.

But they usually suit different investors, budgets and strategies.

So in this step, we’ll break down properties in 3 ways:

| How to categorise properties | What it means |

| Property type | House, townhouse, apartment or land |

| Growth vs yield | Whether the property is more likely to grow in value or provide stronger rent |

| Age | New build vs existing property |

The first way to categorise investment properties is by type. This means asking: What kind of property are you actually buying?

| Standalone house | A house that is not attached to another property |

| Townhouse | An attached home, often part of a development |

| Apartment | A home inside a larger building |

| Land | An empty section with no house on it |

Each property type has different strengths, weaknesses and risks.

A standalone house is a home that is not attached to another property.

It usually sits on its own section and often has more land than other property types.

This is the classic Kiwi home.

| Pros | Cons |

| More ways to add value | More expensive to buy |

| Often easier to renovate | Often lower rental yields |

| Can be easier to sell | Less diversification if your money is tied up in one property |

| May have stronger capital growth | Can be more expensive to maintain |

Standalone homes are easier to renovate. You might be able to add bedrooms, build a sleepout, or renovate the bathroom and kitchen.

That makes them a better fit for investors using an active strategy, like renovating or adding value.

They can also be easier to sell, because many owner-occupiers prefer standalone houses. If more buyers want that type of property, you may have a larger resale market.

That said, standalone houses are usually more expensive and tend to have lower yields.

That doesn’t make them bad investments. It just means they are often more focused on long-term capital growth than short-term cashflow.

| Standalone houses may suit investors who | They may not suit investors who |

want to renovate or add value have a larger deposit want more control over the property are focused on long-term capital growth can afford weaker cashflow while they hold the property | need strong rental income have a smaller deposit want a hands-off investment want to buy multiple properties sooner |

Townhouses are usually attached homes.

They often share one or two walls with neighbouring properties and may be part of a larger development.

They commonly have:

Townhouses are common in New Zealand’s main cities and are often bought by investors.

| Pros | Cons |

More affordable than standalone houses Often available as New Builds Can have a good mix of growth and yield Often in central suburbs Popular with tenants and first-home buyers | Less land Less control over exterior changes May have Residents' Association fees Harder to renovate extensively Similar properties may compete for tenants |

Townhouses can be a good middle ground – cheaper than standalone houses. But they often grow in value faster than apartments.

They are also commonly built as new builds, which can make them more accessible for investors using a Buy and Hold strategy.

The downside is that you have less control owning a townhouse.

A Residents' Association (the group that manages shared areas and sets rules for the development) may tell you what you can and can’t do to the outside of your property.

There is often less land, so it’s harder to add value through landscaping, extensions or minor dwellings.

New townhouse developments can also create tenant competition if many similar properties are completed at the same time.

That’s why location and rental demand matter.

| Townhouses may suit investors who: | They may not suit investors who: |

want a passive Buy and Hold property want a new build have a moderate deposit want a balance between growth and yield don’t want to renovate | want to do major renovations need very high rental yield only want standalone houses don’t like residents’ association rules |

An apartment is a home inside a larger building.

You usually own the inside of your unit, while sharing common areas with other owners.

That can include lifts, lobbies, gyms and pools.

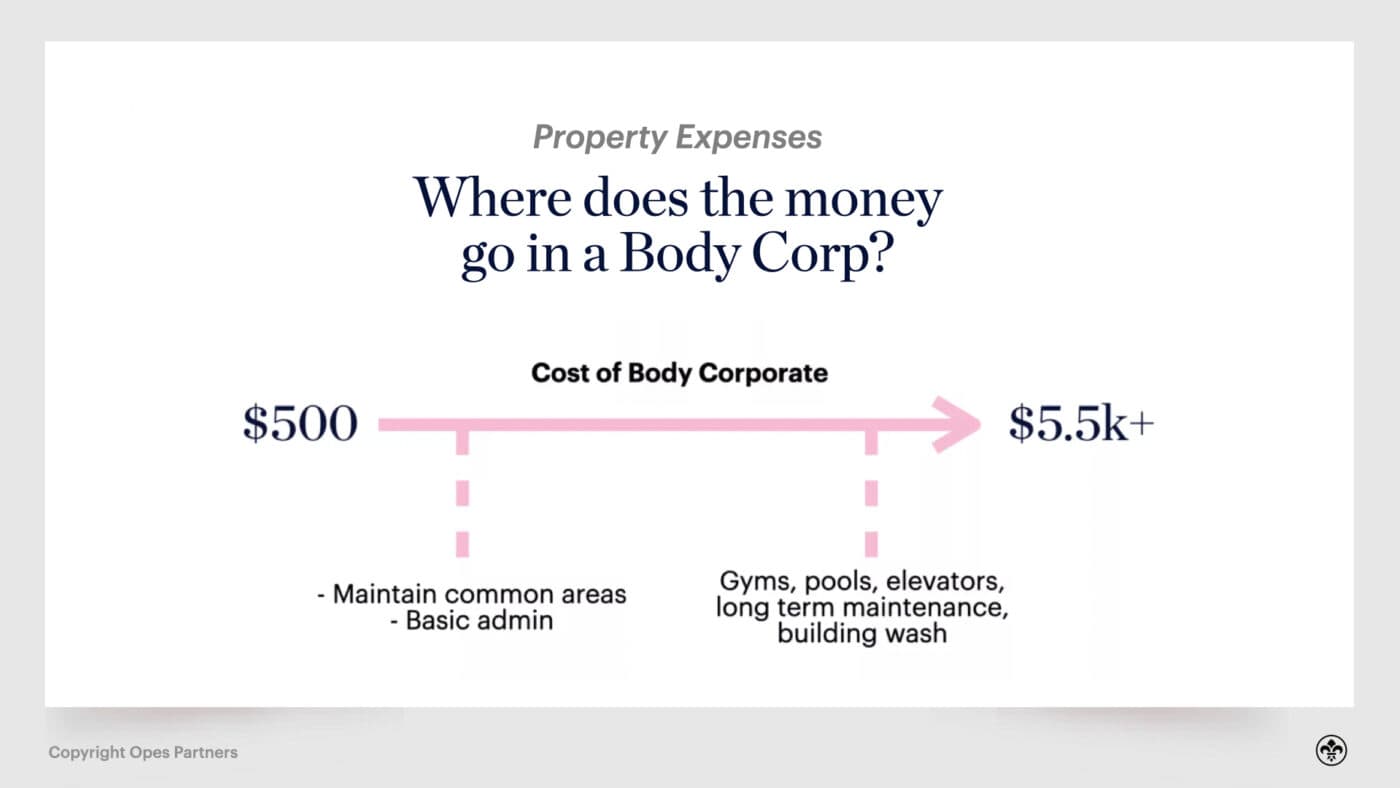

Most apartments have a body corporate. This is a group that manages the shared parts of the building and charges owners fees for maintenance and upkeep.

Common apartment types can be:

Dual-key apartment: Two separate rentable spaces under one legal title.

| Pros | Cons |

Lower purchase price Often higher rental yields Lower maintenance Often in central locations | Usually slower capital growth Body corporate fees Less control over the building Some banks may require a larger deposit Smaller resale market for some apartments |

Apartments can be more affordable. So, they may help some investors get into the market sooner.

They can also produce higher rental yields because the purchase price is lower, while rent can still be relatively strong.

That can make apartments attractive for investors who care more about income than long-term capital growth.

The downside is, that apartments have historically grown in value more slowly than houses and townhouses.

They can also have high body corporate fees, especially if the building has lifts, gyms, pools or other expensive shared services.

Some apartments can also be harder to finance. Banks may ask for a larger deposit if the apartment is small, unusual or has a limited buyer market.

| Apartments may suit investors who: | They may not suit investors who: |

have a smaller deposit want higher rental yield are close to retirement want more income from their portfolio want a low-maintenance property | want strong capital growth want to renovate or add value dislike body corporate fees want a large resale market |

Land banking means buying land and holding it for several years, hoping it becomes more valuable in the future.

Some investors buy land and hold it. Others buy land to develop.

| Pros | Cons |

Can grow in value quickly in a rising market No tenants to manage Little day-to-day maintenance | No rent while you hold it Can be risky if the market doesn't move Building requires more capital and risk |

The cool thing about buying land is it can increase in value quickly when developers want it or if it gets rezoned.

If house prices rise faster than building costs, developers may be willing to pay more for land because development becomes more profitable.

Land also gives you the option to build and add value.

The downside is that land usually has no income.

So, you still pay the mortgage, rates and other holding costs, but there is no tenant paying rent.

This can make land banking hard for everyday investors.

It can also be risky. If the land doesn’t increase in value quickly, you may be left paying costs for years without any cashflow.

| Land may suit investors who: | It may not suit investors who: |

have strong cashflow from other sources understand development can handle higher risk have enough capital to build later | need rental income have limited surplus income want a passive investment are buying their first investment property |

There is no "best" property type. The right property is the one that fits your strategy, budget and goals.

The next way to compare properties is by growth and yield.

Unfortunately, in most cases, there is a trade-off between growth and yield.

Higher-growth properties often have lower rental income, while higher-yield properties often grow in value more slowly.

Most properties lean one way or the other.

| Property type | Usually stronger at |

| Standalone house | Growth |

| Townhouse | Growth |

| Apartment | Yield |

| Dual-key / multi income property | Yield |

| Land | Growth |

Growth properties are usually bought because they are expected to increase in value.

