What is a Wealth Plan?

Your Wealth Plan is made up of 5 simple parts:

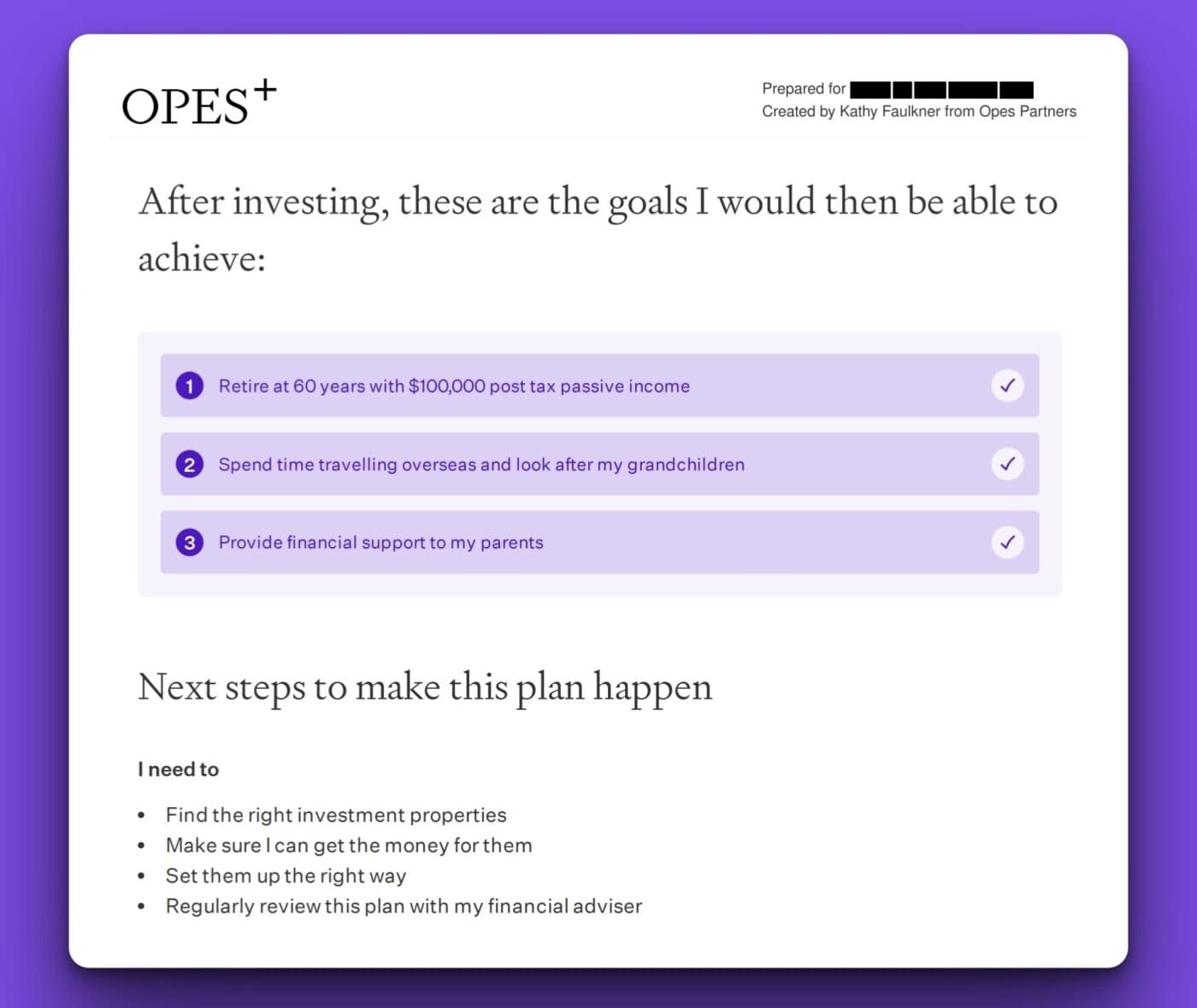

Step #1 – Work out where you want to go

Everyone has goals. Whether it’s to retire on the same lifestyle, or quitting work early to travel the world.

The first step is to turn those goals into numbers. Ask yourself: “How much do I want to spend per year?”

You can then calculate how much money you’ll need in the bank to make that happen.

