Property Investment

The top 9 reasons kiwis invest in property (in their words)

In this article we’ll go through the top 3 reasons Kiwis invest in property. Then we’ll go through an additional 6 reasons other investors put their money in property.

Property Investment

5 min read

Author: Laine Moger

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Audio version of the article

As the most basic of definitions, property investment uses properties to fund your future retirement.

Yup, get rich with property – it’s that simple, right? Or is it?

In all honesty, the ins and outs of what’s involved in property investing could fill a book.

It did, in fact our book Wealth Plan – How To Invest In Property and Retire on Real Estate is being released this year.

But, in this article you’ll learn the core basics of property investment in just 1,000 words, starting … now.

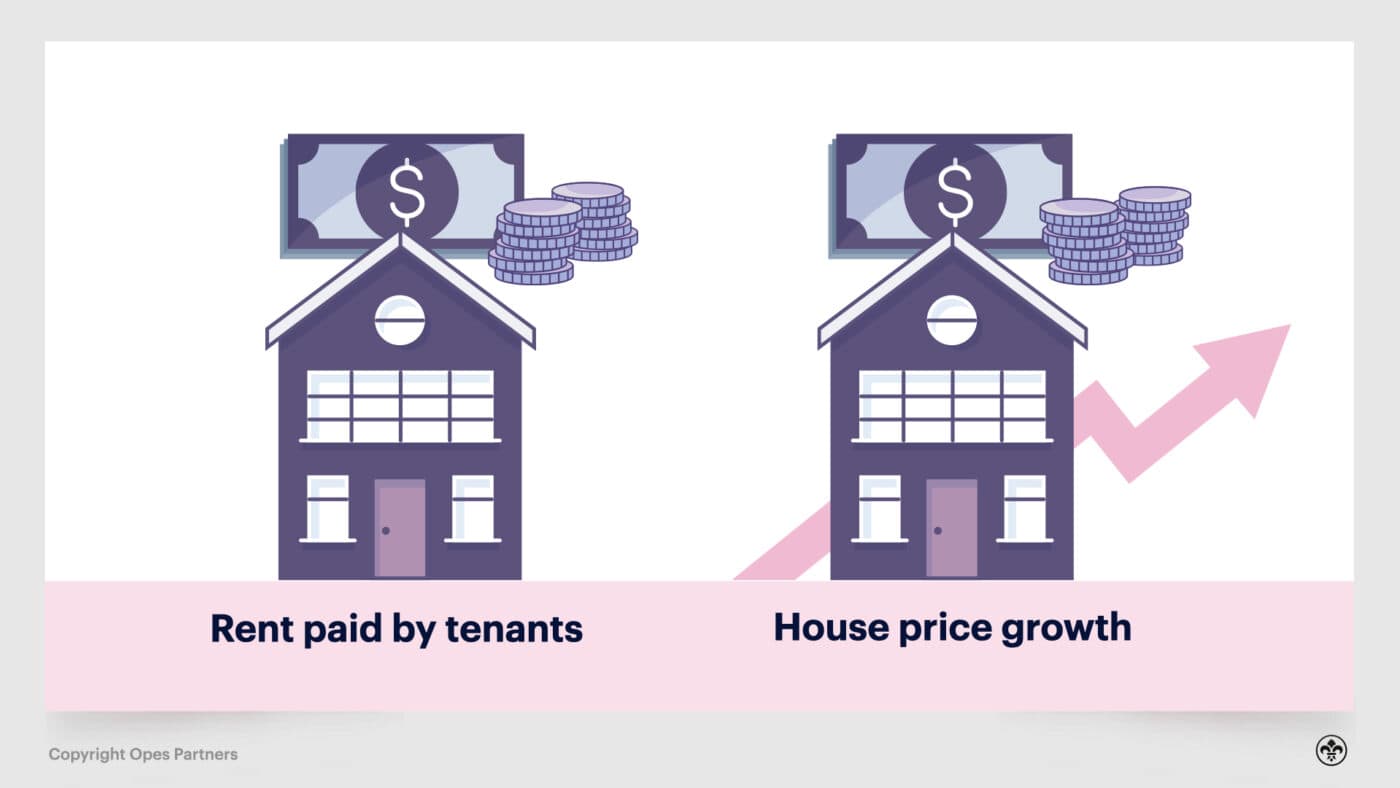

Property investment is buying property for the purpose of creating wealth.