They often appeal to owner-occupiers, which can help push up resale prices.

The trade-off is cashflow.

Growth properties often have lower rental yields, so you may need to contribute more money each week to hold them.

Yield properties are bought because they produce stronger rent.

These properties may produce better cashflow, but they often have a smaller market when you sell.

That’s because the next buyer is more likely to be another investor, not an owner-occupier.

| Factor | Growth property | Yield property |

| Main goal | Increase in value | Rental income |

| Typical buyer | Owner-occupier or investor | Mainly investor |

| Cashflow | Often weaker | Often stronger |

| Resale market | Usually broader | Often narrower |

| Best for | Long-term wealth building | Income or cashflow support |

Townhouses are a good option for passive buy-and-hold investors. They are very popular among the investors we work with here at Opes Partners.

In fact, 76% of the properties investors bought through us between January – June 2022 were townhouses.

So, let’s go through the benefits of townhouses and who they tend to be the right fit for.

We’ll also talk about the other side of this, which is the drawbacks of townhouses.

Capital growth builds wealth. Rental income helps you hold the property long enough to get it.

The final way to categorise properties is by age: Is it a New Build or are you buying an existing property?

In simple terms:

| Property age | What it means |

| New Build | Brand new property, usually bought from a developer |

| Existing property | A property that has already been lived in or owned before |

Both can be good investments, but they suit different strategies.

So, neither option is automatically better.

The better question is: “Which one suits your strategy?”

| Factor | New Build | Existing property |

| Best suited to | Buy and hold investors | Renovations-focused investors |

| Deposit | Often lower | Often higher |

| Maintenance | Lower | Higher |

| Ability to add value | Limited | Higher |

| Cashflow | More predictable | Can be better after renovation |

| Risk | Developer/build risk | Renovation/maintenance risk |

| Time required | Lower | Higher |

A New Build is a brand new property. This means you are usually the first owner.

You might buy it:

New builds are often townhouses, but they can also be standalone houses or apartments.

| Pros | Cons |

| Often lower deposit requirement | Limited ways to add value |

| Lower maintenance | May not be ready immediately |

| More predictable cashflow | Often weaker cashflow than a renovated existing property |

| Often attractive to tenants | You rely on the developer delivering the property |

New Builds are often easier for investors to buy.

You often only need a 20% deposit to buy a New Build, compared to a 30% deposit for an existing property. That’s according to the Reserve Bank’s LVR rules.

They can also have lower maintenance because everything is new. That means fewer unexpected costs, like replacing an old roof, hot water cylinder or major chattels.

New builds can also attract good tenants because they are warm, dry and modern.

The downside is, New Builds don’t usually give you many ways to add value.

The kitchen is already new. The landscaping is usually done.

That means you generally can’t manufacture quick equity through a renovation.

New Builds are usually a better fit for investors who want to buy and hold, not investors who want to actively renovate.

| New builds may suit investors who: | They may not suit investors who: |

want a passive investment have a smaller deposit want lower maintenance want more predictable cashflow don’t want to renovate | want to add value quickly want to renovate want the cheapest property on the market need immediate high cashflow |

Existing properties are homes that have already been owned or lived in.

Most properties listed on Trade Me or realestate.co.nz are existing properties.

| Pros | Cons |

More way to add value Can renovate to increase rent Available immediately Can suit active investors May create quick equity | Often need a higher deposit Higher maintenance Less predictable costs May have weaker cashflow before renovation Can take more time, skill and money |

Existing properties give you more opportunity to add value.

You might repaint, replace the carpet, renovate the bathroom or add bedrooms.

All these things can increase both the value of the property and the rent you can charge.

This is why existing properties often suit investors using renovation, flipping or BRRRR-style strategies.

The downside is that existing properties can cost more to maintain.

Older homes are more likely to need repairs. Chattels wear out. Roofs get older. Plumbing, wiring and insulation may need attention.

For investors, they also require a 30% deposit, compared to a 20% deposit for New Builds.

That makes them harder for some first-time investors to buy.

| Existing properties may suit investors who: | They may not suit investors who: |

want to renovate have extra cash for improvements want to manufacture equity are comfortable managing trades want stronger cashflow after renovation | want a passive investment have limited cash after settlement don’t want maintenance surprises don’t have time to manage renovations |

Once you know the type of property you want, you can start looking.

There are 3 main places to find investment properties.

| Where to look | Best for |

| Property websites | DIY investors looking for existing properties |

| Property investment companies | Investors who want new builds |

| Developers | Investors who want to buy a new build directly |

Many investors start with websites like:

These websites give you a wide range of properties. But that is also the problem.

There are a lot of listings, and most are not designed to be investment properties.

| Websites are usually a better fit if you: | They may be harder if you: |

want to buy an existing property are comfortable doing your own research know how to run the numbers want to renovate, flip or add value | want a new build want a done-for-you process don’t know how to analyse a property want someone to help you choose |

Rather than finding a property yourself, a property investment company helps you build a strategy and recommends properties that fit it.

This is what we do at Opes Partners.

For example, our financial advisers can help you understand your goals, help you build an investment strategy, and recommend properties that fit your plan.

They’ll also run the numbers for you and hold your hand throughout the buying process.

Some people will love this hands-on approach, others … not so much.

| They may be a good fit if you: | They may not be the right fit if you: |

want a hands-off investment want help choosing a property want a new build don’t want to renovate want advice before you buy | want to flip properties want to renovate want to buy in a very specific small town only want existing properties |

You can also buy a New Build directly from a developer.

This can work well if you already know where you want to invest and what type of property you're looking for.

The benefit being you go straight to the source.

The downside is that the developer has their own product to sell. So, they usually won’t compare their property with every other option in the market.

If you go direct to a developer, it is still worth getting independent financial advice before you buy.

| It may be a good fit if... | It may not be a good fit if... |

You already know what type of property you want You want a New Build You're comfortable analysing property deals yourself You have a specific development or developer in mind You understand the risks and numbers involved | You need help choosing a strategy You want someone to compare multiple options for you You want independent advice before deciding You want someone to negotiate or source properties on your behalf You're a first-time investor who isn't sure what to buy |

Once you find a property you like, don’t buy it just because it looks pretty.

Run the numbers first.

At minimum, you’ll want to understand:

| Number to check | Why it matters |

| Purchase price | What you are paying |

| Deposit required | How much money you need to buy it |

| Rent | How much income it produces |

| Gross yield | How rent compares with price |

| Mortgage costs | Your largest regular expense |

| Rates and insurance | Ongoing holding costs |

| Maintenance | Expected repairs and upkeep |

| Body Corporate and Residents' Association fees | Extra costs for apartments and townhouses |

| Tax | Whether you need to pay extra tax |

| Cashflow | How much you pay or receive each week |

If you’re working with a property adviser or accountant, they may do this for you.

If not, use a spreadsheet or calculator so you can compare properties properly. For instance, you might use Opes+, a free software that helps you analyse your property’s potential returns.

A property can look good online and still be a poor investment once you run the numbers.

By the end of Step 4, you should know what type of property suits your strategy.

Maybe it’s a standalone house, if you want to renovate and chase growth

It could be a townhouse if you want a more hands-off investment with less maintenance involved.

Either way, the order matters:

That way, you’re not just scrolling listings and hoping something stands out.

You’re shopping with a plan.

New Zealand has a culture of Do It Yourself (DIY), and we don’t always like to seek or pay for help.

We’d rather stumble, figure it out, and do it on our own.

Purchasing an investment property is one of the largest financial decisions you may make in your life.

You don’t want to mess this up or get it wrong.

Because that will cost you … a lot.

That’s why there are several advisors and professionals you should use when getting into investment property. This chapter will walk through all the advisors you might need, along with how they get paid and the benefits of using them.

Mortgage Brokers act as your representative to the banks.

They study the bank’s policies and rules and aim to understand which banks will lend to what types of people (and on what properties).

They’ll also negotiate with the banks to ensure you get the lending and the best interest rate possible.

Sure, you could go and use the bank's mortgage calculator and try to figure it out yourself.

However, if you don’t use a (good) mortgage broker, you may end up talking to banks who won’t lend to you. This might be because you don’t fit within the types of people or properties they like to lend on.

If you do this and get rejected by multiple banks, some other banks may also not lend to you. They’ll see you’ve been denied finance and think: “Well, maybe we won’t lend to them either”.

The end result is that by trying to do it themselves some investors aren’t able to secure finance for their investment property.

The other main cost is around how you set up your mortgages. Banks are “order takers” – they’ll give you what you ask for.

So, if you ask for a 30-year principal and interest mortgage for an investment property – and you’re approved – that’s what they’ll give you.

But, paying P+I on the investment mortgage may not be the right fit for you.

Let’s say you’ve got your own personal mortgage already. In this case having an interest-only loan on the investment often means paying less tax to the IRD – compared with paying P+I on both properties.

Good mortgage brokers will not just ask you which type of mortgage you want – they’ll ask what you want your portfolio to do for you. Then it’s a matter of finding the type of loans that will best suit your goals.

So, the cost of not using a mortgage broker could land you with loans:

Generally, mortgage brokers don’t cost you anything.

This is because brokers are typically paid by banks. The banks generally want your mortgage, so if the broker secures your lending, the bank pays the broker a commission.