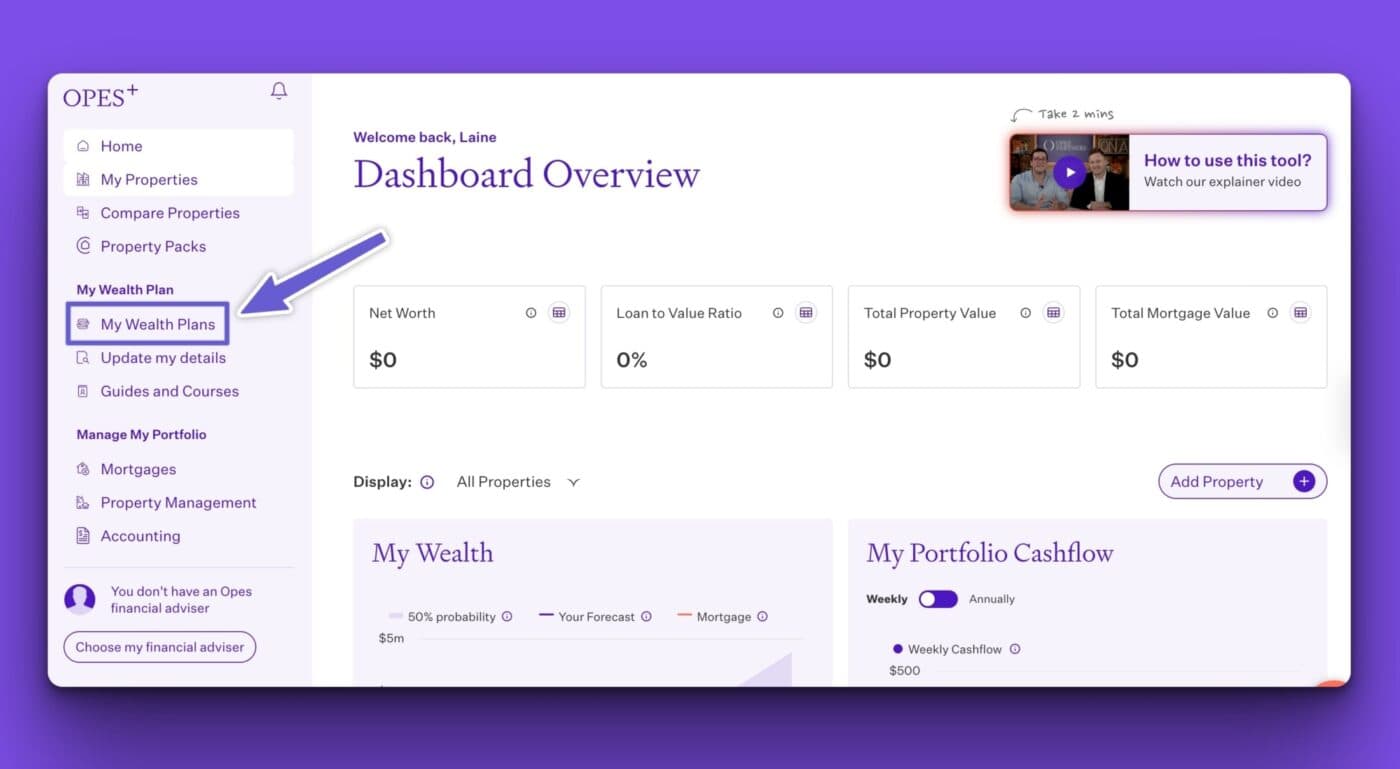

Step #2 – Work out where you are now

This means understanding how much you are worth today (financially). That includes your income, expenses, savings, KiwiSaver, mortgages, properties and investments.

Step #3 – Calculate where you will be in the future

Even if you don’t have lots of money today, that doesn’t mean you’re not doing anything about it.

If you’re contributing to KiwiSaver, own a rental property, or investing in a fund, your wealth should grow over time. You’re already investing for your future.

But you need to calculate where all that investing will take you. Will it be enough for the future you want? All this can take a fair bit of number crunching.

Step #4 – Calculate your Wealth Gap

Once you’ve figured out how much money you’ll need … and what you’re on track for … you can then see if there’s a difference.

If you’re current investing isn’t likely to get you to your goal, then you have a Wealth Gap. It’s OK … many New Zealanders do.

That often means you either need to decrease your goals or invest more.

Step #5 – Create a plan to invest more

This is the interesting part. If you decide you want to close your Wealth Gap, then the answer is often to save (or invest) more.

This is where you look at different scenarios to change your outcome.

For example, what happens if you repay debt faster? Or what if you buy an investment property or invest more in KiwiSaver?

Or what happens if you do nothing and just ride it out?