It has two ways of *potentially making you money, or returns.

#1 – Rent paid by tenants

#2 – House price growth (capital gains).

You need two things to get a mortgage so you can get started and buy an investment property –

#1 – Your own home with equity in it

#2 – You need a job (income) to service the mortgage

You do not need to have a lot of cash in the bank. Many Kiwis invest in property with less than $5,000.

Use a simple calculator, like the one below, to see if you are in a financial position to invest.

When you strip out the detail there are only two tried-and-true residential property investment strategies investors tend to use.

#1 – ‘Buy and Hold’

#2 – ‘Buy and Flip’.

If you’re a “buy and hold” you buy property and rent them out – for the purpose of holding on for the long term.

The alternative is the “buy and flip” strategy or “flipping” as it’s more commonly known. This is when you buy a property that needs work, renovate, and then immediately sell.

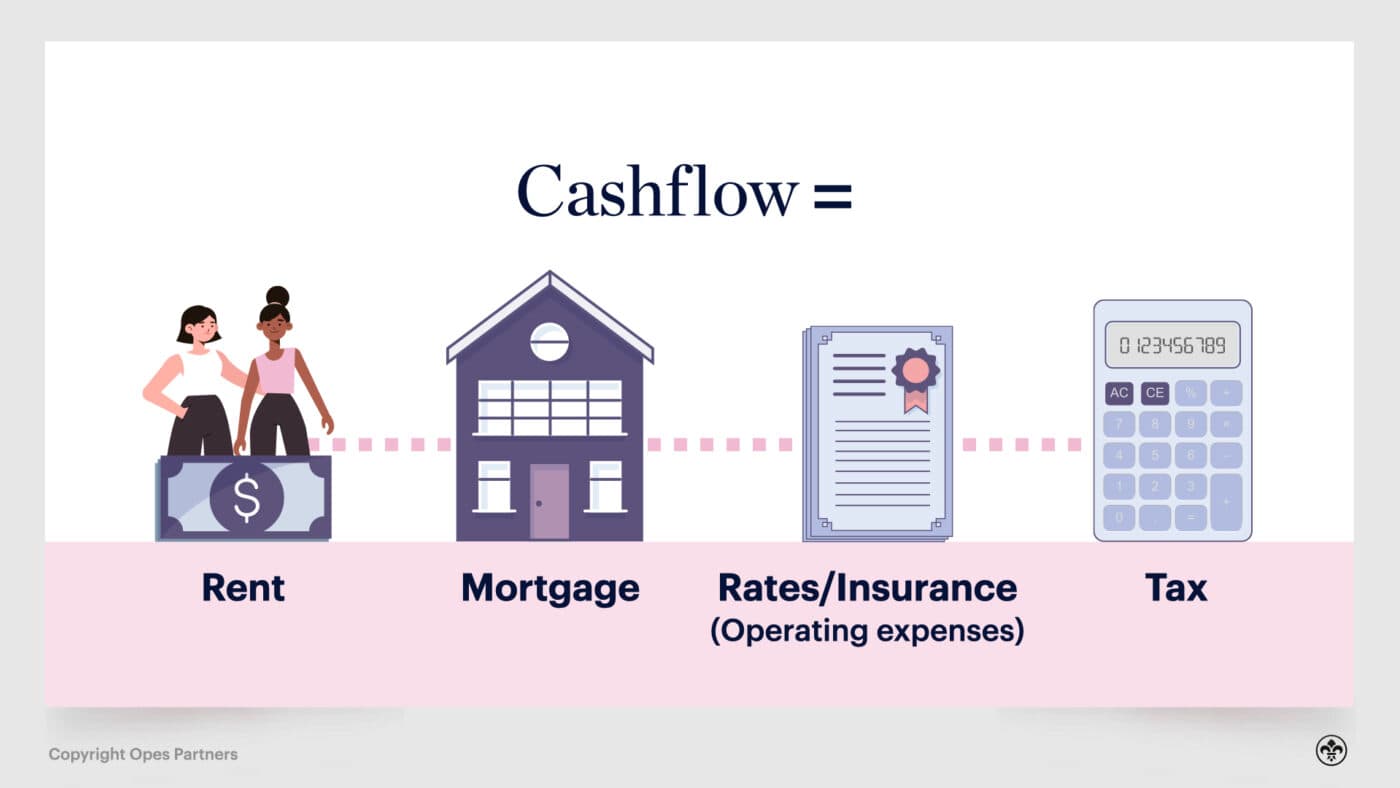

Cashflow is talked about a lot in investment circles.

Cashflow is the money that goes in and comes out of your investment property’s bank account.

For instance: Cashflow = rent - mortgage - operating expenses (rates and insurance) - tax

How much flow you have on your property investment’s cash depends on a whole bunch of things, and it’s mainly to do with your investment strategy.

For instance, an acceptable cashflow for a passive buy-and-hold investor dealing in New Builds is going to be different to an active investor who is using the BRRRR strategy to renovate properties.

New Builds are often negatively-geared (at least initially), which means the rent flowing in doesn’t cover all the other expenses.

Whereas active investors specialise in increasing rental income considerably. It’s unlikely they’d settle for a negatively-geared property after this.