Insurance Advisers are very similar to mortgage brokers as they act as your representative to insurance companies.

They learn about each company’s products and rules and can recommend the right product and level of cover for you.

If you don’t use a (good) insurance adviser, you may end up buying the wrong insurance.

Or worse, you may end up purchasing an insurance product that has prohibitive terms and conditions (i.e. fine print). This can make it hard for you to claim on that insurance when you need it.

It’s important to note, not all insurance policies are created equal. The quality of the policy, which is what you can claim on, is determined by the specific wording within the insurance agreement.

And because these policy documents are complicated, it takes someone dealing with them day-in day-out to really understand the differences.

An insurance adviser will also help when it comes to claim time, working with the insurance company to make sure your claim is paid out.

Like mortgage brokers, insurance advisers typically get paid a commission from the insurance company when they help you purchase the right type of cover for you.

This means they don’t cost you anything to use or to get advice from.

So, it’s more than worth it to have them on your side.

Your Solicitor will make sure you are sorted from a legal perspective.

They’ll look over:

It is highly risky not to use a solicitor.

You may end up investing in a property you don’t fully understand. For example, legally what happens if there is a shared driveway.

You may also accidentally agree to clauses which aren’t in your best interests.

For instance, let’s say you want to purchase a new-build. During negotiation you agree to a Sunset Clause that allows the developer to cancel the contract if the build takes too long.

Now, let’s say during the construction of the property, house prices go up and your property is now worth more. The developer may allow the build to drag on, which allows them to cancel your contract. Now, they can sell the property to another purchaser at a higher price.

This wouldn’t happen if your lawyer negotiated the Sunset Clause solely for the benefit of the purchaser (i.e. you), preventing the developer from cancelling your contract under this clause.

In another scenario, let’s say you want to buy a cross-lease property. It all looks good so you go unconditional (i.e. you commit to buying the property) without consulting a lawyer.

Just before settlement you later discover the conservatory at the back of the house isn’t on the ‘flats plan’. For a cross-lease property, this could mean the conservatory is illegal. So, the property has a defective title and the bank won’t lend you the money.

It’s 2 days from settlement (i.e. paying the money for the property), and the bank has withdrawn their offer of finance. This means getting hit with penalty interest.

This is an extreme – but not uncommon – example of what can happen if you’re not working with your lawyer.

A good property solicitor will check the flats plan and the LIM to make sure all the buildings on your property are legal. If they’re not, then you can use that information to negotiate a better price with the current owner.

Solicitors charge a direct fee for their services, so when buying a property you can expect to factor this in.

Different lawyers will charge different amounts, so it’s best to ask.

But we would usually budget for between $2,000 and $3,500 (including GST).

With the recent introduction of interest deductibility rules from the IRD, property accountants are more important than ever.

Not only will they file your tax returns with the government and IRD, ensuring the numbers behind your investment stack up … they’ll also make sure you are paying the correct amount of tax.

This is because many property investors pay more tax than they need to. This often happens when investors aren’t using companies or family trusts correctly, or they’re not claiming all of the taxable expenses they could.

Remember, succeeding in property investment is less about the property and more about the investment (numbers).

If you try and do your own property accounting you will need to:

Also, you may find you are owning your properties in the wrong entity.

Maybe you are holding them in your own name, when a trust would be more efficient.

For instance, let’s say you earn $200,000 a year – a big income. Your tax rate is 39%. If your property makes $10,000 in pre-tax profit – you then have to pay $3,900 in tax.

Now, let’s say you move that property into a trust. The tax rate falls to 33%, which means the amount of tax you have to pay for your property falls to $3,300. You’ve saved $600 per year because you moved your property into a different entity.

This is the sort of advice a good property accountant should give you.

Like solicitors, property accountants charge fees for their services so investors pay them directly.

While the fees charged by property accountants differ from firm to firm, it is safe to budget $1200 - $2000 (including GST) per year.

Property managers manage your investment on your behalf.

They will:

Every property investor should use a property manager.

If you don’t, you will have a lot more worries about your properties and tenants. You’ll spend a lot more time dealing with your investment properties, which causes stress and may make you limit the size of your property portfolio.

For instance, most property investors know they need to do regular property inspections, but fail to do so.

If you don’t inspect your property every 3 months you will have broken the terms of your insurance, and if something goes wrong you may not be able to make a claim.

Tenancy regulations are also becoming more complex and investors who accidentally break the rules can find themselves on the receiving end of a fine.

If you would like more evidence on why you need a property manager, join the Property Investors Chat Group NZ on Facebook. You will see the distress and worry investors have when they try to manage a property themselves, because they’re not fully across the detail of tenancy regulation. Just take a look at a few screenshots below.

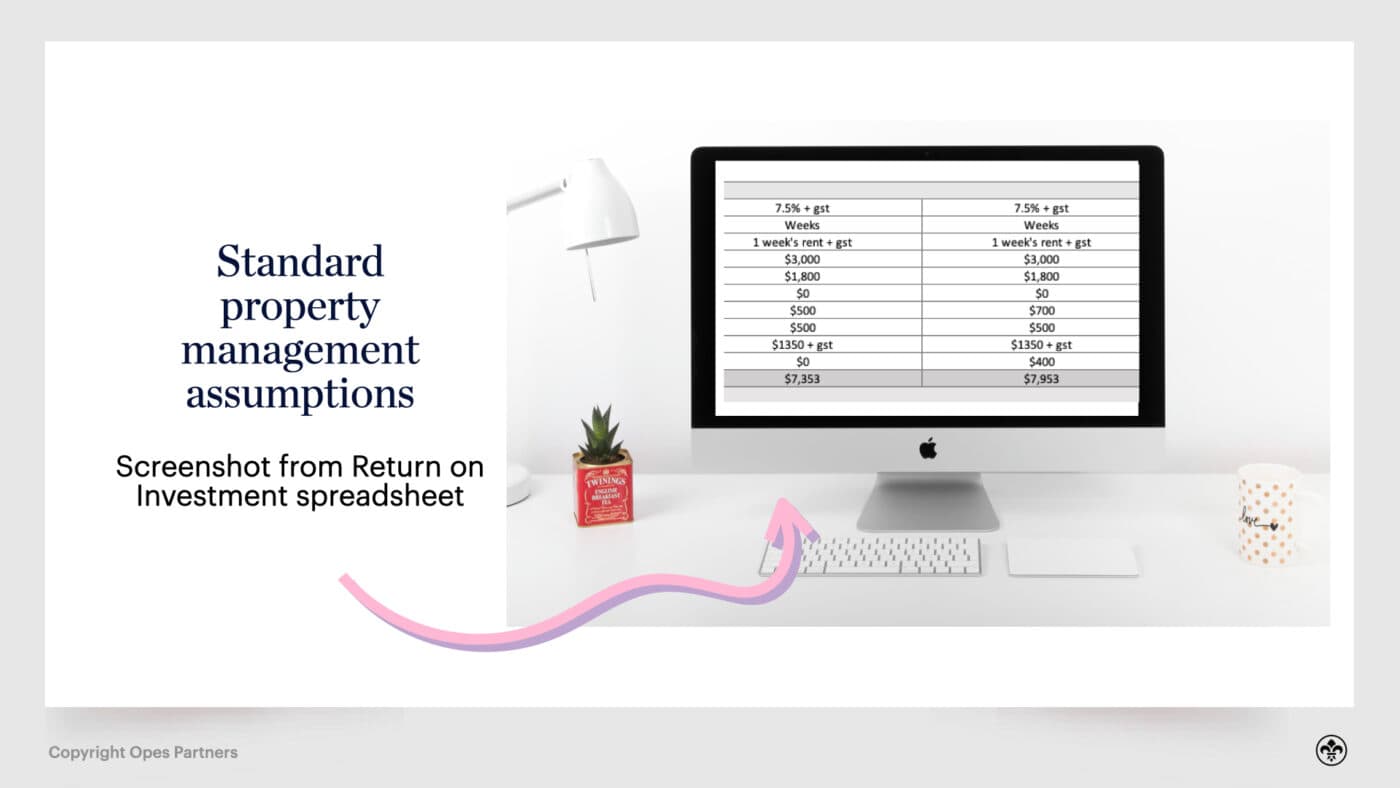

Property managers generally charge two types of fees.

The first is a percentage of the rent you get paid.

This is typically somewhere between 7% (+GST) and 10% (+GST).

For a property charging rent at $500, that’s about $40 - $57.70 per week, or $2,000 - $2,820 a year (factoring in three weeks for the property being empty).

They then also charge a letting fee every time the property is vacant, which is to cover advertising, finding a tenant, and getting that tenant to move in.

This is a relatively new fee, as letting fees were previously charged directly to tenants before a recent law change. This cost is now typically passed on to landlords.

Letting fees are typically one week’s rent + GST, which for a $500-a-week property is $575.

There are two main types of tenancy agreements in New Zealand: Fixed term and Periodic.

It’s particularly important to know the difference because (after changes to the Residential Tenancy Act in February 2021) any fixed-term tenancy agreement automatically rolls into a periodic tenancy … unless a new fixed-term contract is signed.

Fixed term

As already stated, a fixed-term tenancy agreement means a tenant and a landlord are locked in for a certain amount of time (12 months is the norm).

So, let’s say Bob and Simon sign a 12-month fixed-term tenancy agreement in July 2022.

This means before July 2023 Bob and Simon can’t just hand in their 4-weeks’ notice and leave without breaking the contract. If they do, the landlord can charge them for the remaining tenancy. More on this below.

Periodic tenancy

Whereas, a periodic tenancy is a rolling tenancy that has no end date – unless the landlord or the tenant gives notice to end the tenancy.

Having said that, in a periodic tenancy a tenant can give notice for any reason. And while the landlord can end the tenancy in some situations (and ask the tenants to leave) they have to give a legally-approved reason.

And the main reasons now allowed for giving notice are:

There are a few more. But, importantly, there is now no ability for the landlord to ask a tenant to leave “just because”.

So, if your tenant is on a periodic tenancy they are pretty much setting up camp for good (if they want). They can live there indefinitely, which does mean it is rather difficult to give your unruly tenant the boot.

Property Advisers find and source property investment opportunities for you to purchase. They typically fall into two categories – property finders, and property advisers.

Property finders search for properties that meet your buying criteria, or that fit within your existing strategy (and charge you a fee to do so).

Property advisers also find properties for your requirements and strategy, but they also help you create that strategy.

Typically, property advisers do not charge for their service (Opes Partners fall into this category).

If you choose not to use a property adviser you will need to find the property on your own. The risk here is the property you choose may not make a good investment.

You may end up purchasing property that doesn’t fit with the long-term objectives you are trying to achieve (especially if you are purchasing property without a written-down strategy).

Property finders (who follow your existing strategy) typically charge a fee. This is generally 2% of the property price + GST, or a fixed fee (somewhere between $10,000 - $15,000 + GST).

Property advisers, on the other hand, are paid like a stockbroker – they are paid by the existing owner of the property they recommend. This means that most property advisers (like Opes) don’t charge you a fee when you use their service.

We’re into the final steps. Here’s everything you’ve achieved so far:

The final hurdle is getting the funds for the investment and making the numbers work (but you may not have to worry about this if you’ve found the right mortgage broker).

This chapter is broken into 3 sections:

The most important part of investing in property is securing the funds from the bank to buy the investment.

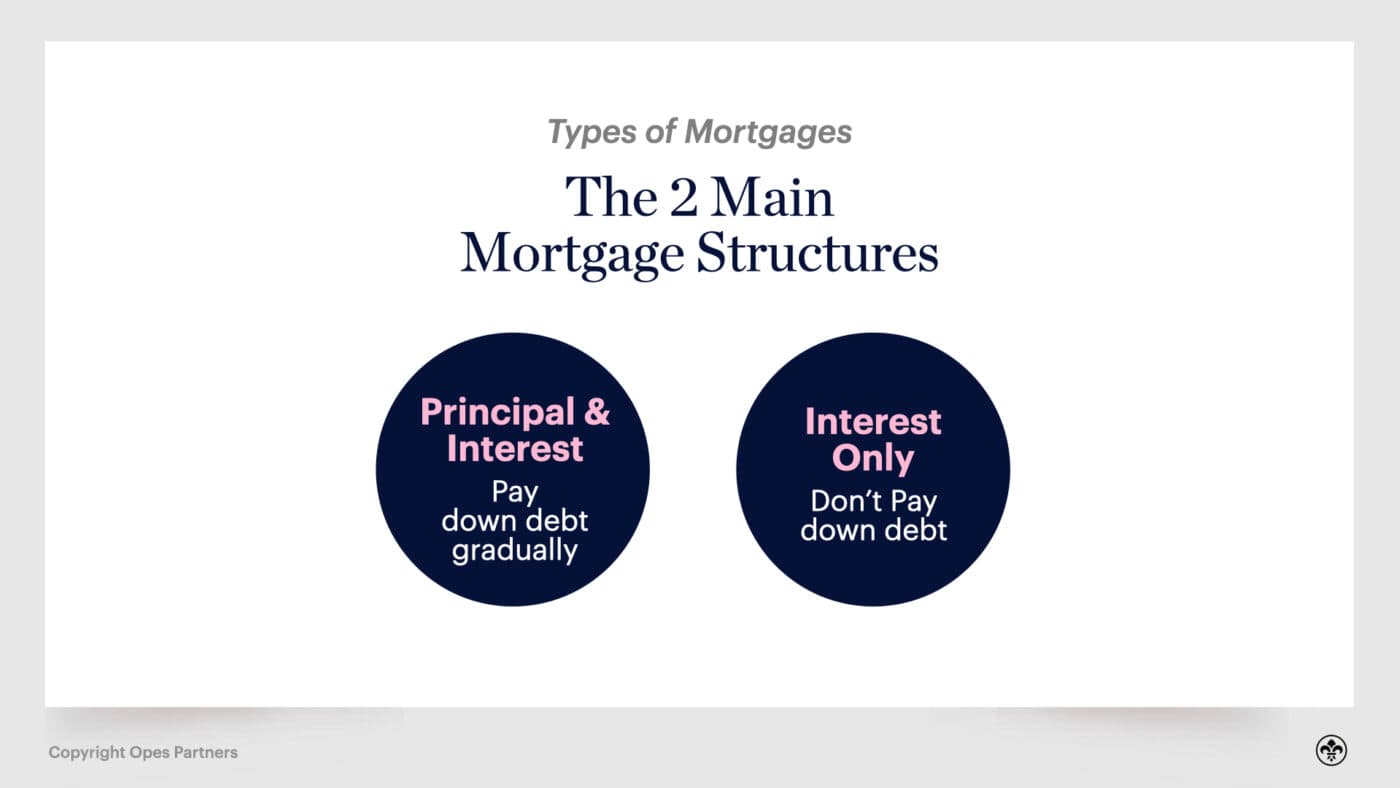

Some investors are surprised to learn there are different types of mortgages they can use to secure the loans, and that the most common loan property investors use is not the same one they use for their home.

The two types of loans are:

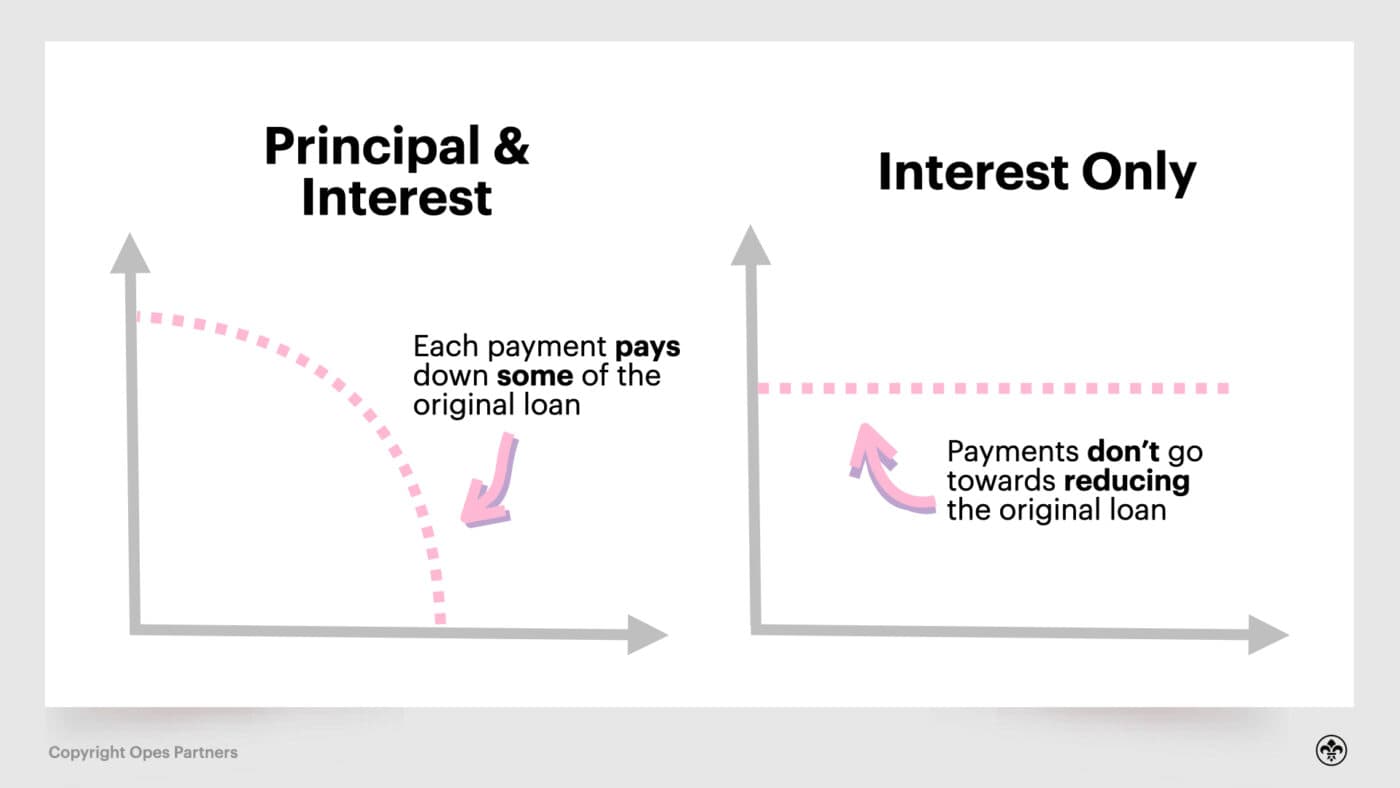

The most common type of loan is a Principal and Interest loan (also called a table loan). This type of loan is mostly used by people for their own homes.

Each payment you make to the bank includes the interest payment – the banks charge for giving you the loan – (e.g. 4%), and also some amount that pays down the loan’s ‘principal’.

Paying that extra ‘principal’ part means the size of the loan goes down each month.

The other type of loan, which is much more common in property investment, is the interest-only loan.

With this loan you only pay interest to the bank each month, and make no principal payment.

This means the size of the loan never decreases.

You might wonder two things:

If your property investment strategy includes holding the property, then the primary way you’re going to make money is through the property increasing in value over time.

Let’s say you purchased a property for $490,000 in 2016, and financed that property on an interest-only loan.

Because the median New Zealand house price increased 73.47% over that period (August 2016 - August 2021) then you will have still made $360,000 in capital gain even though you still have a mortgage.

In other words, investors can build wealth without paying down debt.

The other reason investors use

Reason #2 investors use this type of loan is that properties on principal and interest mortgages are often heavily negatively-geared.

This means the investor needs to make a significant ‘top-up’ to the property’s bank account each week – since the rent doesn’t cover all expenses.

This makes interest-only loans attractive since they are cheaper in the short term, compared with a principal and interest loan.

Let’s go through an example to see what we mean.

Typically, a property set up on principal and interest may be negatively geared by $250 a week.

The same property on an interest-only mortgage may only be negatively geared by $50 a week.

Most Kiwi investors might say “I can afford $50 a week to buy a property … especially if it’s going up in value”. But paying $250 might be a bit more of a stretch, especially if you’ve already got a personal mortgage.

So using an interest-only loan can allow more New Zealanders to become property investors, or grow their portfolios in the short term.

When you use an interest-only loan you are holding onto your debt for longer because you’re not paying down any of the loan.

Over time this means you’ll pay more interest.

So, in the short term you’ll save on cashflow, since your repayments are lower, but you will end up paying more money to the bank in terms of interest payments.

Our view, here at Opes Partners, is that paying more interest over time is an acceptable trade-off for many investors.

The reason is you’ll often be able to build a larger portfolio than is otherwise the case.

Renovations-focused investors will also use these types of loans, especially during renovations.

Because, while an investor is renovating a property, they typically can’t tenant it. So no money is coming in.

This means decreasing their contributions to the bank (through an interest-only loan) is going to give them more funds to spend on the renovation, while limiting outgoings.

What does a mortgage broker think?

Ella Dromgool, a mortgage broker from Opes Mortgages, is in favour of interest-only loans, especially if the investor has their own home mortgage as well.

Ella says the aim of the game is to pay down your debt on your owner-occupier. So, if you have one, make that your focus.

Investors utilise interest-only loans to increase cashflow, which can be spent to invest elsewhere.

But while you aren’t paying down debt, at least not immediately, the investor is relying on the premise the property is going to increase in capital gain. This historically has always been true over the long term.

So, what is the right choice for me?

Generally speaking, a switch to a principal and interest loan can be the right decision for older Kiwi investors, especially for those who have already paid off personal mortgages on their own homes.

This way you can start paying down your debt as you approach your retirement goals.

Compare interest-only loans vs principle and interest loans.

However, if you are an early-mid career investor and you have a sizeable mortgage on your own property, it could be a great idea to go for an interest-only loan on your investment properties.

Generally, this is what we see here at Opes, which is investors paying interest-only on their investments while paying down their personal mortgage first.

Interest-only loans aren’t the right fit for everyone. But if you think it might be an option you want to consider, have a chat with your mortgage broker.

In Chapter 4 we talked about how to start looking for investment properties, and we put it in the context of moving through a Briscoes store to find what you need.

Let’s now say you walk into Briscoes and you are looking for a toaster.

Once you find the shelf with the toasters, you will be confronted with more toasters than you could ever imagine.

Different colours, different features, different brands. And the question is, which one should I get?

Now, searching for a property is not too dissimilar. Let’s say you’re looking for new-build townhouses with 3 bedrooms in the South Auckland area.

You’ll be able to find hundreds of options.

So, how do we narrow it down to find the one that we want to purchase?

This is where we start to use formulae and financial-metrics to see which is the better investment.

That sounds complex, but we’re going to keep it really simple.

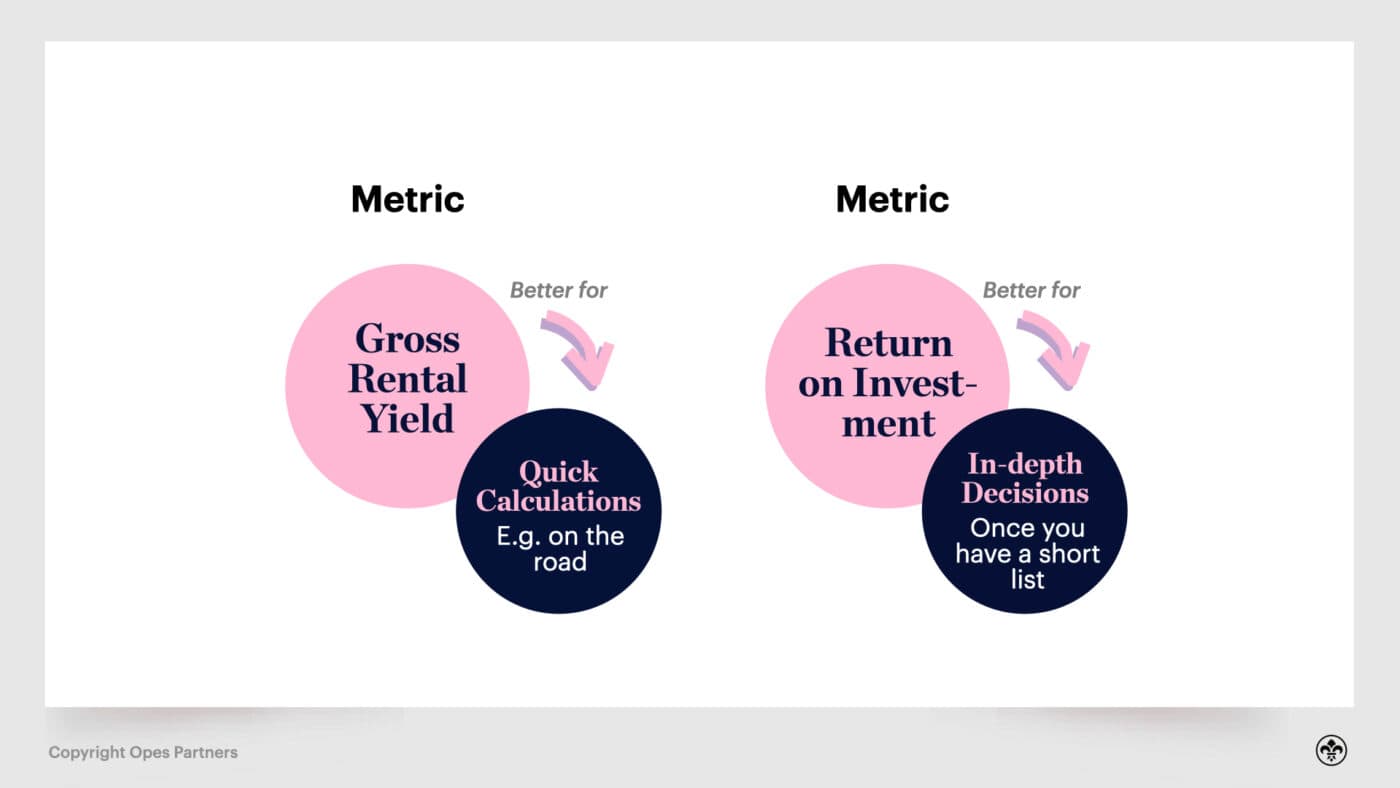

Go to a property investors’ event and you’ll hear everyone talking about gross yields when comparing properties. This is the amount of money a property generates compared to its purchase price.

But, as we’ll see in a moment, there are different types of yields and some give a better comparison than others.

So, in this section we’ll discuss the different types of yields, what they each mean, and the other (sometimes better) metrics you can use to compare properties.

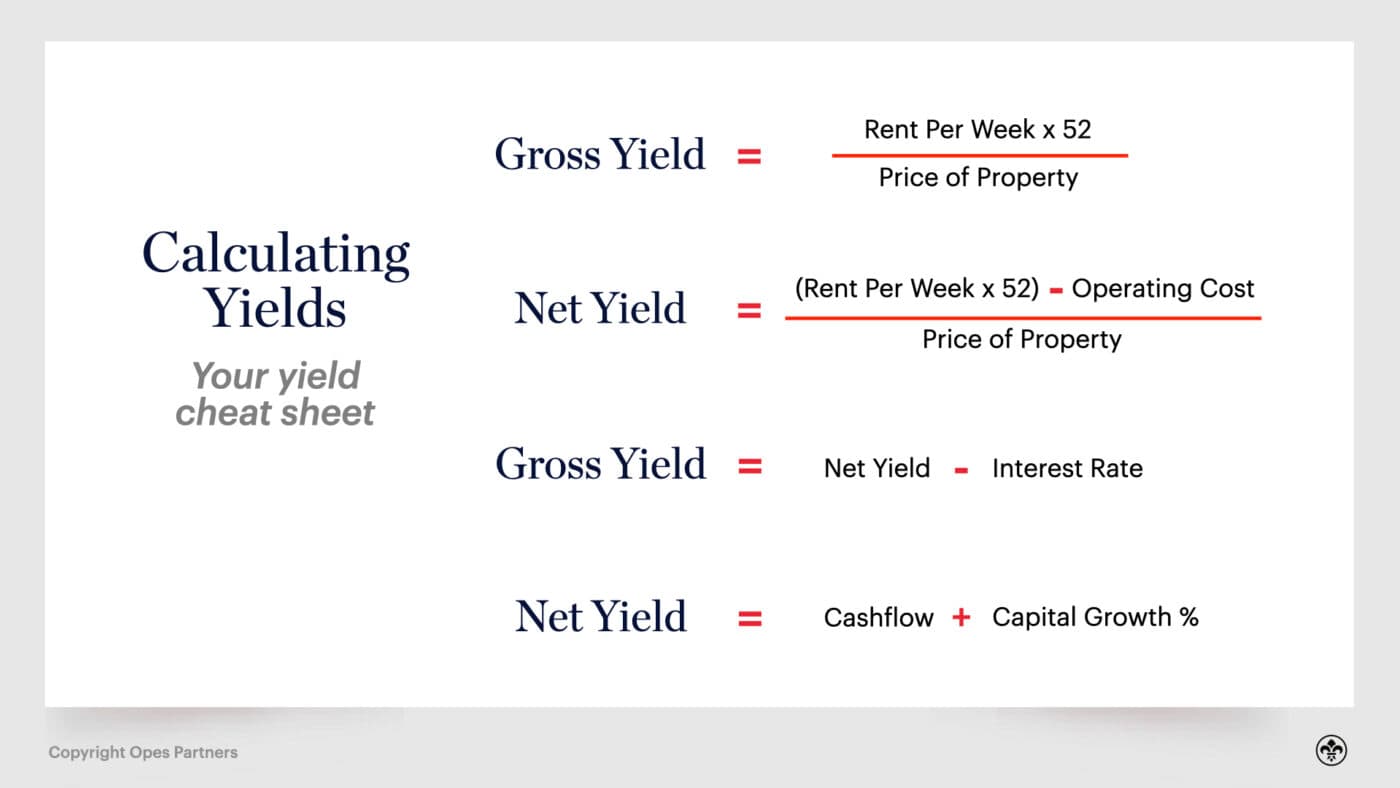

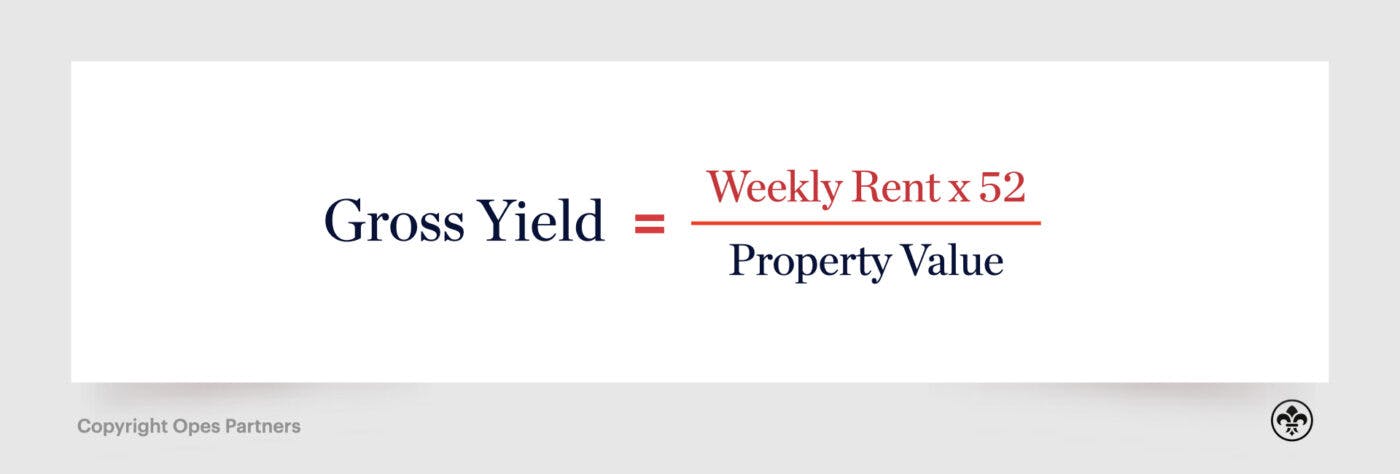

Gross yield

Your gross yield is the most common term you will generally hear from property investors when they talk about yields.

This is calculated by dividing the rent the property earns over a year by the purchase price.

Case study – calculating gross rental yield

Jamie has just bought a property for $500,000. After speaking to his property manager he believes the property will rent for $500 per week.

Jamie multiplies $500 by 52 (the number of weeks in the year), which gives him rental income of $26,000 per annum.

He then divides $26,000 by $500,000, to calculate that his gross rental yield is 5.2%.

The pros and cons of gross yields

The best thing about gross yields is they are incredibly easy to calculate. Because of this they are often the most talked about in property circles.

However, they are of limited use.

However, they are of limited use.

That’s because gross yields don’t factor in things like expenses, or the time a property spends without a tenant paying rent (vacancy), or any capital growth over time.

So, while they are useful for a first look at a property to see whether it’s worth investigating further … the gross yield on its own shouldn’t be the metric to use to determine if you’ll buy one property over another.

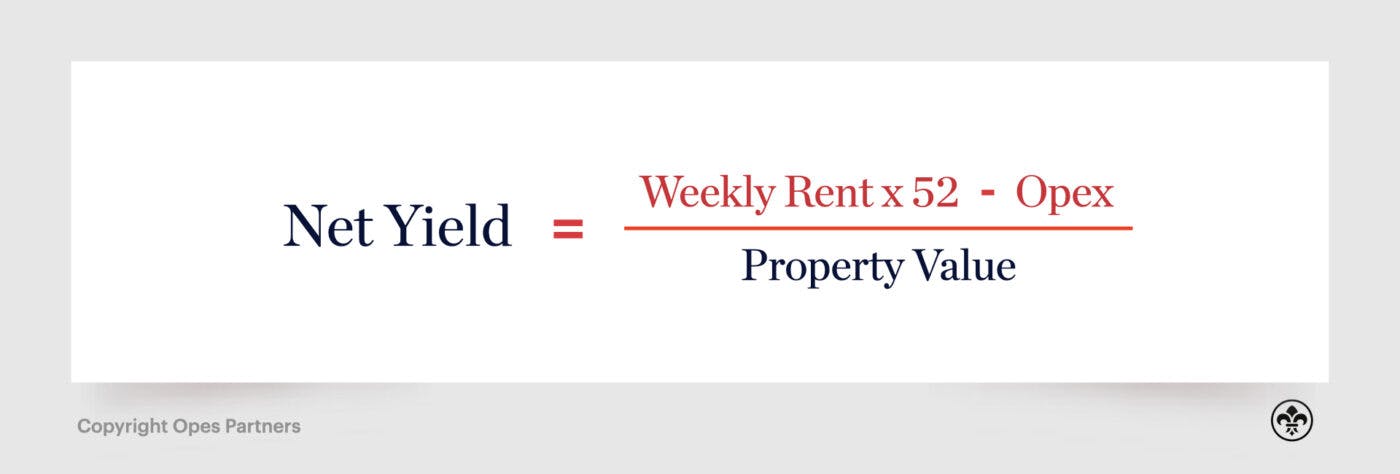

Net yield

Net Yield is a much more useful metric than gross yield.

It tells you how much the property earns (or costs you) each year after operational expenses have been taken out.

Operational expenses include things like vacancy (how long the property is without a tenant), rates, insurance, accountants fees, property management, letting fees and maintenance.

But this does not include your mortgage costs.

This is calculated by taking the rent received each year and deducting the annual expenses. You then divide that number by the property’s purchase price.

Case study – net yield

Hannah bought a similar property to Jamie's. It was $500,000 and earns $500 per week.

It has operational expenses of $10,565 per year. This is made up of:

This means that Hannah’s property makes an operational profit of $15,435 per year ($26,000 - $10,565).

Dividing that by $500,000 – the purchase price of the property – Hannah calculates that her net yield is 3.1%.

However, this is not profit that Hannah can keep.

That’s because in order to buy the property, Hannah got a mortgage from the bank, which means she also has interest costs.

Note: Mortgage expenses are not operational costs, and therefore are not used to calculate net rental yield. Leaving mortgage expenses out of net yield is also useful as you can more easily compare different investment opportunities.

The pros and cons of net yields

Net yields are a little bit better than gross yields, since they take into account expenses.

Let’s say you have two properties earning the same amount of rent, but one has really high body corporate fees.

The net yield will show us the high body corporate property will likely provide a lower return.

But the net yield still has some limitations. It doesn’t tell us anything about capital growth, and it doesn’t give us a sense of the actual cashflow we’ll take out of the property, since mortgage costs aren’t included.

This is where the cash yield starts to come in.

Cash yield

Your cash yield includes your payments towards your mortgage.

This is typically the metric most property investors are interested in, as it shows the real money the investor is either putting into the property each week or able to take out of the property each week.

There are two possible ways to calculate your cash yield:

First way to calculate yield

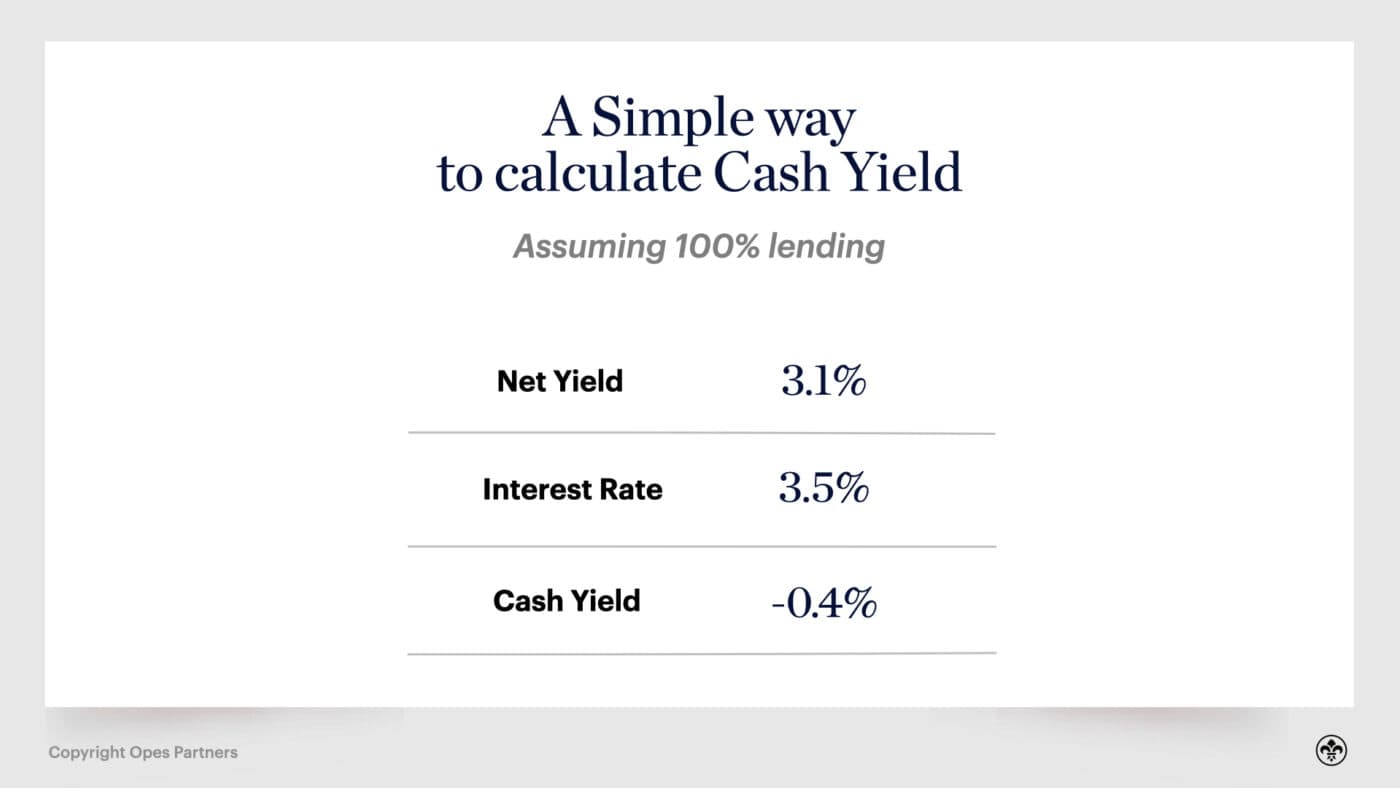

The first is to simply take your net yield and minus the interest rate.

This assumes you plan to borrow 100% of the money to purchase a property and that you’ll put it on interest-only.

Case study

Hannah has already calculated her net yield is 3.1%. She goes to her mortgage broker and is able to secure an interest-only loan at 3.5%, which will cover the entire purchase price (100% lending).

By subtracting 3.5% from 3.1%, she sees that her annual cash yield is -0.4%.

Multiplying this yield by the purchase price ($500,000), Hannah sees that her property will be cashflow negative by $2,000 in the first year.

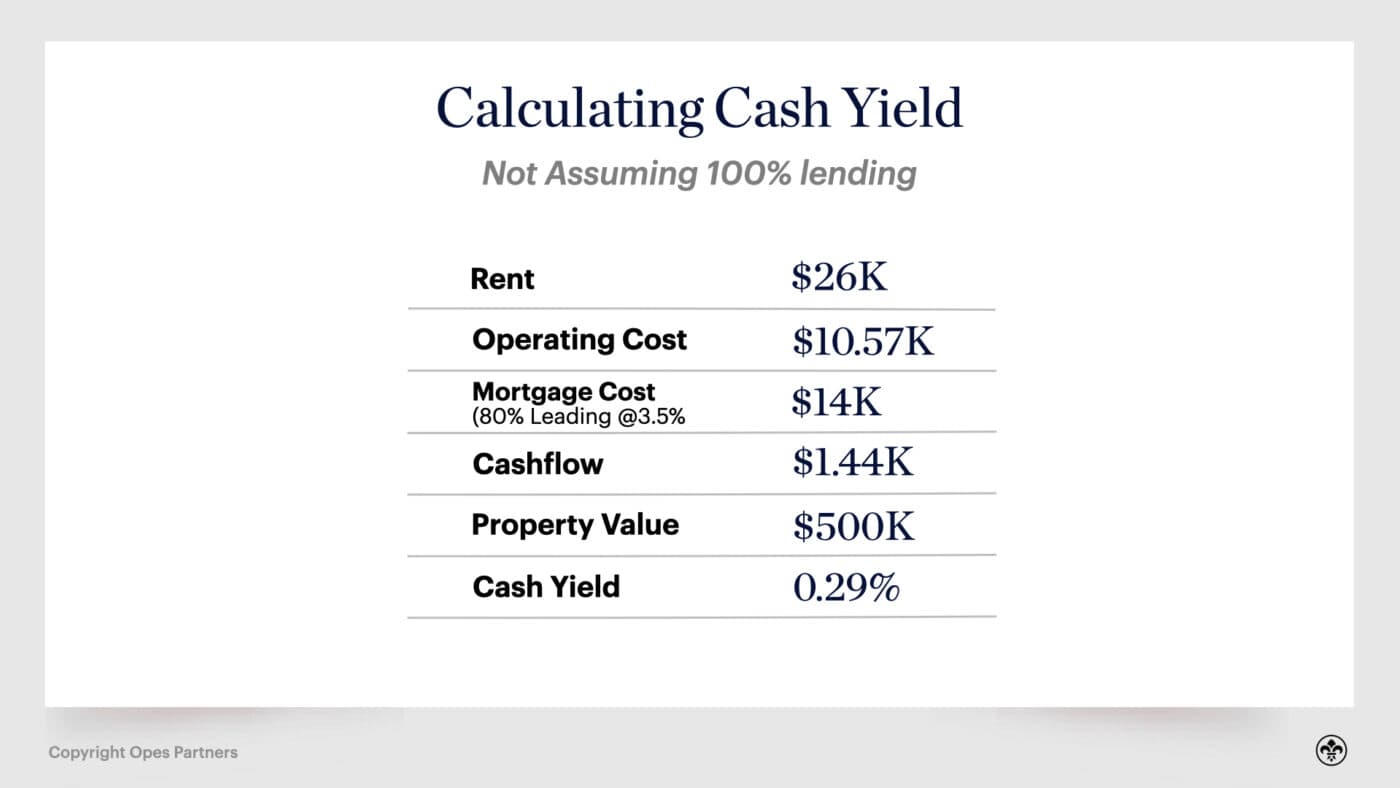

Second way to calculate cash yield

The second way takes a little more arithmetic to calculate, but it doesn’t include the 100% lending or interest-only assumption. So, it’s a little more flexible.

To calculate this, take the Net Yield (expressed in dollar terms), and minus the mortgage repayments. Then divide that number by the purchase price of the property.

Case study

Let’s stick with Hannah and her $500,000 property.

She goes to her mortgage broker and secures that interest-only loan at 3.5%. However, this time she uses a 20% cash deposit.

This means that instead of paying interest on $500,000 she now only has to pay interest on $400,000.

So, her interest costs are $14,000, rather than $17,500 like they were in the first example.

Hannah calculates she’ll receive $26,000 in rent. She’ll then have $10,565 of operating costs and $14,000 of interest costs. This means the property will have positive cashflow of $1,435 in the first year.

When Hannah divides that cashflow by the property’s $500,000 purchase price, she sees her property will earn a cash yield of 0.29%.

When to use this second method

It’s important to use this second method if you are not purchasing the property with 100% bank lending or are using a principal and interest (P+I) mortgage.

Using a deposit or going P+I will impact your mortgage payments and therefore change your cashflow.