An acceptable cashflow for a New Build is split into two camps:

#1 – Growth

#2 – Yield

For instance, a growth property tends to increase in value more substantially, but has less cashflow. Conversely, a yield property tends to go up in value slower, but has greater cashflow.

Your investment property’s annual cashflow will be affected, in part, by the rental yield.

There are a couple of types of yield and different ways for calculating them.

Here at Opes we have a benchmark yield of 4%, which means we wouldn’t recommend a property that doesn’t meet this standard.

Opes investors can also use our Return on Investment calculation to understand the total gain the property earns an investor over a 15-year period.

The right investment property will be initially swayed by what strategy you choose and how much you can afford.

But then you’ll have to think about where you want to invest, and what sort of property is right for you.

These details are unique to each investor.

For instance, if you are just starting out and have limited funds, an apartment or 2-bed townhouse in Christchurch may be the best option.

However, once you get a bit more established it’s likely you’ll want to break into heftier investment properties.

For instance, a standalone property in outer Christchurch, a 3 or 4-bed townhouse in Auckland, or a dual-key apartment in Wellington.

Regardless, you’re always going to want to look at the “where to invest” first. This is because you want your property to tick:

#1 – Long-term equity gain

#2 – A reasonable yield (cashflow)

Both of these are market-led, and the property you choose will perform differently depending on the region it’s in.

The frustrating answer to every investor’s question: “What’s a good rental yield in the city I’m investing in?” is “it depends.”

This is where you need to do your own calculations to work out what sort of cashflow, or yield, you’ll get for your property.