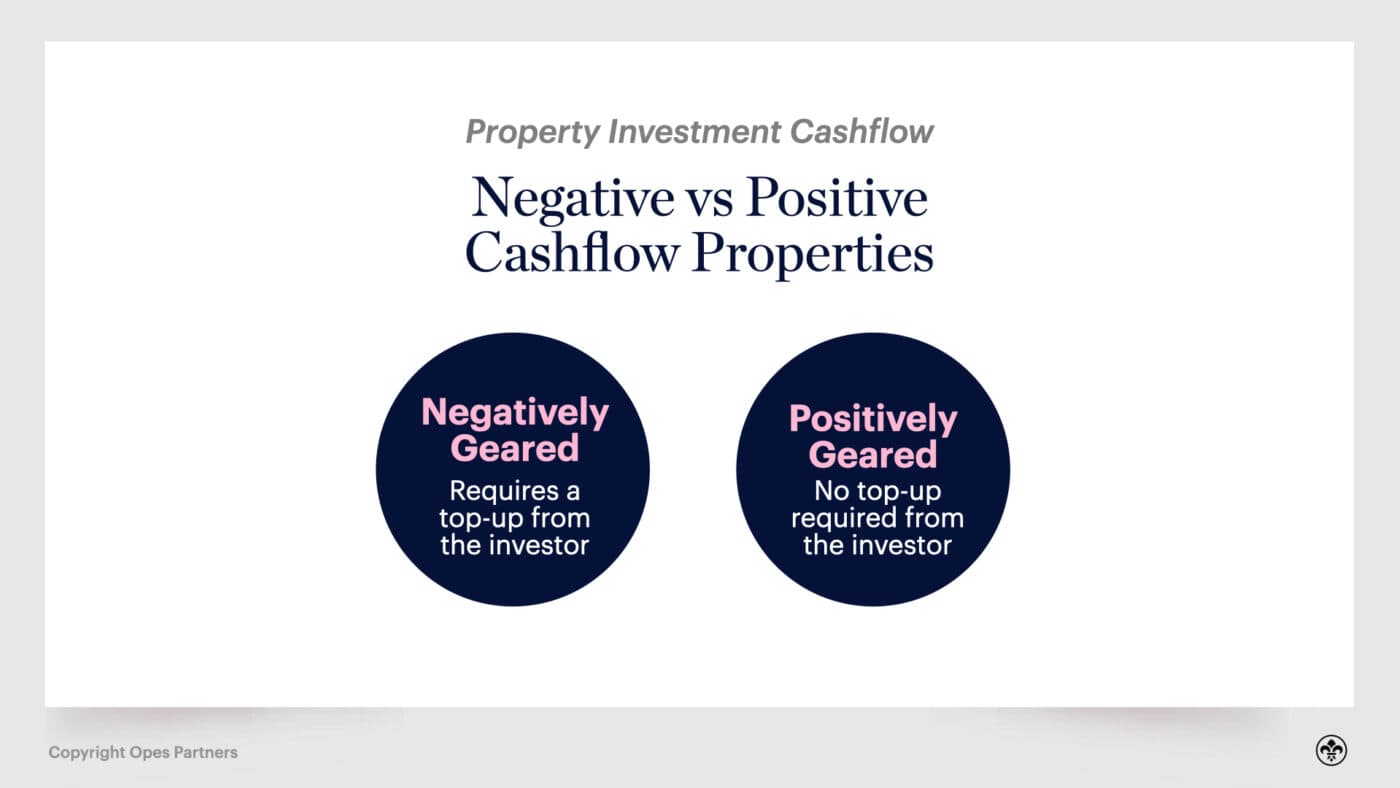

The same investment property can be ‘positively geared’ or ‘negatively geared' depending on how you structure it

In this example, when Hannah purchased the property without a cash deposit, the property costs her $2,000 a year.

But when she uses a cash deposit, the property then makes her cashflow – since the interest expenses are lower.

The first scenario is what we call a ‘negatively-geared’ property (or a cashflow negative property). That’s because once the expenses are taken out the property earns a cash loss each week.

The second scenario is what we’d call a ‘positively geared’ property (or a cashflow positive property), because once its expenses are taken out it earns money.

You may be wondering why anybody would invest in a property that is negatively geared and incurs a cost to the investor each week.

I can hear you saying: “It’s an investment – shouldn’t it be earning me money?”

This is how many investors felt a few decades ago when yields were higher and cashflow positive properties were aplenty.

As property prices have risen faster than rents, negatively geared properties are more popular.

Because while a property may cost $50 a week in cashflow (on average) it may make hundreds of dollars a week as the value of the property increases.

But those potential capital gains haven’t been factored into any of the metrics we’ve discussed so far.

This is why, here at Opes Partners, we’ve had to create a way of calculating a property’s return, that is both simple – and factors in all the possible returns.

Return on investment

The Return on Investment is a calculation Opes uses to help investors understand the total gain the property earns an investor over a 15-year period.

This is a more realistic metric for investors to consider because:

Because these are much more complex calculations, we’ve built a Return on Investment spreadsheet, which you can download for free in order to run the numbers for any investment property you’re considering.

But to simplify this, the spreadsheet looks at all the potential returns over time:

It then divides this by all of the potential investment an investor has put in:

This gives the investor one metric to look at to accurately compare rental properties over time.

Case study

Let’s come back to Hannah with her $500k rental property. In this case we’ll keep all the assumptions the same as the above.

Once we plug those numbers into the Return on Investment calculator, we see that Hannah is expected to receive a 444% return on the money she has invested into the property over the long term.

That’s because the property is expected to earn about $440,000 over the next 15 years, whereas she has only invested $100,000 of her own equity.

Just over 90% of those gains are expected to come from capital gains – the property increasing in value. And the other 10% from rental cashflow.

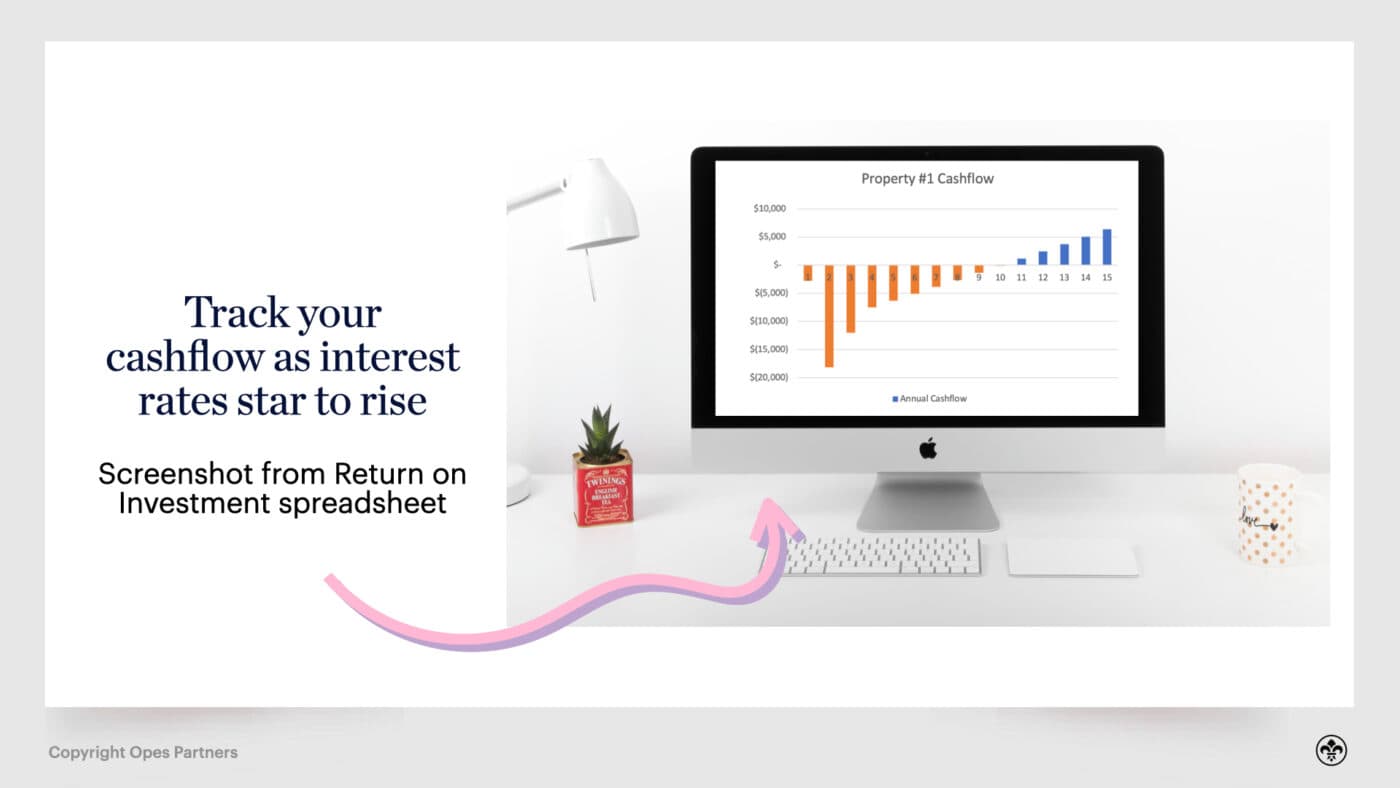

Using this spreadsheet, Hannah can also track the expected cashflow of her property, even as interest rates rise.

The pros and cons of return on investment

The benefit of a return on investment calculation when running the numbers on an investment property is you get a much fuller picture of your investment.

This is because it takes many more real-world factors into account, and includes all the ways you might make money from a property.