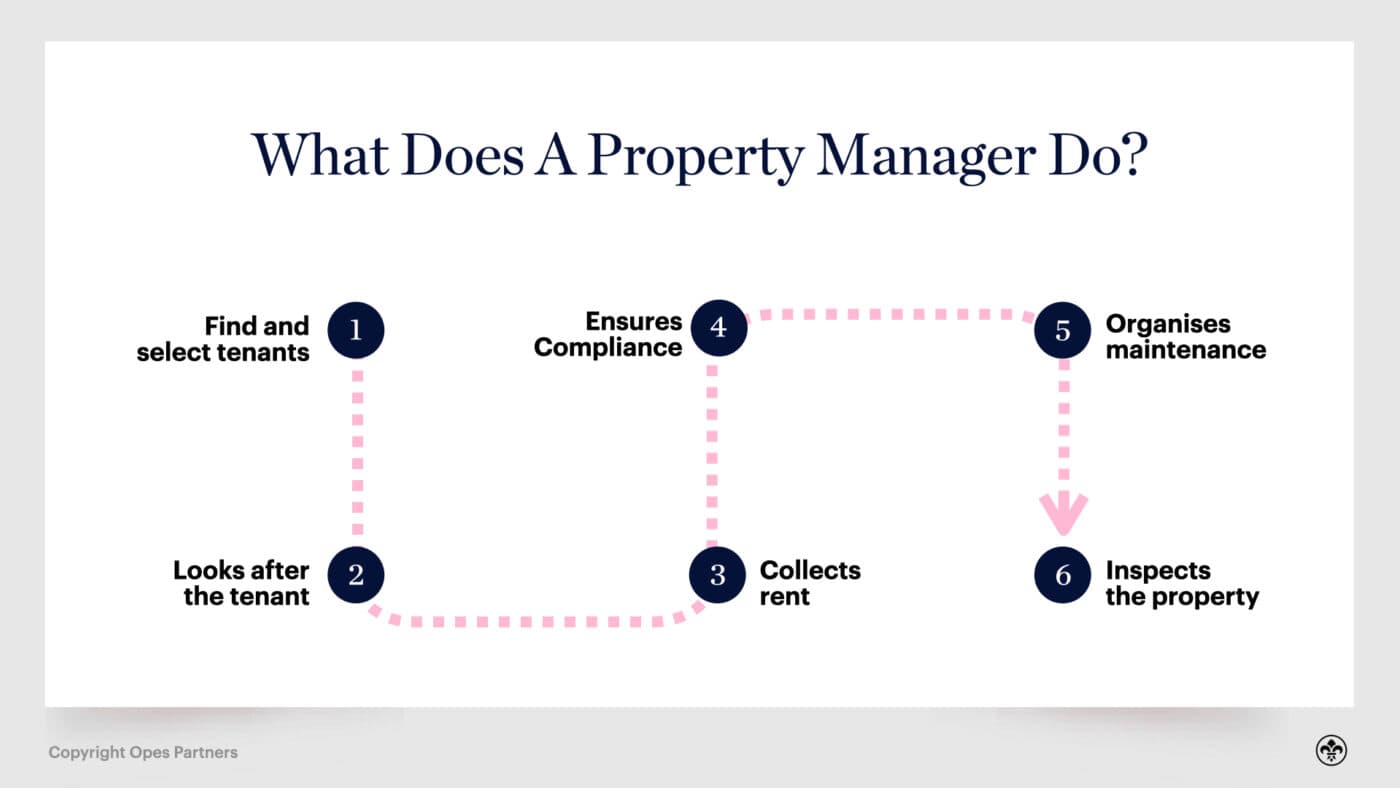

It is vital to use a property manager. You’ll pay them a percentage of the rent to look after the house and the tenant. That way you don’t get the tenant’s 11pm calls when they’ve locked themselves out.

The property manager will help you set the rent, run inspections, organise any maintenance and vet the tenants.

They can also give you a “rental appraisal”, which is the predicted rent for your New Build property. This is essential when working out the cashflow of your property, and if you are going to achieve a reasonable yield.

Two ways – You can DIY.

There are loads of online tools out there (our articles too) to help you find a property, vet your own developer, work out your Return on Investment and get tenants in.

However, if you prefer to be guided along the process you can enlist the help of investment property specialists, like us here at Opes.

Well … it could be.

It depends on what your financial situation is and what sort of investment strategy you want to go for.

There are a lot of people out there who believe they can’t invest, when actually they can.

It’s just a matter of getting investment-ready and having an adviser talk you through your options.

There is, obviously, so much more that goes into it beyond these 1000 words, but these are the basic foundations.

Our saying here at the office goes: “Don’t wait to invest, invest and wait.” You’ve kinda just gotta go for it.

Journalist and Property Educator, holds a Bachelor of Communication (Honours) from Massey University.

Laine Moger, a seasoned Journalist and Property Educator holds a Bachelor of Communications (Honours) from Massey University and a Diploma of Journalism from the London School of Journalism. She has been an integral part of the Opes team for four years, crafting content for our website, newsletter, and external columns, as well as contributing to Informed Investor and NZ Property Investor.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser